Operational Highlights

Operational Highlights

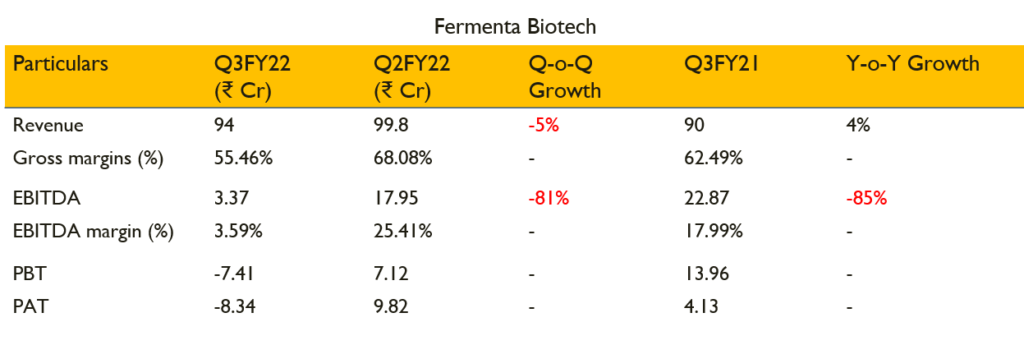

- The revenues for the quarter stood at ₹93Cr with growth of 3.2% YoY

- EBITDA stood at ₹2.2Cr translating to EBITDA margins of 2.36%

- The company posted a loss of (-₹8 Cr) and negative PAT margins

- Q3-FY22 gross margins are better by 3.6% over Q2-FY22. However due to lower sales and under absorption of cost the EBITDA margins have dropped approximately by 3%.

- Volumes of Human Vitamin D3 in Q3-FY22 are lower by 31% over Q2-FY22 due to lower offtake of Human Vitamin D3, however they are higher by 19% in 9M-FY22 over 9M-FY21.

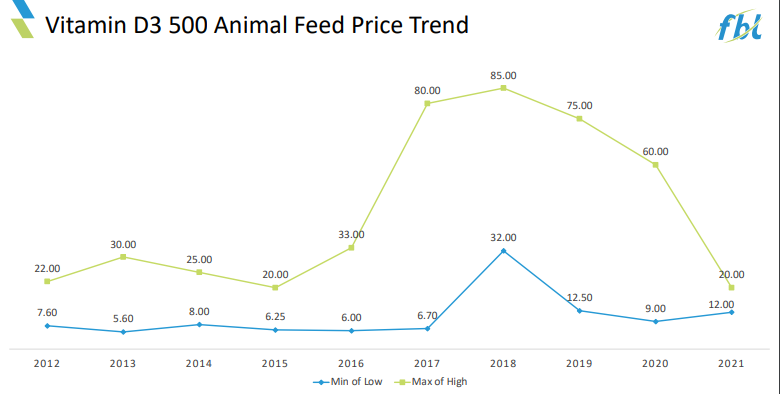

- Volumes of Animal Feed in Q3-FY22 are higher by 145% over Q2-FY22, however they are lower by 33% in 9M-FY22 over 9M-FY21. The prices are also lower by 22% in 9MFY22 over 9MFY21

- Fish Oil Cholesterol revenue was down by 55% in Q3-FY22, however it was higher by 80% for the 9 month period

- The benefit of Sec 10 (AA) under the Income Tax Act for SEZ unit ceases to exist w.e.f. FY 22

- The human nutrition suffered in this quarter but as far overall demand is concerned, it stays strong

- NSE listing is expected to be conducted post merger

- In nutrition business- Human nutrition- 64.3% and Animal feed was 35.7%

- Formulation of products are into oil, powder and spray dry forma,.powder portfolio is majorly exported.

- Currently the major part of business is vitamin D3 and 80% of volumes are used in animal feed. Animal feed is a commodity business and china is also responsible for volatility in prices, however this is tackled by product diversification, working on cost improvement and process from new raw materials to improve efficiency etc.

- Aspiration to reach ₹1000Cr revenues in 5-6 years

- The previous year high revenues were primarily driven by high vitamin prices

- The company is developing proprietary technology to manufacture vitamin D3 from fish oils and cholesterols, targeting the same product quality with different use of raw material which will benefit in manufacturing cost. The company is evaluating pathways to get the necessary regulatory approvals for the usage of new raw materials.

