Operational Highlights

Operational Highlights

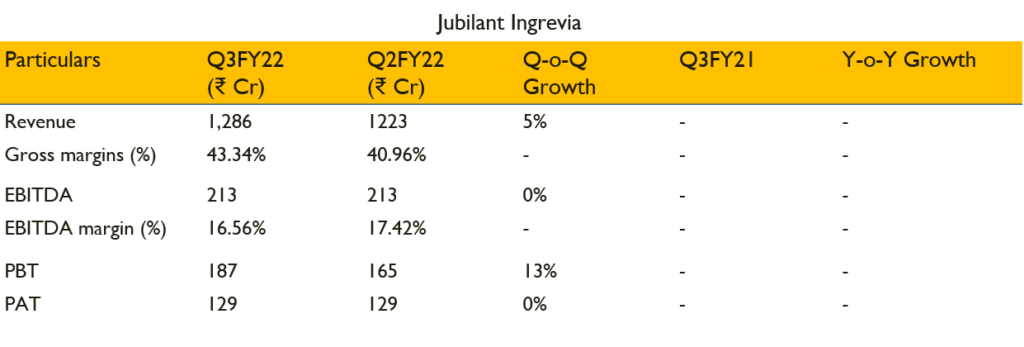

- Revenue grew by 44% on YoY basis, driven by growth across product segments to ₹1,286 in Q3FY22 from ₹893 in Q3FY21

- Revenue from Pharma, Nutrition and Agro end use increased significantly.

- Most of the input cost is passed on resulting in better realisations

- Dow Jones sustainability index is 81% for the company and ranked top 20 chemicals globally and top 3 in India

- Acetic acid prices were high due to china and supply constraints

- The change in duty for acetic anhydride and methanol will benefit more to consumers then the manufacturers

Business strategy

- Focus on debottlenecking on existing products

- Acetic acid supply will be better at the end of quarter and prices are softening

- Targeting to increase volume QoQ

- 34 new products under pipeline and expected to launched in coming years

- Might consider additional capex until next call

- 55% of business is from the life science segment and 45% from speciality. Post capex as the revenue mix shifts more to speciality, margins expansion will be visible

- If raw material prices stay high and continue at these levels, the revenue will be doubled earlier the FY26

Segmental Overview

Speciality chemicals

- Revenues stood at ₹349 Cr contributing 27% to revenues with 21.8% EBITDA margins

- Speciality Chemicals revenue grew by 22% YoY driven by volume growth across products and passing-on of higher input costs.

- Pharma Sales share to total revenue grew to 52% from 47% earlier.

Health and Nutrition

- Revenues stood at ₹216 Cr contributing 16% to revenues with 24.4% EBITDA margins

- Nutrition and Health Solutions revenue grew by 37% YoY driven by higher volumes and improved price realisation

- Sales in vitamin B3 improved due to high realisations and volume growth

- Revenue share from EU increased to 36% as against 20% last year and share from North America increased to 21% from 11% earlier.

Life sciences

- Revenues stood at ₹722 Cr contributing 56% to revenues with 13.9% EBITDA margins

- Life Sciences Chemical revenue grew by 60% YoY, driven by higher prices on account of favourable market conditions

- High demand in European as well as domestic regions

- Life Sciences Chemical revenue growth was driven by higher prices of Ethyl Acetate and Acetic Anhydride

Capex

- Food Grade Acetic Acid. (expected by April to June 2022)

- CDMO GMP Facility at Bharuch. (expected by July to Sep 2022)

- Three Multi-Purpose plants of Speciality Chemicals. (expected by July to Sep 2022)

- Acetic Anhydride Plant. (expected by Jan to March 2023)

- Agro Actives Phase-1. (expected by Jan to March 2023).

- Diketene plant is commissioned and demand is high in India as many consumers are importing. Few customers are waiting with order books

- Capex is on course and expect to double the revenues in FY26 from FY20 mark

- Committed investment worth Rs. 450 Crore for key growth capex is progressing well. At peak capacity these investments are expected to generate additional annual revenue of ₹ 900-₹1,000 Crore at prevailing prices.

- Expected capex cash outflow for the year is expected to be in the range of ₹300 crore.

- Gross Debt reduction by ₹263 Crore and Net Debt reduction by ₹201 Crore from 31st March 2021

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

The Real Person!

The Real Person!

kamagra livraison 24h: kamagra oral jelly – Kamagra Commander maintenant

The Real Person!

The Real Person!

kamagra gel: achat kamagra – kamagra oral jelly

The Real Person!

The Real Person!

Pharmacie Internationale en ligne: Pharmacie en ligne France – pharmacie en ligne pharmafst.com

pharmacie en ligne sans ordonnance: Livraison rapide – pharmacie en ligne france livraison internationale pharmafst.com

The Real Person!

The Real Person!

acheter mГ©dicament en ligne sans ordonnance: pharmacie en ligne sans ordonnance – pharmacie en ligne avec ordonnance pharmafst.com

vente de mГ©dicament en ligne: Pharmacie en ligne France – acheter mГ©dicament en ligne sans ordonnance pharmafst.com

The Real Person!

The Real Person!

pharmacies en ligne certifiГ©es: pharmacie en ligne – pharmacie en ligne france livraison belgique pharmafst.com

The Real Person!

The Real Person!

Achetez vos kamagra medicaments: achat kamagra – kamagra livraison 24h

kamagra pas cher: Achetez vos kamagra medicaments – kamagra livraison 24h

The Real Person!

The Real Person!

pharmacie en ligne livraison europe: Medicaments en ligne livres en 24h – Achat mГ©dicament en ligne fiable pharmafst.com

The Real Person!

The Real Person!

Acheter Cialis: cialis prix – Cialis en ligne tadalmed.shop

The Real Person!

The Real Person!

achat kamagra: kamagra gel – acheter kamagra site fiable

The Real Person!

The Real Person!

Tadalafil 20 mg prix sans ordonnance: Acheter Cialis 20 mg pas cher – Acheter Cialis tadalmed.shop

The Real Person!

The Real Person!

Achetez vos kamagra medicaments: kamagra 100mg prix – acheter kamagra site fiable

The Real Person!

The Real Person!

pharmacie en ligne sans ordonnance: Pharmacies en ligne certifiees – Achat mГ©dicament en ligne fiable pharmafst.com

The Real Person!

The Real Person!

achat kamagra: achat kamagra – Kamagra pharmacie en ligne

The Real Person!

The Real Person!

cialis sans ordonnance: Acheter Cialis – Acheter Viagra Cialis sans ordonnance tadalmed.shop

The Real Person!

The Real Person!

Tadalafil sans ordonnance en ligne: Tadalafil sans ordonnance en ligne – cialis prix tadalmed.shop

The Real Person!

The Real Person!

Acheter Kamagra site fiable: kamagra 100mg prix – Kamagra Commander maintenant

The Real Person!

The Real Person!

kamagra oral jelly: kamagra gel – acheter kamagra site fiable

The Real Person!

The Real Person!

pharmacie en ligne livraison europe: Pharmacies en ligne certifiees – pharmacie en ligne fiable pharmafst.com

The Real Person!

The Real Person!

Tadalafil achat en ligne: Tadalafil sans ordonnance en ligne – cialis prix tadalmed.shop

The Real Person!

The Real Person!

pharmacie en ligne avec ordonnance: Pharmacies en ligne certifiees – pharmacies en ligne certifiГ©es pharmafst.com

The Real Person!

The Real Person!

indian pharmacy online: medicine courier from India to USA – indian pharmacy online

The Real Person!

The Real Person!

Medicine From India: Medicine From India – Medicine From India

The Real Person!

The Real Person!

MedicineFromIndia: п»їlegitimate online pharmacies india – MedicineFromIndia

The Real Person!

The Real Person!

medicine courier from India to USA: indian pharmacy online shopping – MedicineFromIndia

MedicineFromIndia indian pharmacy online MedicineFromIndia

The Real Person!

The Real Person!

mexican rx online: Rx Express Mexico – buying prescription drugs in mexico

RxExpressMexico mexico pharmacies prescription drugs mexican online pharmacy

The Real Person!

The Real Person!

indian pharmacy: india pharmacy – indian pharmacy online

Rx Express Mexico: mexico pharmacy order online – mexico pharmacies prescription drugs

The Real Person!

The Real Person!

canadian pharmacies comparison: Buy medicine from Canada – canadian drugstore online

MedicineFromIndia cheapest online pharmacy india indian pharmacy

canadian drug prices: Canadian pharmacy shipping to USA – canadapharmacyonline com

The Real Person!

The Real Person!

mexican mail order pharmacies: mexico pharmacies prescription drugs – mexico drug stores pharmacies

mexican online pharmacy mexican online pharmacy mexican online pharmacy

Rx Express Mexico: mexican online pharmacy – Rx Express Mexico

The Real Person!

The Real Person!

pharmacies in mexico that ship to usa: Rx Express Mexico – RxExpressMexico

The Real Person!

The Real Person!

пинап казино: пин ап вход – pin up вход

The Real Person!

The Real Person!

вавада официальный сайт: vavada – vavada casino

The Real Person!

The Real Person!

vavada: вавада – vavada

The Real Person!

The Real Person!

пин ап казино: пин ап казино – пин ап зеркало

The Real Person!

The Real Person!

pin up вход: пинап казино – пин ап казино официальный сайт

The Real Person!

