Operational Highlights

Operational Highlights

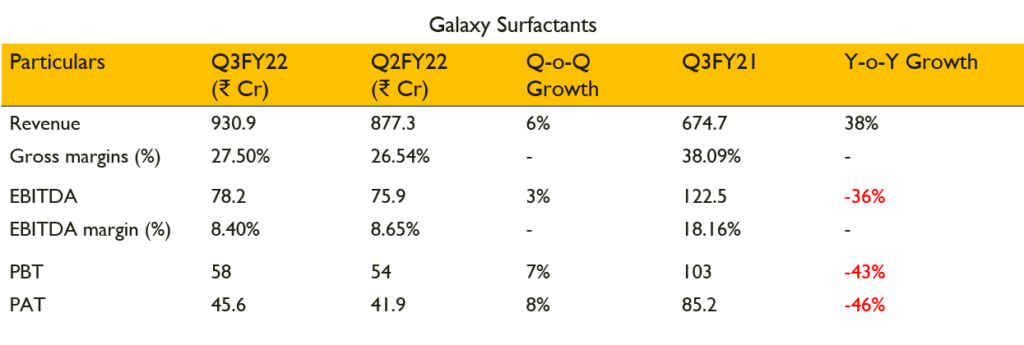

- The revenues for Q3FY22 stood at ₹929.1Cr from ₹674.7 Cr in same period previous year accounting to growth of 37.7% YoY

- EBITDA for the quarter stood at ₹78.2Cr translating to EBITDA margins of 8.4%

- PAT contracted by (-46.5%) YoY to ₹45.6 Cr in Q3FY22 from ₹85.2Cr in Q3FY21 translating to PAT margins of 4.9% for the current quarter

- Supply led volatility continued in Q3FY22

- While the volumes remain flat YoY, the decline in EBITDA impacted the overall performance

- Across the board inflationary scenario combined with Supply Chain challenges (Freight Costs + On time Container availability + Port congestion) impacted International Volumes and Margins

- EBITDA/MT below the stated band of Rs 16,000-18,000/MT on account of higher input costs and higher cost of servicing given the volatile scenario

Volume breakup for Q3FY22

- Performance Surfactants 36,983MT

- Specialty care-21,044 MT

- Total production volume is at 58,027 MT

- Indian market grew by 6.9% on YoY basis

- Africa, the Middle east and Turkey contracted by 9.2% on YoY basis. RoW regions grew by 2.5%

- Volumes were affected in turkey due to local problems, besides that all other geographies stood robust in terms of demand

- Logistical issues in North America is more on the the internal truck network, the containers are timely on ports but delivery is delayed due to lack of availability of trucks

Revenue Split in Q3FY22

- Performance Surfactants -61% i.e ₹570 Crs

- Specialty care-39% i.e ₹361Crs

- Fatty Alcohol prices in this Quarter increased to an average price of $ 2,602/MT vs, average prices of $ 1,558/MT in Q3FY21.

- Crude derivatives, fatty alcohols, and fatty acids constitute nearly 80% of raw material procurement and sudden surge in fatty alcohols, crude and freight rates impacted the margins. Compared to September, the have increased in Oct-Dec quarter by 10-45%. These incremental costs will be passed on with lag of one quarter

- Significant share of the speciality business is on contractual basis with a quarterly lag to pass the incremental rice increase.

- Export incentives realised in egypt during Q3 to the tune of ₹14 Crs was not recognized in the current quarter.

- Raw material availability improved in this quarter, but container shortage resulted in delayed shipments accounting to loss of volumes

- Plant commissioning in line at Jhagadia, the capacities has been well utilised and will ramp up fast whereas at Tarapur facility, which is under process of commissioning will ramp up slower compared to Jhagadia

- Expecting to spend ₹150-₹200 Cr for capex every year

- The new product diversification basket will be more speciality based

- Certain orders will be deferred and have a quarter lag due to delay in availability of raw materials

- Target to have volume growth of 6-8%

- Fatty alcohols prices were $2600/MT in Q3 and has elevated to $3000/MT

- Capacity utilisation for 9M stood at 67% and for previous year it was 65%

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

The Real Person!