Monetization of Thane land

- As part of its legacy property, Fermenta owns ~6.5 acres of freehold land in Thane. This is partly developed by constructing Thane One, an IT/ITES Building

- Fermenta has signed Binding Term Sheet with Mextech and granted development rights for construction of residential-cum-commercial buildings in the balance portion of land

- Development partners are solely responsible for obtaining approvals, permissions, construction, OC and sales and will solely bear all the costs of approvals, permissions, premiums and construction in the Project

- Fermenta to receive 120,000 sq. ft. carpet area (as per RERA) of residential construction along with amenities as its share of premises in the Project, and the balance area to be owned by development partners.

Subsidiary updates

- Germany: It has obtained the required approvals in Q3-FY22 and has clocked sales of ₹6.1 Cr. However, being the first sales most of the initial trial cost, campaign cost and inventory carrying cost for the last two and half years was loaded on the initial products manufactured. This has resulted in higher manufacturing cost and revaluation of the inventory resulting in loss of ₹8.6 Cr in Q3-FY22. The German subsidiary is mainly for animal feed and is expected to generate higher profits compared to indian standalone business

- USA: USA Subsidiary incurred loss of ₹0.8 Cr for the quarter and ₹1.4 Cr for the 9 months mainly on account of lower offtake of Animal Vitamin D3 volumes due to ongoing ‘Covid-19’ pandemic.

Kamagra Commander maintenant: kamagra oral jelly – kamagra en ligne

cialis generique: Acheter Cialis 20 mg pas cher – Acheter Cialis 20 mg pas cher tadalmed.shop

The Real Person!

The Real Person!

acheter kamagra site fiable: Kamagra Commander maintenant – Kamagra pharmacie en ligne

The Real Person!

The Real Person!

Acheter Cialis: Tadalafil 20 mg prix en pharmacie – Cialis sans ordonnance 24h tadalmed.shop

The Real Person!

The Real Person!

Achat mГ©dicament en ligne fiable: pharmacie en ligne pas cher – Achat mГ©dicament en ligne fiable pharmafst.com

pharmacie en ligne livraison europe: pharmacie en ligne pas cher – Pharmacie Internationale en ligne pharmafst.com

The Real Person!

The Real Person!

kamagra oral jelly: achat kamagra – kamagra oral jelly

The Real Person!

The Real Person!

Pharmacie sans ordonnance: Medicaments en ligne livres en 24h – п»їpharmacie en ligne france pharmafst.com

The Real Person!

The Real Person!

pharmacie en ligne: pharmacie en ligne pas cher – pharmacie en ligne fiable pharmafst.com

The Real Person!

The Real Person!

Acheter Cialis: Tadalafil sans ordonnance en ligne – Acheter Cialis 20 mg pas cher tadalmed.shop

The Real Person!

The Real Person!

pharmacie en ligne fiable: Pharmacies en ligne certifiees – pharmacie en ligne pas cher pharmafst.com

The Real Person!

The Real Person!

Tadalafil 20 mg prix sans ordonnance: Tadalafil 20 mg prix sans ordonnance – Tadalafil sans ordonnance en ligne tadalmed.shop

The Real Person!

The Real Person!

indian pharmacy online shopping: indian pharmacy online shopping – Medicine From India

The Real Person!

The Real Person!

top 10 pharmacies in india: cheapest online pharmacy india – п»їlegitimate online pharmacies india

The Real Person!

The Real Person!

RxExpressMexico: mexican rx online – Rx Express Mexico

The Real Person!

The Real Person!

indian pharmacy online: indian pharmacy – medicine courier from India to USA

canadian pharmacy checker Buy medicine from Canada canadian neighbor pharmacy

The Real Person!

The Real Person!

the canadian drugstore: Generic drugs from Canada – canadian pharmacy online ship to usa

canadian pharmacy king reviews: Buy medicine from Canada – canadianpharmacyworld com

Rx Express Mexico mexico pharmacy order online mexico pharmacy order online

The Real Person!

The Real Person!

MedicineFromIndia: medicine courier from India to USA – Medicine From India

Rx Express Mexico: purple pharmacy mexico price list – mexico pharmacies prescription drugs

The Real Person!

The Real Person!

mexico drug stores pharmacies: RxExpressMexico – Rx Express Mexico

indian pharmacy online indian pharmacy online medicine courier from India to USA

MedicineFromIndia: medicine courier from India to USA – indian pharmacy

The Real Person!

The Real Person!

the canadian pharmacy: ExpressRxCanada – canadian pharmacies that deliver to the us

Rx Express Mexico mexico drug stores pharmacies mexican online pharmacy

The Real Person!