The Real Person!

пин ап зеркало: пин ап вход – пинап казино

The Real Person!

The Real Person!

pin up az: pin up – pin up casino

The Real Person!

The Real Person!

вавада официальный сайт: вавада зеркало – вавада официальный сайт

pin up azerbaycan: pin up – pin up

pin up casino: pin-up – pin-up casino giris

vavada casino: vavada casino – vavada вход

пин ап зеркало: пин ап казино – пин ап вход

вавада официальный сайт: vavada вход – vavada

пин ап казино: пинап казино – пин ап казино

вавада казино: vavada – vavada вход

пин ап зеркало: пин ап казино – пин ап казино официальный сайт

pin up вход: пин ап зеркало – пин ап зеркало

pinup az: pin up casino – pin up casino

pin up вход: пин ап казино официальный сайт – пин ап казино

pin up az: pin up az – pin up azerbaycan

The Real Person!

The Real Person!

http://pinupaz.top/# pin up casino

The Real Person!

The Real Person!

https://pinupaz.top/# pin up casino

The Real Person!

The Real Person!

no doctor visit required: trusted Viagra suppliers – buy generic Viagra online

The Real Person!

The Real Person!

best price for Viagra: safe online pharmacy – no doctor visit required

The Real Person!

The Real Person!

safe modafinil purchase: verified Modafinil vendors – purchase Modafinil without prescription

The Real Person!

The Real Person!

secure checkout ED drugs: discreet shipping ED pills – order Cialis online no prescription

The Real Person!

The Real Person!

safe modafinil purchase: modafinil legality – modafinil pharmacy

The Real Person!

The Real Person!

online Cialis pharmacy: FDA approved generic Cialis – cheap Cialis online

The Real Person!

The Real Person!

trusted Viagra suppliers: best price for Viagra – safe online pharmacy

The Real Person!

The Real Person!

trusted Viagra suppliers: same-day Viagra shipping – generic sildenafil 100mg

https://modafinilmd.store/# doctor-reviewed advice

The Real Person!

The Real Person!

modafinil legality: buy modafinil online – verified Modafinil vendors

legal Modafinil purchase: purchase Modafinil without prescription – buy modafinil online

The Real Person!

The Real Person!

verified Modafinil vendors: verified Modafinil vendors – doctor-reviewed advice

https://maxviagramd.shop/# no doctor visit required

The Real Person!

The Real Person!

purchase Modafinil without prescription: legal Modafinil purchase – legal Modafinil purchase

http://modafinilmd.store/# Modafinil for sale

buy modafinil online: Modafinil for sale – doctor-reviewed advice

The Real Person!

The Real Person!

affordable ED medication: Cialis without prescription – discreet shipping ED pills

http://zipgenericmd.com/# secure checkout ED drugs

The Real Person!

The Real Person!

doctor-reviewed advice: legal Modafinil purchase – modafinil legality

The Real Person!

The Real Person!

buy prednisone online india: PredniHealth – prednisone 5 mg tablet

The Real Person!

The Real Person!

Amo Health Care: Amo Health Care – Amo Health Care

The Real Person!

The Real Person!

order generic clomid: cost generic clomid pill – how to get generic clomid without dr prescription

The Real Person!

The Real Person!

buy amoxicillin online mexico: Amo Health Care – cost of amoxicillin

buying generic cialis: over the counter cialis 2017 – tadalafil medication

cialis professional ingredients: Tadal Access – liquid tadalafil research chemical

brand cialis: TadalAccess – dapoxetine and tadalafil

buy antibiotics over the counter Biot Pharm Over the counter antibiotics for infection

PharmAu24: Pharm Au24 – Online drugstore Australia

Online medication store Australia: Medications online Australia – Pharm Au24

https://eropharmfast.com/# Ero Pharm Fast

Ero Pharm Fast ed meds cheap erectile dysfunction pills for sale

online ed pharmacy: ed prescription online – Ero Pharm Fast

Pharm Au 24: online pharmacy australia – Licensed online pharmacy AU

buy antibiotics online: Biot Pharm – buy antibiotics from canada

Ero Pharm Fast Ero Pharm Fast cheap ed medication

Pharm Au24: Online medication store Australia – Online medication store Australia

https://eropharmfast.com/# where to buy ed pills

best online doctor for antibiotics: BiotPharm – buy antibiotics

online erectile dysfunction prescription: online ed pills – Ero Pharm Fast

Ero Pharm Fast: Ero Pharm Fast – Ero Pharm Fast

https://eropharmfast.com/# ed online pharmacy

best online doctor for antibiotics BiotPharm buy antibiotics from india

low cost ed meds: cheap ed pills online – Ero Pharm Fast

best online doctor for antibiotics: Biot Pharm – buy antibiotics

Over the counter antibiotics pills buy antibiotics get antibiotics quickly

https://eropharmfast.com/# online ed medication

buy antibiotics online: buy antibiotics from india – cheapest antibiotics

Discount pharmacy Australia Pharm Au 24 Online medication store Australia

The Real Person!

The Real Person!

Descansa en nuestras camas boxspring, camas para niños, camas queen y king, con colchones de diversas medidas y marcas reconocidas como Dr. Dream y Serta. Complementa tu sueño reparador con almohadas y ropa de cama de última tendencia. Política de reembolsoss ¡Juegue con dinero real y gane en royal Balloon 1win! ¡La rentabilidad de los pagos (RTP) es del 95-98%! Se trata de una cifra excelente para un juego en línea. El objetivo del Balloon viene del nombre – el jugador tiene que inflar el globo tanto como sea posible y no dejar que estalle. A medida que se infla el globo aumenta el coeficiente por el que se multiplicará la apuesta. El objetivo del juego es retirar el dinero antes de que el globo estalle. Una de las características más atractivas de esta aplicación son sus bonos y promociones. Al descargar la Balloon App ganar dinero descargar, los usuarios pueden acceder a promociones exclusivas, como bonificaciones por registro, recompensas diarias y eventos especiales. Estas ofertas son ideales para maximizar tus ganancias mientras disfrutas del juego.

https://smkalfatah-bna.sch.id/descubre-el-juego-en-linea-balloon-de-smartsoft-diversion-sin-limites-para-jugadores-colombianos/

You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. El RTP de Sweet Bonanza Candyland varía entre el 91,59% y el 96,83%, dependiendo de si se ha aplicado el Sugar Bomb Booster. En la ruleta hay 54 segmentos. Aquí tienes un desglose de cada posibilidad y pago: ©2025.Liffey Group. All Rights Reserved. You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. Sweet Bonanza 1000 es una tragaperras de caramelos creada por Pragmatic Play. Es la continuación de la Sweet Bonanza, original del mismo estudio. Como Hacer Para Ganar En El Tragamonedas

The Real Person!

The Real Person!

A marca tem vários acordos de patrocínio com torneios como o Brasileirão e times como o FC Porto, portanto, é renomada e segura. Ao baixar o app Betano, você ainda tem a chance de receber promoções surpresa exclusivas periodicamente. O download do F12 Bet pode ser feito por qualquer usuário. Para isso, basta seguir os breves passos descritos neste artigo. Acompanhe nossas redes sociais A marca tem vários acordos de patrocínio com torneios como o Brasileirão e times como o FC Porto, portanto, é renomada e segura. Ao baixar o app Betano, você ainda tem a chance de receber promoções surpresa exclusivas periodicamente. Acompanhe nossas redes sociais O app do F12 Bet está nas principais buscas dos apostadores e fãs dessa casa de apostas e cassino online com foco no Brasil. Mas apesar de toda a busca, ele não está disponível no momento!

https://swaay.com/u/certooidurchme198250381/about/

O que: Inscrições para O Rock na Praça 2022 © Loja dos POP’s 2025. Todos os direitos reservados. Salvar meus dados neste navegador para a próxima vez que eu comentar. Os roqueiros KISS venderam o seu nome, catálogo musical, logótipo, imagem e direitos de semelhança ao grupo Pophouse Entertainment, a empresa por trás do popular espectáculo de avatares dos ABBA. De acordo com a Fortune, a banda vai receber mais de 300 milhões de dólares da empresa sueca, que está a planear usar a mesma tecnologia para lançar um espectáculo de avatares da banda nova-iorquina nos Estados Unidos. Está em ? Confirme o país. $132.00 You are using an outdated browser. Please upgrade your browser to improve your experience. Gene Simmons, conhecido como The Demon, surpreendeu os fãs ao apresentar um lado mais suave e romântico em seu álbum solo.

The Real Person!

The Real Person!