The Real Person!

kamagra 100mg prix: Achetez vos kamagra medicaments – kamagra 100mg prix

The Real Person!

The Real Person!

pharmacie en ligne fiable: pharmacie en ligne france livraison belgique – pharmacie en ligne pas cher pharmafst.com

The Real Person!

The Real Person!

acheter kamagra site fiable: kamagra gel – Kamagra Oral Jelly pas cher

The Real Person!

The Real Person!

achat kamagra: acheter kamagra site fiable – kamagra oral jelly

The Real Person!

The Real Person!

pharmacie en ligne pas cher: pharmacie en ligne – pharmacie en ligne france fiable pharmafst.com

The Real Person!

The Real Person!

Acheter Cialis: Cialis sans ordonnance 24h – Cialis en ligne tadalmed.shop

The Real Person!

The Real Person!

cialis sans ordonnance: Pharmacie en ligne Cialis sans ordonnance – Cialis sans ordonnance 24h tadalmed.shop

The Real Person!

The Real Person!

Tadalafil sans ordonnance en ligne: Tadalafil 20 mg prix en pharmacie – Tadalafil 20 mg prix en pharmacie tadalmed.shop

The Real Person!

The Real Person!

acheter kamagra site fiable: kamagra pas cher – kamagra oral jelly

The Real Person!

The Real Person!

Kamagra Oral Jelly pas cher: Acheter Kamagra site fiable – Achetez vos kamagra medicaments

The Real Person!

The Real Person!

kamagra livraison 24h: acheter kamagra site fiable – kamagra livraison 24h

The Real Person!

The Real Person!

Tadalafil 20 mg prix en pharmacie: Cialis sans ordonnance 24h – Tadalafil 20 mg prix sans ordonnance tadalmed.shop

The Real Person!

The Real Person!

pharmacie en ligne france livraison belgique: pharmacie en ligne pas cher – pharmacie en ligne avec ordonnance pharmafst.com

The Real Person!

The Real Person!

Achat mГ©dicament en ligne fiable: Pharmacie en ligne France – pharmacie en ligne sans ordonnance pharmafst.com

The Real Person!

The Real Person!

Tadalafil 20 mg prix en pharmacie: Tadalafil achat en ligne – Cialis sans ordonnance pas cher tadalmed.shop

The Real Person!

The Real Person!

Pharmacie en ligne Cialis sans ordonnance: Cialis generique prix – Acheter Cialis 20 mg pas cher tadalmed.shop

The Real Person!

The Real Person!

pharmacie en ligne france fiable: pharmacie en ligne pas cher – vente de mГ©dicament en ligne pharmafst.com

The Real Person!

The Real Person!

Achat mГ©dicament en ligne fiable: Meilleure pharmacie en ligne – pharmacie en ligne france livraison belgique pharmafst.com

The Real Person!

The Real Person!

kamagra en ligne: Kamagra Commander maintenant – Acheter Kamagra site fiable

The Real Person!

The Real Person!

Achat mГ©dicament en ligne fiable: Livraison rapide – Pharmacie Internationale en ligne pharmafst.com

The Real Person!

The Real Person!

online pharmacy canada: Express Rx Canada – legitimate canadian online pharmacies

The Real Person!

The Real Person!

mexican rx online: mexican rx online – mexico pharmacies prescription drugs

The Real Person!

The Real Person!

RxExpressMexico: mexico drug stores pharmacies – mexico drug stores pharmacies

The Real Person!

The Real Person!

indian pharmacy online: Medicine From India – indian pharmacy online

canadian pharmacy 365 Buy medicine from Canada canadianpharmacy com

canadian drugstore online: Generic drugs from Canada – canada drugs online reviews

The Real Person!