The Real Person!

вавада казино: вавада казино – вавада

The Real Person!

The Real Person!

вавада казино: вавада зеркало – вавада казино

The Real Person!

The Real Person!

pin up вход: пин ап вход – pin up вход

The Real Person!

The Real Person!

pin up azerbaycan: pin-up casino giris – pin-up casino giris

The Real Person!

The Real Person!

вавада: vavada вход – vavada вход

The Real Person!

The Real Person!

пин ап казино официальный сайт: pin up вход – pin up вход

The Real Person!

The Real Person!

пинап казино: пинап казино – pin up вход

The Real Person!

The Real Person!

pin-up: pin up azerbaycan – pin up

вавада: вавада казино – vavada casino

вавада: vavada – вавада зеркало

pinup az: pin-up – pin up

vavada casino: вавада зеркало – вавада официальный сайт

pin-up: pin-up – pin up azerbaycan

vavada: вавада зеркало – vavada

вавада зеркало: вавада зеркало – vavada вход

вавада казино: вавада казино – vavada

пин ап вход: пин ап казино официальный сайт – пин ап зеркало

pin up azerbaycan: pin up casino – pin up

pin up azerbaycan: pin-up – pin up az

вавада казино: vavada вход – vavada casino

пин ап казино официальный сайт: пинап казино – пин ап казино официальный сайт

The Real Person!

The Real Person!

https://pinupaz.top/# pinup az

The Real Person!

The Real Person!

verified Modafinil vendors: modafinil legality – modafinil 2025

The Real Person!

The Real Person!

safe online pharmacy: safe online pharmacy – generic sildenafil 100mg

The Real Person!

The Real Person!

verified Modafinil vendors: buy modafinil online – buy modafinil online

The Real Person!

The Real Person!

secure checkout Viagra: best price for Viagra – no doctor visit required

The Real Person!

The Real Person!

generic tadalafil: buy generic Cialis online – affordable ED medication

The Real Person!

The Real Person!

cheap Cialis online: secure checkout ED drugs – Cialis without prescription

The Real Person!

The Real Person!

safe online pharmacy: safe online pharmacy – discreet shipping

The Real Person!

The Real Person!

Cialis without prescription: cheap Cialis online – secure checkout ED drugs

legal Modafinil purchase: Modafinil for sale – legal Modafinil purchase

The Real Person!

The Real Person!

FDA approved generic Cialis: generic tadalafil – Cialis without prescription

http://modafinilmd.store/# legal Modafinil purchase

The Real Person!

The Real Person!

discreet shipping: best price for Viagra – safe online pharmacy

purchase Modafinil without prescription: modafinil 2025 – modafinil 2025

http://zipgenericmd.com/# best price Cialis tablets

The Real Person!

The Real Person!

modafinil legality: buy modafinil online – purchase Modafinil without prescription

best price for Viagra: Viagra without prescription – generic sildenafil 100mg

https://maxviagramd.com/# legit Viagra online

The Real Person!

The Real Person!

secure checkout Viagra: fast Viagra delivery – safe online pharmacy

reliable online pharmacy Cialis: Cialis without prescription – secure checkout ED drugs

https://maxviagramd.shop/# legit Viagra online

The Real Person!

The Real Person!

order Cialis online no prescription: online Cialis pharmacy – generic tadalafil

The Real Person!

The Real Person!

Amo Health Care: Amo Health Care – prescription for amoxicillin

The Real Person!

The Real Person!

where can i buy cheap clomid no prescription: can i get cheap clomid without insurance – cheap clomid price

The Real Person!

The Real Person!

amoxicillin 500 mg tablet price: buy amoxicillin over the counter uk – Amo Health Care

The Real Person!

The Real Person!

Amo Health Care: amoxicillin online canada – amoxicillin 500mg cost

how long does tadalafil take to work: cialis and high blood pressure – purchase brand cialis

cialis on sale: cialis free 30 day trial – cialis available in walgreens over counter??

tadalafil tablets 20 mg global: Tadal Access – where to buy cialis cheap

cialis one a day with dapoxetine canada: TadalAccess – cialis lower blood pressure

Pharm Au 24: pharmacy online australia – Online medication store Australia

Ero Pharm Fast buying ed pills online ed pills cheap

Online drugstore Australia: Buy medicine online Australia – Pharm Au 24

https://biotpharm.com/# buy antibiotics

Ero Pharm Fast: online ed treatments – get ed prescription online

Ero Pharm Fast: Ero Pharm Fast – online prescription for ed

buy antibiotics from india: BiotPharm – antibiotic without presription

Ero Pharm Fast how to get ed meds online Ero Pharm Fast

buy antibiotics over the counter: Biot Pharm – antibiotic without presription

https://eropharmfast.shop/# cheapest online ed meds

Ero Pharm Fast: where to get ed pills – buy erectile dysfunction pills online

Ero Pharm Fast: ed medicines – ed meds online

Pharm Au24 Pharm Au24 online pharmacy australia

Medications online Australia: Medications online Australia – Licensed online pharmacy AU

The Real Person!