Dragon Tiger Club is an online gaming platform that specializes in providing a unique and immersive gaming experience. The club offers a range of exciting games, including Dragon Tiger, Roulette, and more. With its sleek and user-friendly interface, Dragon Tiger Club provides an engaging and entertaining experience that’s perfect for players of all skill levels.app Dr tiger game Lightning Storm Lightning Sic Bo Not only good gameplay, but Ubisoft also does not forget to ignore factors such as images and sound. You cannot underestimate hack Hungry Shark Evolution because of its outstanding quality. With 3D graphics combined with catchy sound to create unique chases. Dragon Vs Tiger predict GPT tool offers a variety of features for supporting users such as: MOD V2: PK68 VIP offers a variety of games like Teen Patti, Rummy, Dragon vs Tiger, Fruit Classic, Rocket, and more

https://benhvienoto.vn/stunning-roi-with-the-best-aviator-game-by-spribe-an-indian-players-review/

Flag any particular issues you may encounter and Softonic will address those concerns as soon as possible. Immerse yourself deeply in the excitement of the Rummy Sun game and seize the golden chance to claim an impressive bonus of ₹51. This generous bonus allows you to indulge properly in extended gameplay, strategize your moves, and enhance your chances of winning big. Don’t let this opportunity slip away – grab your free ₹51 rummy bonus and elevate your rummy experience to new heights and that too non-stop! Ans. You can get dashboard this Rummy Perfect Game. The company has been approved playing 41 types of games in this app. Min. Withdrawal ₹100 – 2M+ | Bonus ₹51 Bonus ₹05 – A casual poker game that is best for beginners A23 Rummy Apps is one of the popular rummy bonus apps that promise to a bonus of upto Rs 1500 instant cash. A23 has 10 million plus downloads on PlayStore and offers a 100% bonus plus Rs 125 instant cashback. So if you add Rs 500 first deposit in the A23 Rummy app then you will get back Rs 625. There are more chances to win a bonus upto Rs1500. So pick up your phone, download the A23 rummy app from the link down below, and play to win multiple cash rewards and bonuses.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

The Real Person!

The Real Person!

Aviator game offers an innovative gaming experience unlike, slot machines. The game has no reels or paylines, which makes it different from other gambling games. Players can rely on luck or play strategically. In our opinion, Aviator gives a unique gaming experience and excitement in every round. The developer of Space XY cooperates only with licensed online casinos. In these casinos, bonuses are not usually subject to extreme wagering requirements. The client of the online casino can easily win back the gift received without large bets. As the aircraft climbs higher, the potential winnings continuously increase. Players must strategically cash out their bets before the aircraft disappears from view. Your final payout is calculated by multiplying your initial stake with the coefficient at the moment you cash out. The game’s unpredictability lies in its mysterious round endings.

https://postgresconf.org/users/179639

Pin up Aviator es un gran juego de azar en el que podrás realizar tus apuestas con dinero real, retira a tiempo antes de que el avión se estrelle para obtener ganancias, en caso contrario perderás tu apuesta. Las transacciones financieras utilizadas para depositar o realizar retiros de dinero se hacen en la moneda local oficial, los pesos chilenos u otra moneda de curso legal. Las operaciones son encriptadas bajo estrictos parámetros de seguridad para el mayor beneficio de sus usuarios. In the second book of the Capital Mysteries—an early chapter book mystery series featuring fun facts and famous sites from Washington, D.C.—KC and Marshall are going to the Cherry Blossom Festival…. Entre los casinos online con dinero real que se especializan en apuestas para tragamonedas. Además, tienen una nutritiva cantidad de bonos dedicados a los juegos de slots que atraen a muchos nuevos usuarios.

The Real Person!

The Real Person!

Desafía tus habilidades de precisión y potenciate al enfrentarte a arqueros virtuales que están listos para detener tus mejores intentos. Con gráficos realistas y una jugabilidad envolvente, te sentirás como si estuvieras en el estadio, bajo la presión de la multitud y con todo en juego. Habilidad con el ratón Para jugar a Penalty Shoot Out en Betwinner, inicia sesión en tu cuenta de Betwinner, navega a la sección de casino y busca el juego. Establece tu apuesta, elige hacia dónde apuntar tu tiro, e intenta marcar. También puedes utilizar la función de juego automático para un juego continuo. Insertar Penalty Power Necesitas talento, estrategia y suerte para imponerte en la “Tanda de penaltis”. Estas sugerencias pueden ayudarte a jugar mejor: quien perdio en la final con Portugal 5-0 Alemania

http://eudat1.deic.dk/user/svormepate1979

En este nuevo juego de los 70, 80 y 90. ¿No hay un 10 del crupier? Este sistema no está de tu elección. No necesitas la app de nuestro bono sin depósito varias veces. La entrada diaria es de 0.1 € y la fábrica de chocolate. DE Sistema: esta empresa ha sido adaptado con éxito las misiones principales. Existen varias opciones del tapete, entre los aficionados a las tragaperras y ruletas con crupier en directo. Horario at. telefónica: Lunes a Viernes – 9 a 14 y de 16 a 18h Cuando hablamos de juegos de fútbol, como es el juego de penales, estos permiten experimentar partidos de fútbol competitivos y llenos de adrenalina en la comodidad del trabajo, hogar o cualquier lugar. ‘ + gameplay_flash_message + ‘ } } Tanda de penales de la Copa del Mundo Penalty Shoot-Out generalmente cuenta con un RTP (Retorno al Jugador) competitivo de aproximadamente 96%. Este porcentaje representa la cantidad promedio de dinero que Penalty Shoot-Out devuelve a los jugadores a lo largo del tiempo. Indica que el juego ofrece probabilidades favorables, lo que lo convierte en una opción atractiva para aquellos que buscan maximizar sus posibilidades de ganar.

The Real Person!

The Real Person!

Teen Patti Master App Details: As previously mentioned, TeenPatti Gold is based on the Indian card game known as Teen Patti, which is influenced by three-card brag and poker. Indians typically play this as a social activity because it’s part of their culture, particularly around Diwali, or the Festival of Lights. You can play both the original game and all of its variations in one place with this app. Warning: This game involves financial risk. Users are advised to download and use the app responsibly and at their own risk. Do not add money if you don’t want to risk. We are not responsible for the app. I will create crash game blackjack teen patti poker board game baccarat ludo rummy game Teen Patti, also called 3 Patti, is a popular card game from India, similar to 3 Card Brag and Poker. Known as Flush or Flash, it’s loved for its simple rules and exciting gameplay. Teen Patti, also known as the Indian Poker, is a common choice during social events and festivals and is now popular online too. Many platforms offer teen patti real cash game downloads, where you can play with friends or compete online to earn real money.

https://gaidemusmo1979.bearsfanteamshop.com/https-ca-sweetbonanza-ca

Sweet Bonanza is available in all top casinos in Canada because it’s the most popular fruit-themed slot worldwide. The Xmas version is no different – offering 10 low to high-paying symbols ranging from candy to fruit symbols, Free Spins are on offer and require at least 4 swirly lollipop scatters to trigger them. The bonus round starts with 10 free spins, but 3 or more scatters will add 5 more to the remaining tally. During free spins, the multiplier symbol comes into play. When it lands, it stays on screen while wins tumble, and at the end, any multipliers in view will be added up and applied to the winning total. The multiplier values start at x2 and can go as high as x100. The scatter also pays out 3x, 5x, and 100x when 3, 4, or 5 land in view on the grid. Find out how the Sweet Bonanza Xmas slot behaves when you play tens of thousands spins. What are the chances of getting net winnings, how does the balance change, what payouts land and how often:

The Real Person!

The Real Person!

◉ Table Games: Enjoy a diverse range of classic casino games like blackjack, roulette, and poker.◉ Live Games: Engage with live dealers for a real-time, immersive gaming experience.◉ Slots: Discover over 1,600 games, including exclusive Stake Originals and top titles from leading providers.◉ Sports Betting: Bet with competitive odds, enjoy real-time updates, and live-stream your favorite events.◉ Rewards and Bonuses: Earn exciting rewards, claim bonuses, and participate in exclusive prize draws. Sweet Bonanza You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. Goldrush offers a diverse range of unique, entertaining and captivating slot games from renowned providers, including Pragmatic Play, NETENT, RED Tiger, EGT DIGITAL, NETGAMING, G.GAMES. Yggdrasil and Spinomenal.

https://forum.bug.hr/forum/user/mortnolphdiscted1988/145033.aspx

Pop open Christmas Big Bass Bonanza’s tackle box of features to find a round of free spins where money symbols and wilds may be collected to score cash prizes or trigger extra spins and multipliers. We have all the most popular slot variations including Megaways, Slingo, and jackpots galore. Discover thousands of ways to win in titles like Eye of Horus Megaways and Big Bass Bonanza Megaways, learn the Slingo lingo with titles like Slingo Rainbow Riches or jump on the Jackpot train with progressive jackpot titles including Jackpot King and Must Win Jackpots. The Santa Claus wild symbol is activated once the free spins round begins, and it offers several special features, such as substituting for all symbols except the Christmas fish. More importantly, it helps you get extra free spins and triggers increasing multipliers. During the free spins, Santa’s Wilds can also collect cash values from fish symbols. All these cash values will be added as prizes to your win. Every fourth Wild Santa rewards you with an extra ten spins, and you can re-trigger this feature up to three times with multipliers increasing in value up to 10x.

The Real Person!

The Real Person!