The Real Person!

Online medicine home delivery: indian pharmacy online shopping – indian pharmacy online shopping

ed drugs online from canada Canadian pharmacy shipping to USA canadian pharmacy no rx needed

canadianpharmacy com: Generic drugs from Canada – canadian pharmacy online store

The Real Person!

The Real Person!

mexican rx online: mexico pharmacy order online – medication from mexico pharmacy

legal to buy prescription drugs from canada Express Rx Canada canadian medications

The Real Person!

The Real Person!

top 10 pharmacies in india: indian pharmacy online – indian pharmacies safe

online pharmacy india: india online pharmacy – indian pharmacy

indian pharmacy online shopping Medicine From India Medicine From India

Rx Express Mexico: mexico pharmacy order online – mexican online pharmacy

The Real Person!

The Real Person!

mexico pharmacy order online: mexico drug stores pharmacies – mexico pharmacy order online

The Real Person!

The Real Person!

vavada вход: вавада зеркало – vavada casino

The Real Person!

The Real Person!

пин ап казино официальный сайт: пин ап вход – пин ап казино

The Real Person!

The Real Person!

pin-up casino giris: pin up casino – pin up az

The Real Person!

The Real Person!

vavada: vavada вход – vavada casino

The Real Person!

The Real Person!

pin up вход: pin up вход – пин ап вход

The Real Person!

The Real Person!

вавада зеркало: вавада казино – вавада

The Real Person!

The Real Person!

vavada: вавада казино – vavada вход

The Real Person!

The Real Person!

пин ап вход: pin up вход – пин ап вход

The Real Person!

The Real Person!

вавада казино: vavada – вавада казино

The Real Person!

The Real Person!

пинап казино: пин ап вход – pin up вход

вавада официальный сайт: вавада зеркало – vavada

пин ап казино официальный сайт: пин ап казино – пинап казино

пинап казино: pin up вход – пин ап зеркало

vavada вход: вавада зеркало – vavada

vavada вход: vavada – vavada

vavada casino: вавада – vavada вход

пин ап вход: пин ап казино – pin up вход

пинап казино: пин ап казино официальный сайт – пин ап зеркало

вавада официальный сайт: vavada – вавада казино

пин ап вход: пин ап вход – пин ап вход

пин ап казино официальный сайт: пин ап вход – пин ап казино официальный сайт

пин ап зеркало: пин ап вход – пин ап вход

Today, I went to the beach with my kids. I found a sea shell and gave it to my 4 year old daughter and

said “You can hear the ocean if you put this to your ear.” She placed the shell to her

ear and screamed. There was a hermit crab inside

and it pinched her ear. She never wants to go back! LoL I know this is entirely off topic but I had to tell someone!

Feel free to surf to my site: nordvpn coupons inspiresensation; http://cfg.me,

пинап казино: pin up вход – пин ап казино

The Real Person!

The Real Person!

safe online pharmacy: buy generic Viagra online – fast Viagra delivery

The Real Person!

The Real Person!

Cialis without prescription: cheap Cialis online – FDA approved generic Cialis

350fairfax nordvpn coupons

It’s really a cool and useful piece of information. I’m happy that you simply shared this

useful info with us. Please keep us informed like this.

Thanks for sharing.

The Real Person!

The Real Person!

buy generic Cialis online: order Cialis online no prescription – order Cialis online no prescription

The Real Person!

The Real Person!

order Cialis online no prescription: discreet shipping ED pills – online Cialis pharmacy

The Real Person!

The Real Person!

no doctor visit required: cheap Viagra online – same-day Viagra shipping

The Real Person!

The Real Person!

generic sildenafil 100mg: safe online pharmacy – secure checkout Viagra

The Real Person!

The Real Person!

doctor-reviewed advice: modafinil 2025 – modafinil pharmacy

The Real Person!

The Real Person!

affordable ED medication: affordable ED medication – best price Cialis tablets

The Real Person!