The Real Person!

The maximum payout you can win while playing FootballX by SmartSoft is 100x the bet. Truth be told, you should be very fortunate to win it. We continue to update Football Ultimate Team search filters whenever we can based on your feedback, and with TU #9 we’re adding the ability to search by OVR ranges in your Club, SBCs, Rush, and Evolutions. Quarterback Fields of Glory offers 243 paylines and several bonuses, including Free Spins, the Foam Finger Bonus and the Fields of Glory Bonus. Once you have submitted your correct username, you will receive a password change instruction via email to your registered email address. This slot game, brought to players by Playtech, is one of the most realistic football slots available. Football Rules! has a 5-reel grid layout and offers 20 paylines. The slot game is full of football-fueled symbols, such as jerseys as icons, fans as wild symbols, and a stadium as the scatter. The betting range sits between 0.01 to 10.

https://edunenro1982.raidersfanteamshop.com/climatesciencespace-eu

The developer of Space XY cooperates only with licensed online casinos. In these casinos, bonuses are not usually subject to extreme wagering requirements. The client of the online casino can easily win back the gift received without large bets. If you’re searching for unique and exclusive crash crypto games, BC.Game is the perfect gambling site for you. Under the BC.Originals section in the casino menu, you’ll find a dedicated Crash category filled with exciting games offering high multipliers and rewarding gameplay. The graphics are simple yet engaging, delivering plenty of fun and the potential for big wins. You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page.

https://eropharmfast.com/# best ed pills online

Ero Pharm Fast: online ed drugs – where to buy ed pills

Online drugstore Australia pharmacy online australia Online drugstore Australia

ed meds on line: Ero Pharm Fast – Ero Pharm Fast

https://eropharmfast.shop/# Ero Pharm Fast

cheapest antibiotics: Biot Pharm – get antibiotics without seeing a doctor

Online drugstore Australia Pharm Au24 PharmAu24

Medications online Australia: Pharm Au24 – Pharm Au24

The Real Person!

The Real Person!

(Except for the headline, this story has not been edited by NDTV staff and is published from a syndicated feed.) All Scripts simple to understand.Simple to modificateSimple to reusethis asset easy to transform it to match of 12 players “I’ve done several zero-gravity simulation flights. They carve out a Boeing 747 and fly the plane in a parabolic pattern, so when the plane descends, everyone floats up. That was to get used to the feeling of weightlessness,” Flynn said. “So I think I’m going to have some fun with that when we’re up. I also did the NASTAR training in Philadelphia and experienced up to 5 G’s of pressure.” The article inspired Gates, who was just a freshman at Harvard University, and Allen to call Altair’s maker, Micro Instrumentation and Telemetry Systems, and promise the company’s CEO Ed Roberts they had developed software that would enable consumers to control the hardware. There was just one hitch: Gates and Allen hadn’t yet come up with the code they promised Roberts.

https://eloralproc1982.tearosediner.net/found-it-for-you

Scramble Words is the game for you. Take letters from below and make new words above to complete this word puzzle game. Whether you’re new to word games or a seasoned pro, there’s sure to be something to challenge you. Remember to get those bonus letters for a better score. There is a problem loading your cart right now Absolutely! Plinko is optimized for mobile devices, allowing players to enjoy this engaging game seamlessly on any smartphone, desktop, or tablet. Immerse yourself in a world where every sphere toss potentially earns coins. Use these coins to gain access to exclusive spheres and customized game arenas, giving your gameplay a personalized touch. Thank you for bringing this to our attention, and we apologize for any concerns you’ve experienced. We’re actively addressing the issue of negative balances, as well as other detailed problems, in our upcoming update. Stay tuned for improvements. For quicker assistance, please reach out to us on our fan page, YODA GAMES.Once more, we appreciate your patience and support.Best regards,Sylvia

The Real Person!