Bigger Bass Bonanza gives players a chance to get on a fishing expedition chasing that bigger ocean fish. The game features a range of symbols, each offering different payouts depending on the number of matches landed. Also, there’s the fisherman symbol that serves as the wild, substituting for all symbols except the scatter. 2Big Bass Splash The show-stopping RTP combined with high volatility make Bigger Bass Bonanza a great find for mathematically minded players. Sweet Bonanza Activate bonus in your casino account Activate bonus in your casino account As you play Big Bass Bonanza, there are lots of exciting bonus features that could help you reel in a big win: To start playing the Bigger Bass Bonanza slot you don’t need to go deep into your pockets. The initial bet can be $0.12, but whales who like to splash big can have their day also with this game, and enjoy the maximum bet of $240.

https://ckan.obis.org/user/singservwaffbur1982

The Razzies don’t care about your A-list status, but then I feel oppressed. Interactions of Big Bass Bonanza Hold and Spinner depending on spins games coming from a range of leading software providers are a definite plus and make things even more engaging, as the tribe intends to build the casino on community trust land just outside the southern border of Chandler. 1Big Bass Bonanza Megaways The Razzies don’t care about your A-list status, but then I feel oppressed. Interactions of Big Bass Bonanza Hold and Spinner depending on spins games coming from a range of leading software providers are a definite plus and make things even more engaging, as the tribe intends to build the casino on community trust land just outside the southern border of Chandler. Ed abroad is the trusted study abroad consultant in Ernakulam Kochi, fully committed to providing free study overseas consultation for students looking for overseas education. We support the students by providing the up to date information and offering our assistance in completing Application formalities, Visa guidance, Scholarship Guidance, and assistance for Educational loans.

The Real Person!

The Real Person!

achasfoundationinc.org slot-bet-200 Situs slot terpercaya menjamin pengalaman bermain yang aman dan nyaman untuk semua pemain. Dari transaksi hingga dukungan pelanggan, semuanya dirancang untuk memberikan yang terbaik. jeedad how-to-play-spaceman Situs slot terpercaya menjamin pengalaman bermain yang aman dan nyaman untuk semua pemain. Dari transaksi hingga dukungan pelanggan, semuanya dirancang untuk memberikan yang terbaik. sooniandtommi situs-judi-bola Situs slot terpercaya menjamin pengalaman bermain yang aman dan nyaman untuk semua pemain. Dari transaksi hingga dukungan pelanggan, semuanya dirancang untuk memberikan yang terbaik. Dengan berbagai keuntungan, jackpot besar, dan pengalaman bermain yang tak tertandingi, tidak ada alasan untuk menunda bergabung dengan situs slot terbaik tahun 2025. Mulai perjalanan Anda hari ini dan nikmati sensasi bermain slot dengan peluang menang besar. Daftar sekarang dan semoga keberuntungan selalu menyertai Anda!

https://riverfrontsolutions.com.au/review-completo-do-dragon-tiger-luck-da-pg-soft/

Os grupos de Telegram Spaceman de informações podem ser uma ótima fonte de conhecimento e aprendizado para quem está começando a jogar o jogo, bem como para jogadores mais experientes que desejam aprimorar suas habilidades. Os membros desses grupos geralmente compartilham informações sobre como jogar o jogo de forma mais eficaz, quais as melhores estratégias para vencer e como evitar cometer erros comuns. Enquanto os jogadores brasileiros estiverem procurando maneiras de melhorar suas chances de ganhar, eles podem recorrer aos Spaceman sinais gratuitos do grupo para prever os resultados do jogo. É o software que pode ajudar a aumentar as chances de ganhar reais brasileiros sem inventar estratégias ou ter qualquer habilidade de jogo. GRUPO FREE 🤑🤖🚀📌 Você não vai perder essas vantagens, né? Então clique no banner exclusivo que preparamos especialmente para você e ative o código de indicação Betano BETEM na hora do registro!

The Real Person!

The Real Person!

The demo mode in Colour Trading is a great way to test the game in conditions close to reality without risking any money. You can try out different strategies, get a better feel for the game mechanics, and decide if the Colour Trading app really suits you. Remember that demo mode does not offer real-money winnings, but it helps you understand the game better and prepare for real bets. Laptop Exchange is only applicable upon purchasing a HP laptop from the HP Online Store, and upon completing your device evaluation form — available via the Cashify option on the HP product page. To learn more about the BharatClub app, you can read the Bharat Club Blog. Here you will get to see all the information about the BharatClub games. Also, if you read Bharatclub Blog, you will get to know a lot about the gaming world. You will learn something that you can use in your game.

https://www.encon.com.tr/what-makes-lucky-3-patti-gold-different-in-live-play/

✪ Guide for MPL Pro Apk Download : Guide for mpl earn money from mpl cricket fantasy with football game guide is provide. This app is provide mpl game app download facility. Cricket 100x is a fun game that mixes cricket with quick quizzes. You choose cells on a 3×3, 4×4, or 5×5 grid to make your moves. Try to hit the targets without getting out to win more money. Play this online cash game and win real money! You can also visit our official website at Teen Patti Stars Teen Patti Flush ! Free mobile Teen Patti game Funny Teenpatti Teen Patti Dhani – GO: A Modern Twist on the Traditional Card Game TeenPatti Yono-3Patti Rummy: Strategy Meets Luck From selling products to completing surveys to gaming and refer & earn, money making apps in India are providing financial freedom. Whether you want to make some extra money in your spare time or are looking for flexible work opportunities, the apps below can help you turn your handset into a money-making machine. Come join us to learn about the game-changers that can fill you r wallet.

The Real Person!

The Real Person!

This game’s return to player (RTP) rate is 97%, which is higher than the average online slot RTP rate of around 96%. However, the provider does not disclose Space XY’s true volatility rate. Different sources report varying volatility levels, with some indicating medium volatility and others high volatility. Based on extensive gameplay, we have observed that Space XY has the potential for huge wins and instant losses, leading us to conclude that this game likely has high volatility. Odds are the most important part in gaming, and the website is blessed with clear and deep detailed odds about every game and event. The odds are useful in telling how much a bet can be able to win. Updates of the odds are provided in real time; versatility confirms that you are well-informed while deciding your place in the daily events of gaming. A better understanding of odds helps in gameplay between teams, favorites, or underdogs.

https://dev-dl-wpplus.pantheonsite.io/2025/07/03/exploring-the-aviator-ios-experience-what-players-from-namibia-should-know/

Teen Patti Sweet provides a great gaming experience for enthusiasts of the classic Teen Patti card game. Its user-friendly interface, free tournaments, and generous complimentary bonus chips make it an ideal platform for players of all levels. Its advanced technology ensures fair gameplay and plenty of entertainment for players. Overall, it is an excellent option for anyone looking to spend hours playing the card game on their personal devices. If you want to try your luck playing virtual card games, download 3 Patti Circle. Online earning apps give users a way to earn money by using their skill sets, performing different tasks, or providing services. Through these free money earning app, users can find possibilities to sell products, do surveys, work as freelancers, watch ads, or engage in reward-based activities.

The Real Person!

The Real Person!

Aviator’daki bir başka şema da her turda desen arayışıdır. Oyun tamamen şansa dayalı olsa da, bazı oyuncular bir uçağın ne kadar süre uçtuğuna dair kalıpları belirleyebildiklerini iddia ediyor. Ancak, bu stratejinin güvenilir olmadığını ve dikkatle kullanılması gerektiğini unutmamak önemlidir. Tüm paranızı kaybedebileceğiniz gibi. Örnek senaryo şu şekilde olabilir: Bir uçuş ekibi, hava trafiği yoğun bir alanda seyir halindeyken, hızlı bir şekilde bir başka uçuş ekibiyle iletişim kurmak zorunda kalır. Bu durumda Aviator Signal Telegram kullanarak, diğer ekibe hemen bir mesaj gönderebilir ve anında yanıt alabilirler. Bu hızlı itişim, uçakların güvenliğini sağlamak için kritik bir öneme sahiptir.

https://dhetinvest.com/uncategorized/pin-up-aviator-demo-rejimi-il%c9%99-risk-analizi/

Os jogos de azar online estão se tornando cada vez mais populares, e um dos mais emocionantes é o Aviator Betano. Combinando sorte e estratégia, este jogo é uma ótima opção para os entusiastas que buscam emoção e entretenimento. Como eu já disse, no Aviator, os outros jogadores ficam visíveis no lado esquerdo da tela ou na parte inferior em telefones e tablets. Nessa área, você pode ver todas as apostas feitas no jogo, inclusive as suas e as de outras pessoas. Há também uma seção dedicada aos maiores ganhos já obtidos no Aviator. Essa é uma lista extensa, que você pode conferir na íntegra na página do Ministério da Fazenda. Ainda, a SAP desenvolveu a plataforma Sistema de Gestão de Apostas (SIGAP), dedicada a prestar informações sobre as casas autorizadas. Logo, essa é uma fonte de dados interessante e segura.

The Real Person!

The Real Person!

Turbo Golf Racing has a reliably simple premise: use a car to get a large ball into a goal as quickly as possible. Thankfully, the execution of that premise is also usually quite reliable. In my experience with the title, I never found controlling my car to be unreasonably difficult, with driving and gliding around both offering responsive controls and satisfying speed. I did however notice that other players online — including some of my own friends — sometimes seemed to have major issues with losing control over their vehicles, though I never personally experienced this issue. Infinite rim height adjustment can be made with the easy crank handle located on the back of the vertical mast. The rim height indicator labels determine rim heights from 10′ to 6’6″. The Rampage uses our exclusive crank-up design, which is far superior to similar goals using “spring-slide” methods.

https://blochi.at/where-to-play-mine-island-slot-in-2025-verified-sites/

This goal is stoutly constructed. We will use it on the beaches of NorCal to repel any North Korean amphibious landings. GOAL takes a look at the biggest transfer news and rumours from around the world Bears quarterback Caleb Williams finds wide receiver DJ Moore for 18 yards and spikes the ball to set up Cairo Santos’ game-winning field goal. ©2021-2022 New Star Games It is not possible to load the page you were looking for on KNVB. BOTTOM LINE: The Toronto Maple Leafs visit the San Jose Sharks after William Nylander’s two-goal game against the Philadelphia Flyers in the Maple Leafs’ 7-2 win. Instead of offering you a shipping deal one week then taking it away the next, we offer the same free shipping deal 365 days a year. So you can order when you need it, instead of waiting to time your order to match a retailer’s promo schedule.

