Operational Highlights

Operational Highlights

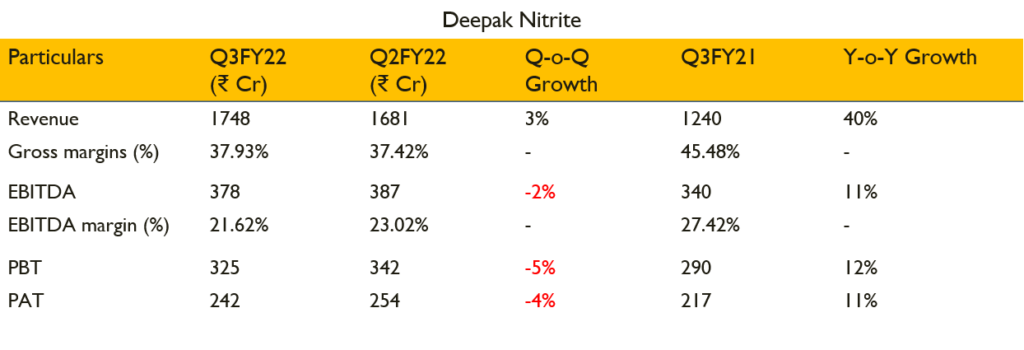

- The revenue for the quarter was ₹1748 cr it was up 41% YoY as against ₹1240 Cr in same quarter previous year

- EBITDA margins stood at 22% translation to EBITDA of ₹378 Cr

- Continued robust revenue momentum was fueled by solid growth trajectory in Phenolics

- In Q3 FY22, the company has achieved highest ever top line in a quarter, both on standalone and consolidated basis

- Business segments are interwoven, this means that if prices of BI increases, you may see a simultaneous dip in FSCsegment, as internal product transfers take place at market prices.

- This year has been very strong for BI segment. In FSC segment, as most are long term contracts, there is some lag inpassing the input costs

- In 9MFY22 volumes grew by 10% partially because of brownfield expansion

- Evaluating opportunities to develop expertise in levels of fluorination and photochlorination.

- China is the largest manufacturer of certain commodities but most of it is captively consumed, so it doesn’t really impact much to the domestic capacities

- Phenol and acetone will remain strong in further quarters

- Last year was covid period, thus it is essential to understand that YoY volume growth is with the base of covid year and thus seems to be higher

- phenol ‘s captive consumption is around 20-25% and expected to rise upto 40-45%, post expansion

- Commodity companies did well during the Q3 but it won’t be the same going forward as the KSM prices neutralises, margins will be back in place

- Having dominant wallet share and market position in operating geographies with most of the products having 75-80% market share

- Rise in crude price have impacted the propylene prices

- Cost of the diesel used for transporting materials to customers (trucks & tankers) is ₹15Crs on monthly basis

- Revoke of anti dumping duty does not affect the business

Segment performance

Basic Intermediates segment

- Basic Intermediates revenue was ₹345.81 cr up by 76.2% YoY

- Benefited from healthy realisation gains as price hikes were undertaken for key products,in-line with higher input costs.

- Volume growth for 9M FY22 came in at 10%

Fine & Specialty

- Fine & Speciality Chemicals revenue stood at ₹206.66 cr down by 2% YoY

- The performance of the FSC segment must be seen in light of significant challenges linked to logistics.

- In addition to this, the Company witnessed elevated raw material costs from BC segment

Performance Products

- Performance product segment stands to benefit from demand supply asymmetries

- Performance Products Revenue was ₹169.88 cr up by 88% YoY

- Momentum in DASDA demand is seen, resulting in higher realisation and OBA was also able to pass on this increase in DASDA costs

- volume growth for 9M FY 22 remained strong, at 44%

Phenolics

- Phenolics revenue stood at ₹1,033.11 cr up by 38.3% YoY

- Capacity utilisation was 117%

- Company plans to bring in downstream products of phenol in FY 22-23

Capex

- Brownfield expansion of IPA was commissioned on 19th December 2021. This has doubled the IPA capacity to 60,000 MTPA

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.com/cs/register?ref=S5H7X3LP

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

The Real Person!

The Real Person!

http://pinupaz.top/# pin up az

The Real Person!

The Real Person!

best price for Viagra: buy generic Viagra online – fast Viagra delivery

The Real Person!

The Real Person!

buy modafinil online: Modafinil for sale – modafinil legality

The Real Person!

The Real Person!

order Cialis online no prescription: buy generic Cialis online – generic tadalafil

The Real Person!

The Real Person!

buy modafinil online: verified Modafinil vendors – legal Modafinil purchase

The Real Person!

The Real Person!

trusted Viagra suppliers: Viagra without prescription – safe online pharmacy

The Real Person!

The Real Person!

verified Modafinil vendors: Modafinil for sale – safe modafinil purchase

The Real Person!

The Real Person!

verified Modafinil vendors: verified Modafinil vendors – modafinil legality

The Real Person!

The Real Person!

Viagra without prescription: trusted Viagra suppliers – fast Viagra delivery

The Real Person!

The Real Person!

FDA approved generic Cialis: order Cialis online no prescription – discreet shipping ED pills

https://maxviagramd.com/# legit Viagra online

The Real Person!

The Real Person!

cheap Cialis online: best price Cialis tablets – online Cialis pharmacy

http://zipgenericmd.com/# best price Cialis tablets

The Real Person!

The Real Person!

order Cialis online no prescription: cheap Cialis online – buy generic Cialis online

The Real Person!

The Real Person!

affordable ED medication: order Cialis online no prescription – online Cialis pharmacy

http://zipgenericmd.com/# online Cialis pharmacy

The Real Person!

The Real Person!

no doctor visit required: buy generic Viagra online – same-day Viagra shipping

The Real Person!

The Real Person!

prednisone canada prices: prednisone nz – prednisone 10 mg over the counter

The Real Person!

The Real Person!

how to get clomid for sale: where can i buy cheap clomid without a prescription – can i buy clomid for sale

The Real Person!

The Real Person!

can you get cheap clomid without rx: Clom Health – how to get clomid without insurance

The Real Person!

The Real Person!

order prednisone 100g online without prescription: PredniHealth – PredniHealth

The Real Person!

The Real Person!

prednisone 5 50mg tablet price: PredniHealth – PredniHealth

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.com/ru/register?ref=V3MG69RO

cheapest ed pills online ed medication Ero Pharm Fast

buy antibiotics from canada: Biot Pharm – buy antibiotics from india

https://biotpharm.com/# cheapest antibiotics

Over the counter antibiotics for infection buy antibiotics online uk over the counter antibiotics

best online ed treatment: Ero Pharm Fast – Ero Pharm Fast

https://biotpharm.shop/# buy antibiotics from india

Over the counter antibiotics for infection: BiotPharm – get antibiotics without seeing a doctor

erectile dysfunction pills online Ero Pharm Fast erectile dysfunction online prescription

http://eropharmfast.com/# Ero Pharm Fast

Ero Pharm Fast п»їed pills online Ero Pharm Fast

https://eropharmfast.com/# ed meds online

where to get ed pills Ero Pharm Fast Ero Pharm Fast

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.