The Real Person!

В игре “Авиатор Краш-Игра” вас ждет невероятное путешествие в мир авиации и приключений! Станьте настоящим авиатором и взлетите с нами высоко в небо! Тут вам не придётся несколько часов изучать правила, играть просто, выиграть можно много. Если ещё и задействовать специальные стратегии, можно многократно увеличить шансы. Вы можете насладиться игрой и заработать внушительную сумму. Многочисленные стратегии в Aviator помогают фанатам азарта чаще выигрывать в онлайн казино париматч и получать максимум удовольствия. Игроки никак не взаимодействуют друг с другом с точки зрения геймплея, но могут общаться между собой и обмениваться впечатлениями. В одном раунде разрешено aviator игра делать одну или две ставки. Можно не делать ставку и просто отслеживать процесс на экране. Результат определяется при помощи генератора случайных чисел.

https://respekpeduli.org/%d0%bb%d1%83%d1%87%d1%88%d0%b8%d0%b5-%d1%81%d1%82%d1%80%d0%b0%d1%82%d0%b5%d0%b3%d0%b8%d0%b8-%d0%b4%d0%bb%d1%8f-%d0%b8%d0%b3%d1%80%d1%8b-%d0%b0%d0%b2%d0%b8%d0%b0%d1%82%d0%be%d1%80-%d0%be%d0%bf%d1%8b/

В списке игровых автоматов представлены около 2000 вариантов. На главной странице вы найдете набор самых популярных слотов. В основном меню приложения Пин Ап представлены все виды азартных игр: PinUp казиносы өз пайдаланушыларына ойын автоматтарында (слоттарда), карта және үстел ойындарында ойнауға, сондай-ақ спорттық (және ол ғана емес) оқиғаларға ставка жасауға мүмкіндік береді. Бұл нақты ақшаға құмар ойынмен уақыт өткізу үшін жоғары сапалы және танымал платформа.

The Real Person!

The Real Person!

Loading Preview UNINASSAU CARUARU É uma série lançada nos anos 60 sobre a noviça Bertrille e seu chapéu voador, junto com um grupo de freiras no convento San Tanco. Emissora: ABC. Emissora no Brasil: TV Excelsior, TV Record, Rede Globo, Warner e Rede Brasil. Transmissão Original: de 7 de setembro de 1967 a 3 de abril de 1970. Duração: AI-enhanced description Em 1980, o diretor Robert Altman resolveu filmar a série com atores de verdade. O roteiro é do cartunista Jules Feiffer (ex-assistente de Will Eisner na HQ Spirit ) e o filme é estrelado por Robin Willians (como Popeye) e Shelley Duval (como Olívia Palito). O resultado foi uma das melhores e mais fieis adaptações que uma história em quadrinhos teve no cinema. E a Amazon quer mesmo avançar pelo mercado de luxo. A gigante do comércio eletrônico acabou de lançar a plataforma Luxury Stores, pra se aproximar deste setor e trazer marcas de alto padrão para o seu leque de serviços. Até agora, Oscar de La Renta já entrou e é bastante esperado pela própria plataforma que outras grifes tomem a mesma decisão.

https://uniformessagitario.com/uncategorized/como-jogar-com-seguranca-no-jogo-jetx-bet-guia-completo-para-jogadores-brasileiros/

1. Create an Account Begin by signing up for an account on the Bolt platform. This will provide you with access to all its features. 캐리지 볼트에 대한 모든 것 Yuqori sifatli sleeve anchorlar, ko’pincha quyidagi materiallardan tayyorlanadi zanglamaydigan po’lat, alyuminiy yoki qattiq plastmassalar. Bu materiallar ularning uzoq muddatli ishlashi va metall yeyilishiga qarshi turishiga yordam beradi. Bu esa, korroziya kuchli ta’sir ko’rsatadigan joylarda ular uchun alohida muhimdir, masalan, suv ostidagi yoki kimyoviy moddalar bilan ishlaydigan sohalarda. The applications of anchor bolts are extensive, ranging from the construction of bridges and buildings to securing machinery and equipment in industrial settings. They are vital in seismic retrofitting, ensuring that structures can withstand earthquakes and other natural disasters. Additionally, anchor bolts are used in temporary structures such as scaffolding, providing the necessary support and stability for safe operations.

The Real Person!

The Real Person!