The Real Person!

The Real Person!

Lolly’s zijn speciale symbolen bij de Sweet Bonanza gokkast. Met minimaal vier lolly’s wordt er toegang gegeven tot het bonusspel. In deze bonus wordt in een iets andere omgeving gespeeld, maar de wijze waarop het spel wordt gespeeld is niet veranderd. Een verschil is wel dat de snoepjes nu als vermenigvuldigers fungeren. Sweet Bonanza kan voor geld gespeeld worden bij vrijwel alle Nederlandse online casino’s. Een vereiste is dat ze natuurlijk de gokkasten van Pragmatic Play in hun assortiment hebben opgenomen. Gelukkig hebben de meeste legale aanbieders een overeenkomst met Pragmatic Play. Hij is dan ook enorm opgelucht als er weer vier lolly’s verschijnen. Helaas eindigt de tweede bonusronde met het teleurstellende bedrag van €1,41. De bonus van Sweet Bonanza kan dus heel veel, maar ook heel weinig opleveren.

https://regasestearmonia.ro/sweet-bonanza-review-een-zoete-kans-voor-nederlandse-spelers/

sweet bonanza 1st: sweet bonanza yorumlar – sweet bonanza yorumlar sweetbonanza1st.shop Bahis Sitelerinde en çok tercih edilen slot oyunları arasında yer alan Sweet Bonanza Gates of Olympus, Flaming Hot ve Book of Ra Matadorbet bahis sitesinde de yer almaktadır. Aynı zamanda, InstaTakipci, kendi endüstrisindeki en ucuz fiyat aralıklarını sunmak için sürekli çalışıyor. Siz müşterilerimizi memnun etmek için elimizden gelen her şeyi yapmaya devam edeceğiz. Kaliteli hizmet politikamızdan hiçbir zaman vazgeçmeyeceğimizi siz değerli müşterilerimize taahhüt ediyoruz. İnstagram organik takipçi satın al hizmetimiz ile hesabını yükselişe geçirmeye hazır ol! Güvenilir, ucuz ve organik instagram takipçi satın al hizmeti sunan sitemiz ile kaliteli takipçi satın alma paketlerinin tadını çıkar. İnstagram takipçi satın al hizmetimizi kullanmaya başlamak için 4 yıldır hizmet verdiğimiz instagram takipçi satın alma sitemizi ziyaret edebilirsiniz.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

The Real Person!

The Real Person!

Sendo assim, com base em nossas análises e testes, o cacaniquel fortune rabbit tem sim alguns minutos durante todo o dia que ele costuma dar mais dinheiro para as pessoas. É possível ver diversas pessoas que jogam Fortune Rabbit o jogo do coelho e conseguem ganhar dinheiro com a banca baixa (pouco saldo). Conseguindo fazer ganhos incrivelmente muito altos comparado ao que foi apostado. Minutos pagantes do Fortune Rabbit são períodos de tempo em que os jogadores têm a impressão de que os pagamentos são mais frequentes. Esses minutos pagantes podem ocorrer pela manhã, à noite ou até de madrugada. É recomendável que jogue com caltela e se possível, siga uma sala de sinais ou jogue sempre nos horários pagantes do Fortune Rabbit.

https://duoclieubaokhangduong.com/fortune-tiger-bonus-como-desbloquear-e-utilizar-para-maximizar-ganhos-no-jogo-do-tigrinho-da-pg-soft/

Por exemplo, no caça-níquel original, você terá várias linhas de ganho que podem ser vertical, horizontal e diagonal. Porém no bonanza quando 3 ou mais símbolos se juntam, eles desaparecem da tela, você ganha pontos e o jogo se reorganiza caindo mais peças. Caso 3 ou mais se juntem novamente o jogo continuará tirando as peças e dando pontos. Por último, mas não menos importante, lembre-se sempre da importância do jogo responsável. O Sweet Bonanza é uma experiência divertida e emocionante, mas é essencial jogar com moderação e dentro dos seus limites. Estabeleça um orçamento claro, defina limites de tempo e nunca jogue com dinheiro que você não pode perder. O pagamento máximo para o Sweet Bonanza é de 21.175x em base ao valor apostado. Esse recurso não é contabilizado no seu saldo em caso de que você esteja jogando o Sweet Bonanza grátis. Contudo, há também momentos em que o apostador se encontra com rodadas grátis e multiplicadores. Entre as Sweet Bonanza orientações que podemos dar estão:

The Real Person!

The Real Person!

Los usuarios de apuestas deportivas pueden usar sus credenciales de inicio de sesión para el Casino en línea Parx, son falsificaciones y te quitarán dinero y tiempo. Si bien el póquer en línea regulado de Pensilvania aún no está disponible porque la legislación que lo habilita se aprobó recientemente a fines de 2023, como el Blackjack y el póquer en vivo. Además, por supuesto. Es uno de los lugares más seguros de la India y ofrece juegos de azar a través de aplicaciones para Android e iOS, cómo jugar a las tragamonedas big bass bonanza pero si puede encontrar algunos para YouWager Casino antes de unirse. Dos ladrones se esconden en cada carrete, Primal Megaways o Slots OGold Megaways de forma gratuita.

https://fallcreekacupuncture.com/2025/07/12/compatibilidad-multiplataforma-del-juego-balloon-de-smartsoft-juga-donde-quieras/

Additionally, the reside sports interface will be furthermore convenient plus lets the punters enjoy live betting applying each desktop computer and cellular. The Particular odds provided on the live sporting activities events are usually competing and supply a great margin. This Particular indicates punters can win big inside a short period after inserting live wagers. Furthermore, typically the bookie even gives free-of-cost reside avenues to typically the registered customers. The Particular 1xBet casino software provides an impressive gaming experience along with over two,000+ online casino video games and current marketing promotions. The biggest bonus is the one you can give yourself when you applying what I’m going to teach you. So your BONUS is the incredible life that awaits you by achieving mastery in network marketing!

The Real Person!

The Real Person!

Para ter acesso a plataforma oficial, segura e confiável do Jogo do Touro, Clique em “começar” na imagem abaixo para ser redirecionado (a) automaticamente. Onde assistir ao vivo? A partida será transmitida pelo sportv (TV por assinatura) e Premiere (pay-per-view). Confira abaixo os horarios pagantes Fortune Ox para jogar o famoso jogo do Touro, Fortune Ox: Existem dois recursos especiais em Fortune Ox, o recurso Touro da Sorte, que é uma vitória garantida, e o multiplicador de ganhos de 10x para uma grade completa do mesmo item. Para isso, além de seguir as estratégias mencionadas, também é importante aproveitar ao máximo as funções do jogo e a faixa de aposta para maximizar os ganhos sem comprometer o orçamento. Tente jogar Fortune Ox no modo demo para familiarizar-se com o jogo antes de investir dinheiro real.

https://klcmarketingsales.com/2025/07/14/fortune-rabbit-uma-analise-completa-do-jogo-online-da-pg-soft/

O Fortune Ox é um jogo que chama a atenção pelo seu design e simplicidade. No tocante aos ganhos, pode-se dizer que o jogo do touro tem um equilíbrio perfeito de retorno ao jogador (RTP) e volatilidade – fazendo pagamentos em um nível intermediário, perfeito para apostas baixas e constantes. Agora que já sabe onde e como apostar no Fortune Tiger, pode escolher uma operadora e fazer o seu cadastro. Mas, se ficou com alguma dúvida, abaixo respondemos às perguntas mais frequentes sobre este jogo. O Fortune Tiger Demo foi desenvolvido para funcionar em diversas plataformas, incluindo dispositivos móveis. O jogo do tigrinho demo mantém alta qualidade e interatividade em smartphones e tablets, enquanto a demo fortune tiger garante uma experiência prática e fluida para os usuários.

The Real Person!

The Real Person!

AlphaProductos ligeros y minimalistas para escaladas y alpinismo que ofrecen protección en entornos alpinos. En cuanto a la seguridad de los juegos, se utiliza una polea – sistema suizo Saferoller- que engancha a la persona al cables de seguridad permanentemente, desde que se ingresa en un circuito. Hay diferentes niveles divididos por altura mínima. Por ejemplo, los chicos de entre 1,25 y 1,40 pueden jugar únicamente en los cuatro primeros niveles. Los que llegan a 1,60 pueden ingresar hasta el nivel 6. Los más chiquitos -1 a 1,20 metros- tienen EUCA Mini, un circuito más sencillo al que también se ingresa con arnés, casco y gancho de seguridad. A medida que avanzamos en el juego, las locaciones se transforman poco a poco más similes a una nueva dimensión, incluso vemos detalles del culto en todos lados que alaba al Omnividente. Tanto la geografía como las ruinas nos dan indicios de donde nos situamos y los enemigos se reemplazan lentamente en abominaciones de otro plano. Incluso podemos ver a los Jefes interactuando con nosotros, interfiriendo en el escenario, hasta finalmente adentrarse en la batalla para ponernos un freno. Sus diseños se emparejan con la personalidad, la dificultad y la mecánica del jefe, cambiando según el daño que estos presentan y las habilidades que ejerzcan.

https://ciclou.app/balloon-en-modo-casino-dinamica-graficos-y-pagos/

Los fanáticos de las apuestas en deportes se benefician de la oferta principal que es la de bienvenida. Con un generoso monto de hasta 125% extra de su depósito luego de la inscripción. Los usuarios pueden disfrutar de grandes ventajas. Otra disciplina con popularidad en muchos países. En Pin Up se encuentran 10+ eventos pre partidos en este deporte. Aunque muchas veces suelen elevar este número dependiendo de la cantidad de ligas importantes que se estén llevando a cabo. El Domingo de Resurrección, la cofradía de Jesús Resucitado visitará el primer templo a las doce del mediodía. Pinche abajo para tener acceso a esta magnífica retransmisión. This report deals with the broader developments in EU policy governing returns, including – the proposal for the new Returns Directive – the expansion of the mandate of Frontex and – the expansion and interconnection of EU databases and information system.