The Real Person!

same-day Viagra shipping: buy generic Viagra online – safe online pharmacy

https://maxviagramd.com/# no doctor visit required

The Real Person!

The Real Person!

best price Cialis tablets: order Cialis online no prescription – order Cialis online no prescription

verified Modafinil vendors: verified Modafinil vendors – modafinil 2025

https://modafinilmd.store/# purchase Modafinil without prescription

The Real Person!

The Real Person!

best price for Viagra: discreet shipping – order Viagra discreetly

safe modafinil purchase: legal Modafinil purchase – safe modafinil purchase

The Real Person!

The Real Person!

doctor-reviewed advice: safe modafinil purchase – modafinil legality

The Real Person!

The Real Person!

order cheap clomid: Clom Health – where to buy generic clomid without dr prescription

The Real Person!

The Real Person!

Amo Health Care: how to buy amoxicillin online – Amo Health Care

The Real Person!

The Real Person!

can i purchase clomid price: buying cheap clomid without insurance – can i get generic clomid without rx

The Real Person!

The Real Person!

PredniHealth: buy prednisone from india – price of prednisone tablets

The Real Person!

The Real Person!

can i buy cheap clomid: clomid without dr prescription – order cheap clomid pills

Ero Pharm Fast: where can i get ed pills – ed meds online

get antibiotics without seeing a doctor BiotPharm antibiotic without presription

http://eropharmfast.com/# Ero Pharm Fast

over the counter antibiotics: buy antibiotics online uk – buy antibiotics online

buy ed medication online boner pills online Ero Pharm Fast

http://eropharmfast.com/# online ed pills

Ero Pharm Fast: buy ed meds – Ero Pharm Fast

Ero Pharm Fast Ero Pharm Fast Ero Pharm Fast

https://biotpharm.shop/# get antibiotics quickly

antibiotic without presription Biot Pharm cheapest antibiotics

Online drugstore Australia Pharm Au24 PharmAu24

Buy medicine online Australia: Discount pharmacy Australia – Pharm Au 24

Howdy would you mind letting me know which web host

you’re working with? I’ve loaded your blog in 3 different internet browsers and I must say this blog loads a lot quicker then most.

Can you recommend a good web hosting provider at a honest price?

Cheers, I appreciate it!

Look at my blog; eharmony special coupon code 2025

This is a topic that’s near to my heart… Many thanks!

Exactly where are your contact details though?

Take a look at my homepage; vpn

Pretty section of content. I just stumbled upon your weblog and in accession capital to assert that I get actually enjoyed account your blog posts.

Anyway I’ll be subscribing to your augment and even I achievement you access consistently fast.

https://tinyurl.com/235hnz7u gamefly free trial

Awesome! Its genuinely amazing article, I have got much clear idea about from

this paragraph. What does vpn mean https://tinyurl.com/2c2rno87

Hello there! I could have sworn I’ve been to your blog before but after

looking at many of the posts I realized it’s new to me.

Regardless, I’m certainly delighted I came across it and I’ll be book-marking it and checking back regularly!

You’ve made some good points there. I checked on the

web to find out more about the issue and found most people

will go along with your views on this website.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

I simply couldn’t leave your webvsite before suggesting that I really loved the

standard info an individual prpvide on your guests?

Is going to be back frequently in order to check out new posts https://fortune-glassi.mystrikingly.com/

Great weblog here! Additionally your web site loads

up very fast! What host are you the usage of? Can I am getting your associate hyperlink in your host?

I desire my website loaded up as quickly as yours lol eharmony

special coupon code 2025 https://tinyurl.com/yneylc4d

Outstanding post however , I was wanting to

know if you could write a litte more on this topic? I’d be very thankful if you could elaborate a little bit more.

Bless you!

Here is my web-site: http://winkler-martin.de/messages/61849.html

Thanks for finally writing about > Galaxy Surfactants Q3 2022 Concall

Highlights – Value Educator tinyurl.com)