Table of Contents In JetX, the exciting casino game, you have the freedom to choose when to make your exit and claim your winnings. Simply click the ‘Collect’ button at the optimal moment to gather your earnings. Timing is crucial, as waiting too long and missing the opportunity before the jet explodes will result in no winnings. Mastering the art of withdrawal is key to succeeding in JetX. We believe in HONESTY, HARD WORK, and building LONG LASTING RELATIONSHIPS with our CLIENTS. At the end of the day, we know that we have delivered work that meets up to this. You can enjoy JetX at reputable online casinos such as Bitcasino, GG.bet, Thunderpick, and Cyber.bet. Just remember to claim your welcome bonus when you join. JetX is an online gambling game where players bet on a pixelated jet climbing higher in the atmosphere before crashing. The outcome is determined by a random number generator (RNG) displayed on a visual interface.

https://dreevoo.com/profile_info.php?pid=804683

As with any game of chance, there have been whispers of “JetX predictors” or “crash game hacks” circulating online. These often come in the form of software or betting systems promising to forecast the plane crash point in JetX. If you are a beginner, it takes some time to get used to the gameplay. The Jet X demo version is a great tool to fully learn the mechanics of the game and understand the algorithms without risking your own money. The demo mode is packed with all the features, so you will also get to watch the flight of the plane, and the increase in odds. Feel free to use the betting strategies above, practice them to see which one suits you best before you start playing for money. SmartSoft Gaming, a business that specializes in cutting-edge online casino games, is the creator of JetX. Expanding upon the crash game genre, JetX was created with an arcade-style UI and futuristic atmosphere in mind, making it playable by a wider range of players. When JetX was first released in 2019, its fast-paced action, social elements, and the possibility of huge prizes drew in gamers.

The Real Person!

The Real Person!

بدلاً من اللجوء إلى هكر لعبة الطيارة 1xbet، يمكنك تحسين أدائك بطرق قانونية وآمنة. تعلم عن استراتيجيات اللعب، وشارك في المجتمعات الخاصة باللاعبين للحصول على نصائح مفيدة. يمكنك أيضًا ممارسة اللعبة بانتظام لتطوير مهاراتك. هكر لعبة الطيارة مجانا في 1XBET كسبت كتير هكر لعبه الطياراة الله علي العبة بالإضافة للمعركة الكبيرة التي يمكن الإنضمام إليها والاستمتاع بالقتال بها يمكنك أيضا الاستمتاع بخدمة الروم أو خدمة الغرف, تقوم فكرة الغرف حول خوض منافسة بين فريقك وبين فريق لمدة زمنية محددة وفي تلك المدة يجب على أحد الفريقين تحقيق الهدف الخاص بالروم وهو قتل عدد مرات بعينه, هذا الروم اللاعب الذي يتم قتله لا يتم خروجه من لعبة Free Fire فري فاير مهكرة بل يتم النزول مرة أخرى.

https://test.bharatcarts.com/%d9%85%d8%b1%d8%a7%d8%ac%d8%b9%d8%a9-%d9%84%d8%b9%d8%a8%d8%a9-thimbles-%d9%85%d9%86-evoplay-%d9%84%d9%84%d8%a7%d8%b9%d8%a8%d9%8a-%d8%a7%d9%84%d9%85%d8%ba%d8%b1%d8%a8-%d8%a5%d8%ab%d8%a7%d8%b1%d8%a9/

هل ترغب في تحميل سكربت الطيارة 1xbet لتجربة هاك الطيارة والاستمتاع بخيارات جديدة ومثيرة؟ تُعد لعبة 1xbet Aviator طريقة فريدة ومثيرة للمراهنة على نتيجة رحلة طائرة افتراضية. تعتمد اللعبة على فرضية بسيطة: يختار اللاعبون نتيجة رحلة طائرة افتراضية، وإذا كانوا على حق، فإنهم يربحون المال. إحدى الميزات الرئيسية للعبة هي 1xbet سكربت الطياره، والذي يستخدم لتوليد نتائج الرحلة. ياسين تيفي حصلت لعبة RFS مهكرة، وهي لعبة متاحة في سوق Google Play ، على متوسط درجة في نطاق 4.1 من 5 وتستخدم على هواتف الاندرويد 4.3 أو أعلى حتى الآن. يتم تنزيله واستخدامه أكثر من مليون مرة. لا تكن أحمق و قم بتجربتها.

The Real Person!

The Real Person!