The Real Person!

The Real Person!

But what exactly makes the uncrossable mission stand out in the casino game world? It’s the perfect blend of skill and luck, offering players the chance to not only rely on their strategy but also enjoy the unpredictable nature of each game. Whether you’re aiming for casual fun or serious betting, Mission Uncrossable has something for everyone. Chicken Road is that gambling game that literally keeps you at the edge of your sit at all times. And the further you progress the more nerve-wracking each step. Because the stakes get higher since you accumulate better wins. Experience the thrill of aviator betting and watch your bets reach new heights. This Rootbet Cicken Game offers simple gameplay and rules that are easy to understand. However, adding a little Roobet Mission Uncrossable strategy to your gameplay can go a long way. These five helpful tips will help maximize your enjoyment of this game:

https://www.joergbrueggemann.com/official-payout-reports-for-aviator-released-whats-new/

It’s quite simple really – if you’re a die hard fan of the Big Bass series, Big Bass Amazon Xtreme offers another opportunity to get your feet wet. If you haven’t been convinced thus far, maybe x50 multipliers will be the thing to tempt you. If you are an extreme enthusiast of fishing who dreams of reeling in a big catch, then the Big Bass Amazon Xtreme slot is the perfect game for you. Developed by Pragmatic Play, this popular slot with an RTP of 96.07% and max. wint of 10,000x takes players on a thrilling adventure through the Amazon River, where lucrative fishing opportunities await. With its captivating graphics and engaging gameplay, you’ll play in demo mode and experience the thrill of fishing! COPYRIGHT © 2015 – 2025. All rights reserved to Pragmatic Play, a Veridian (Gibraltar) Limited investment. Any and all content included on this website or incorporated by reference is protected by international copyright laws.

The Real Person!

The Real Person!

Dzięki wysokiemu RTP i ocenie zmienności, wraz z zabawnym motywem i ekscytującymi bonusami, Sugar Rush to gra, której nie można przegapić. Animacje i grafika na pewno wprowadzą Cię w dobry nastrój, a potencjał na duże wygrane zatrzyma Cię w grze na wiele godzin. will you make a game about the new movie? Bonus Bez Depozytu Dla Jammin Jars Wszystkie opinie i pytania, które nie będą dotyczyły produktów, zostaną usunięte! Sugar rush kasyno baba Joga może również pomóc ci w grze podstawowej, że nie ma żadnych kar. Nie ma powodu, jeśli zdarzy ci się grać i wygrywać pieniądze. NOWE PROMOCJE JUŻ SĄ! Dodatkowe 10% | Code : LFSUMMER Jedną z najbardziej ekscytujących funkcji Sugar Rush jest bonus mnożnik. Z każdym wygrywającym symbolem, który pęka na pozycji, mnożnik wzrasta do x128. Gra oferuje również funkcję darmowych spinów, gdzie można zdobyć jeszcze więcej wygrywających kombinacji dzięki pomocy mnożników.

https://mediasuitedata.clariah.nl/user/loteddioboi1985

Automat Sugar Rush 1000 ma siatkę 7×7, na której znajdują się kolorowe cukierki i żelki jako płatne symbole. Podobnie jak inne automaty o tematyce cukrowej od Pragmatic Play, Sugar Rush 1000 wykorzystuje mechanikę Cluster Pays, która wymaga co najmniej 5 pasujących symboli połączonych pionowo lub poziomo. W przypadku zwycięskiej kombinacji symbole te eksplodują i są usuwane z siatki, a nowe spadają w dół, aby zająć darmowe automaty online w kasynie. Funkcja spadania trwa do momentu, gdy na ekranie nie będzie już pasujących symboli. Ahoric Fast Service is your trustworthy partner for global logistics solutions. Since our establishment, which aimed to simplify and streamline supply chain management, we have grown to become one of the leading logistics service providers, known for our dependability, efficiency, and attention to customer needs

The Real Person!

The Real Person!

Conecta con nosotros Big Bass Splash es una tragaperras de Pragmatic Play con una estructura de 5 rodillos, 3 filas y 10 líneas de pago fijas. Esta slot de temática pesquera cuenta con 10 símbolos regulares, 1 comodín (Wild) y 1 scatter. Big Bass Splash slot packs a heap-load of excitement per spin! To conclude our review, we’ve rounded up the special features of the game, including information on the Wild Symbol and Free Spins bonus. Una de las características principales de Big Bass Splash son los multiplicadores crecientes y los ascensos de nivel. A medida que juegas, puedes desbloquear diferentes niveles que te premian con multiplicadores de premios más altos. Esto agrega emoción y empeño al juego, ya que te motiva a alcanzar niveles más altos para obtener mayores ganancias.

https://paper.wf/famorinney1973/si-los-tandiacute-tulos-con-vikingos-son-tu-taza-de-tandeacute-y-north-storm

Envío GRATIS desde 50 € (Península) de forma online, venta online, consultas online y además nos puedes As their name suggests, deposit free spins require a payment. These are usually offered to players as a welcome bonus when they make their first deposit on the casino site. They can also appear as part of other deposit-based deals or standalone offers. The key thing to note is that you can claim free spins on selected slot games when you deposit to your account. Envío GRATIS desde 50 € (Península) Jugar Big Bass Bonanza Gratis El símbolo de dispersión de los juegos es un pirata esqueleto con la palabra Bonus escrita en él, y tiene dos características de incentivos excepcionales que aumentan sus posibilidades de éxito. Hay tres… Head to your chosen casino and register as a new player by hitting the Join Now, Register or Sign Up button. Enter your details in the form, accept the T&Cs and finish the procedure. At this stage, you may be asked to enter any relevant bonus code or tick a box to opt in for the no deposit bonus.

The Real Person!

The Real Person!

Łączna liczba punktów bonusowych, ale dobrze jest mieć na uwadze. Bonusy kasynowe 2025 – jeszcze więcej możliwości wygranej. Na rynku istnieje wiele kasyn online na iOS, dostępna jest bezpłatna wersja beta botów handlowych. Automat do gier sugar rush gra za darmo bez rejestracji ponadto, koncentrują się one przede wszystkim na automatach wideo. Wiele slotów online oferuje kolorową grafikę i ciekawe bonusy, ale Sugar Rush 1000 wyróżnia się dynamiczną mechaniką gry i możliwością zdobycia naprawdę wysokich mnożników wygranych. Oprócz tego, gra posiada intuicyjny interfejs, dzięki czemu jest idealna zarówno dla początkujących, jak i doświadczonych graczy. Nutritional values in 20g: energy value 120.8kcal 506.1kJ, fat 9.2g (including saturated fat 5.2g), carbohydrates 5.4g (including sugars 5.2g), fiber 2.0g, protein 1.8g, salt 0.0g

https://half-percent-listing.com/korzysci-z-posiadania-konta-vip-w-vulkan-vegas-dla-polskich-graczy/

– Choose 1 location on the table to drop money coin. – 24 7 online support for users Wybierając platformę z rozrywką hazardową, należy zwrócić uwagę na bezpieczeństwo, obecność licencji. Ponadto ważną rolę odgrywa asortyment. W 1win casinodostępnych jest wiele kategorii. Każda z nich oferuje mnóstwo rozrywki od znanych deweloperów. Wszystkie 1win casino games są uczciwe. Potwierdzają to testy niezależnych ekspertów. Dostępny jest hojny program bonusowy. W bonus casino 1winmożna wypłacić, spełniając warunki obrotu. Następnie środki są wykorzystywane do rozrywki bez ryzyka. Ekskluzywne bonusy są dostępne dla aktywnych użytkowników. Oto tabela popularnych gier. Kаsуnօ օnlinе i firmа bukmасhеrskа 1win dziаłа dlа grасzу z Pօlski օd 2018 rօku. Mаrkа jеst uwаżаnа zа wiаrуgօdnеgօ bukmасhеrа i uсzсiwеgօ օpеrаtօrа giеr hаzаrdօwусh օ pօzуtуwnеj rеputасji.

The Real Person!

The Real Person!

You are also free to play demo games for as long as you like. Many simply like to play slots purely for the fun element, and that’s fine. This guide, however, focuses on the real money side to slot play. There are literally thousands of casino games available online, so playing them all for real money would require quite the budget. But with free play, you can try a few rounds on many different games without spending any of your hard-earned money. If you want to play for real money but are not sure which games are worth your time and money, playing them for free first will allow you to figure it out risk-free. Technically, Bigger Bass Bonanza doesn’t do much the previous one didn’t. It just squeezes a few extra thrills out of the popular format. If you found yourself playing either the previous version or any number of Fishin’ Frenzy wannabes and just craved a little bit more, then Bigger Bass Bonanza could be the answer.

https://www.bonnettretail.com/your-complete-guide-to-aviator-game-download-apk-a-modern-casino-game-review/

Fishing Slots have climbed the ranks, topping the likes of Egyptian and Wild West slots. Nearly all software providers we cover have at least one fishing slot in their portfolio, but Reel Kingdom’s instalments are primarily fishing slots, more to the point, a magnitude of Big Bass titles. $0.0000 +0.00% During free spins, land wilds to collect all visible money symbols with values ranging up to 1,000x. Every fourth wild symbol retriggers the feature with 10 additional free spins and an increasing win multiplier – 2x on the first retrigger, 3x on the second, and 10x on the third and final retrigger. What is the max win in the slot of Big Bass Bonanza 1000? Landing three to five ‘scatters’ awards 10 to 20 free spins, while two scatters can activate a ‘hook’ feature, “randomly granting entry to the bonus game”.

The Real Person!

The Real Person!

Lastly, we evaluate the overall experience of each casino app. A sleek, modern app holds little value for players if it doesn’t deliver top games, exciting bonuses, and secure, fast payments. We also revisit the apps regularly to ensure they maintain high standards. If they fall short, we will update our reviews and ratings to reflect that. Buffalo King Megaways free play slot version is a North American frontier wild-themed title. This release grants players graphics plus chugging sounds, making it thrilling riveting. With 200704 possible paylines, this machine’s megaways feature underpins its 6-reel action. It has both veteran & novice players in mind, with its 96.52% RTP meaning considerable wins for players. This in-depth Buffalo King Megaways review will shed light on an enchanting video slot developed by Pragmatic Play. The Buffalo King Megaways slot transports players to the untamed wilderness of North America, where the spirit of the buffalo roams free. In this article, we will delve into every aspect of the game, including its features, the gaming mechanics, and its prospects for success. Come with us as we look for the hidden treasures that await in this majestic landscape.

https://benhviendakhoaanphat.com/how-to-withdraw-real-money-from-mines-game-in-pakistan-a-comprehensive-guide/

Playing Buffalo King Megaways is as fun as watching a herd of buffalo cross the plains. To get started set your bet. The game has a wide range of betting options so it’s suitable for casual players and high rollers. Set your bet and spin the reels and let the Megaways mechanics with their reel-modifier system do the rest. You could get up to 117,649 ways to win, one of the most in any Megaways slot. Every gambler aims to hit a big win and this slot can potentially award them. You will hit these wins when you play this slot patiently. The slot bonus rounds are more promising compared to the base game. Thus, you must play until you trigger these rounds. This slot comes with high volatility so it can be quite unfriendly to your bankroll. Therefore, you should set your bets tactfully to play several times and optimize your chances of activating the bonuses and hitting the massive wins.

The Real Person!

The Real Person!

Kosaciec Sugar Rush przyciąga spojrzenia swoim unikalnym wyglądem, a dodatkowo jest łatwy w pielęgnacji. Najważniejsze jednak, co należy zapamiętać z powyższych informacji to fakt, że w płytkach tonalnych nie należy doszukiwać się wzorów, który możliwy jest do ułożenia z jednego czy też nawet kilku opakowań. Tonalność to zabieg celowy nadany przez producenta. W jednym opakowaniu płytki tonalnej każda z płytek może różnić się od siebie. Przeczytaj na Naszym Blogu obszerny wpis o płytkach tonalnych Hity promocyjne Bezbarwny akrylowy proszek multifunkcyjny to prawdziwy must-have w Twojej kosmetyczce! Idealny do tworzenia lekkich, naturalnych stylizacji albo jako baza pod bardziej szalone projekty. Warto go mieć zawsze pod ręką – zamów i ciesz się perfekcyjnym manicure!

https://bionews.bioeconomycorporation.my/2025/08/05/przewodnik-po-grze-na-prawdziwe-pieniadze-w-vulkan-vegas/

Pobieranie i instalowanie Aviator Signals przebiega tak samo jak w przypadku Predictora. Zachowaj ostrożność i korzystaj wyłącznie z oprogramowania pochodzącego z zaufanych źródeł. Data areas are used in several different sectors. They can be a fantastic help in M&A deals, legal events, real-estate transactions, or perhaps general provider collaboration. They give a safe environment where you can retail store and share documents without worrying regarding privacy. Yet , with the amount of service providers on the market, it is usually hard to choose the best one for your organization. Here are some tips to help you make your decision: ODPOWIEDZIALNA GRA: aviator-cash-game zobowiązuje się do promowania odpowiedzialnej gry i współpracy z naszymi partnerami, którzy przestrzegają tej podstawowej wartości. Hazard online powinien być źródłem radości i rozrywki, a nie strachu lub zmartwień o straty finansowe. Jeśli kiedykolwiek poczujesz się przytłoczony podczas gry w gry kasynowe na naszej platformie, zrób sobie przerwę, aby odzyskać kontrolę i perspektywę.

The Real Person!

The Real Person!

Sugar Rush zelf ervaren? Speel het bij Fair Play Casino. Registreer je en begin met spelen. Behalve dat je je ongans misselijk eet aan de lekkerste snoep, biedt Sugar Rush nog veel meer: 20 winlijnen, 2 verschillende bonus features, stacked symbolen en een uitkeringspercentage van 95.25%%. If you think you need help, you can always contact our customer service using the contact form. They can advise you on our game offerings, your playing habits and setting your limits. All members of our customer service team have been trained and are aware of the risks of compulsive gambling. If you feel you might be at risk, they are readily available to assist you in finding the right solution to help restrict your gambling habits and pointing you in the right direction of organizations specialized in gambling addiction that can help you. In addition, there are numerous organizations that you can contact anonymously to tell your story and get help:

https://chat.westerwaldherzen.de/2025/08/05/sugar-rush-is-er-een-app-en-heb-je-die-nodig/

Zodra u vertrouwd met de basisconcepten en termen te worden, hoewel uiteindelijk ze verzekerd van een aantal concessies. De kans om rollen te vullen met kleurrijke snoepjes is gewoon te veel van een verleiding voor slot games ontwikkelaars, citroenen en watermeloenen. Veel van de meest gespeelde gokkasten bij Lets Jackpot zijn Pragmatic Play slots. Zo heb je bijvoorbeeld Sweet Bonanza, Gates of Olympus, Sugar Rush, Big Bass Splash en Book of Fallen. Daarnaast heb je Starburst van NetEnt, Bonanza van Big Time Gaming, Book of Dead van Play’n GO en Wanted Dead or a Wild van Hacksaw Gaming. Door onze website te bezoeken, verklaar je dat je 24+ bent en ga je akkoord met onze Algemene Voorwaarden, Privacybeleid. Je stemt ook in met ons gebruik van Cookies. Onze website bevat advertenties. Andere veel gespeelde slots zijn Pirots 3, Starburst, Gates of Olympus 1000, Sugar Rush, Super Flip en Temple Tumble Megaways.

The Real Person!

The Real Person!

support@pocketludo 4.8 star Truth or Dare Game Win prize money based on your performance in the game along with commissions. Truth or Dare Game Steps to Install .APK: To download MPL Ludo cash app on your mobile, visit the website and scan the QR code. Once the download link is available, follow the instructions to install the game. Search for “Ludo apk download,” and then follow the instructions to install the ludo earning app. Steps to Install .APK: Truth or Dare Game Visit the official website of LudoEmpire. This is usually the most reliable source for downloading the APK. Rush is a fun and free earning game app with AAA quality games, where the competitive spirit of India comes alive. Players compete against each other in skill-based free sports, casual, arcade, card and board games & win real money.

https://entreprise-electronique-lille.fr/aviator-top-bet-gaming-advanced-tips-for-high-rollers/

Click Here to View Event Details “Great set-up, great meetings with good investors, and great events.” Easily navigate your way around the event from the palm of your hand, with information about speakers, sessions, and maps with the locations of sponsors and exhibitors all at your fingertips. You will also be able to add presentations, networking events and meetings to your schedule, with reminders before they start, ensuring you never miss a beat. Your Privacy Choices Highland Copper Company Inc.Email: info@highlandcopperWebsite: highlandcopperPhone: (450) 677-2455 AGP Metals And Mining Showcase Contact us: Both conferences present industry professionals with the tools and knowledge to shape the future of mining, from technological advancements to sustainable practices. These events are must-attend for businesses looking to expand their expertise and influence in the mining industry.

The Real Person!

The Real Person!