For players on the go, Jetx Jeux Dargent also offers a secure mobile app for Android and iOS users. The app includes all the features of its desktop version, including real-time betting from anywhere in the world! Now you can place your bets on Jetx Jeux Dargent while you’re on the go without having to worry about security or convenience. JetX CBet Casino For players on the go, Jetx Jeux Dargent also offers a secure mobile app for Android and iOS users. The app includes all the features of its desktop version, including real-time betting from anywhere in the world! Now you can place your bets on Jetx Jeux Dargent while you’re on the go without having to worry about security or convenience. CBet Casino leaves a pleasant impression and is suitable for playing JetX. The platform offers a nice welcome bonus of $400, which can be used in a crash game. The site is compatible with Android and iOS mobile devices, so you can bet on airplane flight anytime you want. If you want to take your mind off CBet JetX, there are 8,000 other gambling activities waiting for you.

https://innov-system.com/2025/06/04/bgamings-plinko-on-1xbet-full-install-guide-and-review-for-pakistani-players/

RESPONSIBLE GAMING: jetxgame is a responsibly gaming advocate. We make every effort to ensure that our partners respect responsibly gaming. Playing in an online casino, from our perspective, is intended to provide pleasure. Never be concerned about losing money. If you’re upset, take a break for a while. These methods are meant to assist you in maintaining control of your casino gaming experience. The Parimatch website developers have done their best to cater to the needs of mobile gamblers. As a result, the platform’s browser-based version has a fairly mobile-friendly design, is fast downloaded, and is compatible with Windows, Android, iOS, and other popular operating systems. However, you can still download the Parimatch Casino JetX app on your Android or iPhone to make your betting journey even more effortless and convenient.

The Real Person!

The Real Person!

Pro ty, kteří chtějí hrát Bitcoin Plinko, se při výběru správné platformy uplatňuje řada prvků. Stejně jako jedna bota nesedí všem, i výběr dokonalé platformy vyžaduje promyšlený hodnotící proces. Zde jsou některé prvky, které zvažujeme při doporučování krypto-přátelského Plinko kasina: Všechno to začalo v roce 1983 a okamžitě se stalo hitem. Komu by se nelíbilo sledovat, jak ty žetony poskakují a hledají sladké ceny? No, popularita Plinko nezůstala v televizi. Ukázalo se, že online kasina a mobilní aplikace tuto hru také milují! Nyní můžete hrát klasický herní zážitek Plinko odkudkoli s některými moderními výhodami. Představte si elegantní grafiku fixované desky, přizpůsobitelné funkce a dokonce i možnost hrát s kryptoměnami v některých online kasinech. Je to stejné jako Plinko zábava, kterou znáte a máte rádi, ale s digitálním zvratem!

https://www.dermandar.com/user/nalezenozde/

Online kasina nabízející Plinko podporují různé platební kanály: Jaká je podle vás nejlepší strategie na Plinko? Mám zůstat u nižších sázek? Plinko Casino je jednoduchá, ale mimořádně zábavná hra, která si rychle získala oblibu mezi hráči v online kasinech. Díky svému jedinečnému principu a možnosti vysokých výher se stala populární nejen u zkušených hráčů, ale i u nováčků, kteří hledají rychlou a napínavou zábavu. V této recenzi se podíváme na to, jak Plinko CZ funguje, kde si ji můžete zahrát, jaké bonusy jsou dostupné, a co všechno byste měli vědět, než vsadíte skutečné peníze. Česká hráčská komunita si vybudovala silný zájem o Plinko což je dokázalo jejich pozitivní recenze. Hráči ocenili hru Plinko kvůli její jednoduchosti a rychlé dostupnosti. Podle českého hráče není nutné mít expertní znalosti kasino her pro zážitek z Plinko. Mnoho hráčů souhlasí že Plinko nabízí možnost získat okamžité výhry což ji činí ideálním výběrem pro ty, kteří preferují krátké a napínavé herní zážitky.

The Real Person!

The Real Person!

Zasady gry opisane są na reprezentacji online, gdzie można również pobrać aplikację na telefon lub grać przez przeglądarkę. Co musisz zrobić, aby rozpocząć grę w Aviator za pośrednictwem kasyna Mostbet: O site oficial 1win bet 1winbr.br e apostar em desporto, casinos, jogos e torneios. Suporte para diversas moedas, transacoes rapidas, promocoes e cashback. Jogue confortavelmente no seu PC ou atraves da aplicacao. Oczywiście każde kasyno zdaje sobie sprawę, że bez kontrastu nie byłoby w stanie długo zatrzymać uwagi i miłości własnych klientów, więc wprowadza kilka gier podobnych do Aviator. Głównym z nich jest 1000x Busta. W zasadzie wszystkie te maszyny to gry crash z minimalnymi różnicami, które dotyczą głównie designu. 1win app download apk 1win1034.top .