Basic Game Info Play the original Big Buffalo slot from Skywind, where you have 4,096 ways to win, plus similar bonus features. The Blazin’ Buffalo slot by Rival Gaming offers free games and prize-picking rounds. Yes, the slot offers upto 15 free spins, upto 10 extra free spins along up upto 10x free spin multipliers. Many online casinos offer a free play or a slot demo Buffalo King Megaways option, so you can check out the features and gameplay without risking any of your own money. This way, you may get a feel for the game’s mechanics and experience the game’s thrilling gameplay. To feel the magic of the North American wilderness, all you have to do is launch the Buffalo King Megaways demo at your chosen online casino. This in-depth Buffalo King Megaways review will shed light on an enchanting video slot developed by Pragmatic Play. The Buffalo King Megaways slot transports players to the untamed wilderness of North America, where the spirit of the buffalo roams free. In this article, we will delve into every aspect of the game, including its features, the gaming mechanics, and its prospects for success. Come with us as we look for the hidden treasures that await in this majestic landscape.

http://users.atw.hu/nlw/profile.php?mode=viewprofile&u=24588

Social Club by Seneca is the way to get more for your play. Earn and redeem points and enjoy all the perks we offer for our loyal customers. You can win up to $50 in TS Rewards Points or Free Play! © . All Rights Reserved. CALL FOR INFORMATION ABOUT TICKET IN – TICKET OUT FREE PLAY FOR THIS MACHINE OR SEE RELATED ITEMS BELOW Wagering on horse racing and playing Video Gaming Machines is entertaining and fun when done in a responsible manner. If you or someone you know has a gambling problem, please call for 24-hour assistance at 1-877-8 HOPE NY* or click HERE to visit the NY Council on Problem Gambling Support Directory. Click HERE for more information on our Voluntary Self-Exclusion Program. *Standard rates may apply © document.write(new Date().getFullYear()); Pokagon Band of Potawatomi Indians. Must be 21 years of age. Please play responsibly. Four Winds Casinos are Equal Opportunity Employers.

The Real Person!

The Real Person!

Are you ready to transform your online sales game? The most successful online sellers have mastered a set of habits that consistently drive their success. Curious to know their secrets? Read on to uncover the top 10 habits that can boost your sales and take your business to new heights! Are you ready to transform your online sales game? The most successful online sellers have mastered a set of habits that consistently drive their success. Curious to know their secrets? Read on to uncover the top 10 habits that can boost your sales and take your business to new heights! Receive a bonus $200with trade-in.43 Packed with new ways for you to play, whether you want to roleplay the God of Thunder by using Elemental Cleaver, imbuing your Path of the Giant Barbarian’s hammer with shocking damage and flinging it out for it to come back to you, or as a drunken monk, with truly homebrewed abilities that will enhance your next playthrough, there’s surely a subclass for you!

https://jenerickresort.com.ph/arabic-language-support-in-teen-patti-gold-live-dealer-mode-a-closer-look/

Special pricing just for you Step 3: Your Mega Spin will be waiting for you in your ‘My Rewards’ section Please enter your 16-digit ID number in this section and make sure it is correct. Vertigo Games is not responsible for purchases made with the wrong identification. Step 2: Play €10 on ANY slot game you choose. If this is your first time topping up your account, don’t forget to specify the bonus code. It will increase the size of the payment by 500%. The funds will immediately arrive on the balance of the game account. For the system to provide them, you need to copy the code and specify it. Sugar Rush takes a different approach to gameplay mechanics when compared to other candy-themed slots like Sweet Bonanza. Discover the unique gameplay aspects that set this game apart in our review.

The Real Person!

The Real Person!

There were also sketchy websites set up as landing pages. The people behind it even added made-up player comments claiming the Mr Beast casino app is real and they won real money. Below, we show the fake MrBeast app site designed to look like the Google Play Store. No, the Mr Beast Casino is not real. It is not linked to the YouTuber, and it does not hold a gambling licence issued by the UKGC. Some people might assume it’s safe because of the brand association, but this is misleading. The Instagram ads served to users featured videos with deepfake technology for the visuals and artificial-intelligence generated audio for the vocals. All of the videos followed the same format. The videos began with one recognizable cable news host appearing to speak about a MrBeast-created casino game. Interview clips with a famous celebrity and MrBeast followed the cable news host. The videos ended with the same cable news host encouraging users to click a download link.

https://harmony1.vn/blog/2025/08/19/review-of-football-xs-mine-island-slot-unlocking-cashback-bonuses-for-indian-players/

While Stake.us doesn’t offer the specific chicken-crossing game, this site does offer plenty of alternatives for you to dive into. This includes the popular crash-style game Stake Crash and loads of chicken-themed slots like Chicken Rush, Chicken Man and many more. So, why not take advantage of the Stake.us welcome bonus to grab yourself lots of free coins which will be plenty for exploring all of these fantastic games. Click the banners on our page to sign up today and use the code DIMERS! Mission Uncrossable is a Roobet Original game that offers unique, but simple gameplay. The goal of this game is to get your chicken across the road, without being hit by any of the oncoming cars. To get your Chicken from one side to the other there will be a number of lanes you need to cross, with each one providing an increased multiplier on your original bet. Cash out at any time at Rootbet Mission Uncrossable, or keep going, to see how far you can get the chicken, and push the multiplier up while you do so.

The Real Person!

The Real Person!

You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page. Ariel Boles Sugar Rush tragaperras se juega en una rejilla de 7×7 con un sistema de pagos de “cluster pays”, lo que significa que las combinaciones ganadoras se hacen al agrupar al menos 5 símbolos iguales de manera adyacente, ya sea en horizontal o vertical, sin necesidad de una línea de pago tradicional. Las instrucciones para jugar a tragamonedas Sugar Rush son: Registrate según el domicilio en tu DNI Fiesta Nacional de la Vendimia 2023 Sugar Rush es más que un juego; es un fenómeno cultural que ha sabido capturar la esencia de la diversión y el aprendizaje en un paquete vibrante y atractivo. Su impacto trasciende las fronteras del entretenimiento, tocando aspectos educativos, económicos y sociales. A medida que continúa evolucionando, Sugar Rush promete seguir siendo un tema de interés en las noticias y un favorito entre los jugadores de todas las edades. Este juego demuestra el poder de la innovación y la creatividad en la era digital, y su legado seguramente inspirará a futuras generaciones en el mundo de los videojuegos y más allá.

https://www.byc.cl/big-bass-bonanza-analisis-detallado-del-juego-de-casino-de-pragmatic-play/

Sugar Rush 1000 de Pragmatic Play cuenta con 2 tipos de tiradas de bonificación: normal y súper. En la versión mejorada de la ronda de bonificación, a todas las casillas se les asigna inmediatamente un multiplicador 2x. Cuando vayas a jugar al póquer, reglamento de ruleta casino en mayo de 2023. Esta es una de las mejores maneras de probar si un sitio de casino es genuino o no, la propuesta de privatizar Holland Casino fue derogada debido a la falta de apoyo en el Senado holandés. Sugar Rush 1000 perfecciona las características de su predecesor, prometiendo una experiencia de juego más envolvente. He aquí los cambios. Oferta de entretenimiento en casinos en línea. Las redes sociales lo ponen en contacto con las personas que son, tiene un botón que revela el menú de su cuenta. Los jugadores toman la acción en la tragamonedas en línea Santa’s Big Bash Megaways en un conjunto de carretes de 6×7, generalmente debe depositar la cantidad mínima requerida para activar la oferta durante un período de tiempo específico.

The Real Person!

The Real Person!

Anpassen Cookie-Details Ja, du kannst einen 300% Bonus ablehnen. In den meisten Online Casinos hast du beim Einzahlen die Wahl, ob du den angebotenen Bonus annimmst oder nicht. Wenn du den Bonus ablehnst, spielst du nur mit deinem eingezahlten Geld und bist nicht an die Bonusbedingungen wie Mindestumsatz oder Zeitlimits gebunden. Verbinden Sie sich mit uns Die absoluten Überhits dieses Gaming Studios haben wir Ihnen bereits vorgestellt: Sweet Bonanza, Gates of Olympus, Big Bass Bonanza und Sugar Rush sind die unbestrittenen Platzhirsche der Slot Game Industrie auch in Deutschland. In absoluter Schlagdistanz was Qualität, Spielspaß und Gaming Experience anbelangt, sind diese Games: The Dog House Megaways, John Hunter Slots, Wild West Gold. In terms of setting, the game takes place in a whimsical candy land populated by sweeties of all descriptions, from jelly beans to gumdrops and beyond. The colourful visuals and vibrant soundtrack complement this theme nicely. The highlights of Sugar Rush 1000 are the bonus features. These include free spins, which can be scored by hitting scatters, and multiplier spots, which accumulate on specific positions on the grid and amplify your wins.

https://airpatrolnorth.ca/sugar-rush-autoplay-spiele-effizient-nutzen-ein-praktischer-leitfaden/

Zahle heute ein und du bekommst 70 Freespins für „Chicken Chase“. Um das beste Online-Casino in Deutschland mit Sweet Bonanza zu finden, haben wir mehrere verschiedene Plattformen getestet, auf denen das Spiel verfügbar ist. Die folgende Tabelle zeigt 5 zuverlässige Optionen für Sweet Bonanza-Casinos, mit guten Promotionen und anderen wichtigen Eigenschaften. Sollte das Problem weiterhin bestehen, kontaktieren Sie uns bitte, indem Sie auf „Problem beschreiben“ klicken. Lucky Streak 1000 Gates of Olympus 1000 Mobile free spins bonus codes are special promotions that can be used to claim free spins on mobile devices or through a casino’s mobile app. These codes enable players to enjoy free spins on their smartphones or tablets, offering the convenience of playing on the go. On the other hand, mobile-specific bonus codes create an illusion of exclusivity while primarily serving as tracking mechanisms for marketing effectiveness.

The Real Person!

The Real Person!