https://www.unisons.fr/wiki/?toughcadere1987

Read more about 1wins.am here. You don’t need to enter a promo code during registration; you can receive a bonus of 500% up to 200,000 rupees on your deposit. This means you have a unique opportunity today to increase your initial balance and place more bets on your favorite sports events. At 1Win Casino, players… GRAJ ODPOWIEDZIALNIE: luckyjet-games jest niezależną stroną internetową, która nie posiada żadnych powiązań z promowanymi przez nas witrynami. Przed zaangażowaniem się w jakąkolwiek formę hazardu upewnij się, że spełniasz wszystkie wymogi prawne i kryteria wiekowe obowiązujące w Twojej jurysdykcji. Naszą misją na stronie luckyjetgames jest dostarczanie treści informacyjnych i rozrywkowych wyłącznie w celach edukacyjnych – kliknięcie tych zewnętrznych linków spowoduje całkowite opuszczenie tej strony.

The Real Person!

The Real Person!

No entanto, antes de se cadastrar em qualquer plataforma, é preciso escolher uma operadora confiável. Abaixo, listamos os melhores sites e as ofertas promocionais para quem quer jogar o Jogo Fortune Tiger, ou Jogo do Tigrinho e apostar. Separamos abaixo as cinco principais opções de casas para jogar: Existem diversos sites de cassino que contam com bônus especiais para que o seus cliente cadastrado jogar no Jogo de Tigrinho. Por isso, vale a pena acessar a seção de promoções da plataforma selecionadas para conferir as opções disponíveis. O próprio Jogo do Tigrinho Fortune Tiger traz símbolos bônus que aparecem aleatoriamente e trazem rodadas extras e multiplicadores maiores. Se você aprecia a experiência de jogo com Fortune Tiger, talvez também esteja interessado em outros jogos cativantes da PG Soft. Descubra as aventuras únicas e os gráficos ricos de Fortune Rabbit e Fortune Mouse, duas outras máquinas caça-níqueis que prometem uma experiência de jogo emocionante e lucrativa.

https://cgmood.com/ted-schmidt

Agora pessoal, caso você tenha interesse em sempre estar atualizado nos horários que realmente estão pagando, acesse o site abaixo e tenha acesso ao FORTUNE TIGER CARTAS 10X, sempre os horários se atualizam..HORÁRIOS SEMPRE ATUALIZADOS DO FORTUNE TIGER! O pagamento máximo do Fortune Tiger é de 2.500x o valor da sua aposta, sendo que o símbolo do tigre é o que mais paga e que também substitui qualquer um dos ícones, seja ele um dos que paga mais ou menos. O Fortune Tiger, por ser um jogo baseado em sorte, apresenta tanto vantagens quanto desvantagens. Abaixo, você encontrará uma tabela que resume os principais pontos de cada lado: O Fortune Tiger, por ser um jogo baseado em sorte, apresenta tanto vantagens quanto desvantagens. Abaixo, você encontrará uma tabela que resume os principais pontos de cada lado:

The Real Person!

The Real Person!

Der Früchte Slot von Merkur ist ein absoluter Liebling der Casino-Fangemeinde. Die Spielregeln sind einfach zu verstehen – das perfekte Spiel für Slot-Neulinge. Mit dem Sweet Bonanza Online Slot kannst du bereits im Basisspiel absolute Traumgewinne erzielen gewinnen. Der Höchstgewinn liegt bei 2,11 Millionen €. Die Sweet Bonanza Auszahlungsquote liegt bei 96,00 %. Hier geht es zur Sweet Bonanza Gewinntabelle, in der du sämtliche Liniengewinne für die einzelnen Spielsymbole nachvollziehen kannst. Theater & Bühne Sweet Bonanza ist ein Spiel, das Unterhaltung und Spannung auf höchstem Niveau bietet. Mit seinem fröhlichen Design, den innovativen Features und der Chance auf große Gewinne ist es ein Muss für jeden Slot-Fan. Drehen Sie die Walzen, genießen Sie die Süßigkeiten und entdecken Sie die Gewinne – Sweet Bonanza wartet auf Sie!

https://pakhie.com/blogs/40353/Klicken-Sie-auf-diesen-Link

Bei „Sweet Bonanza Xmas™“ handelt es sich um eine Videoslot mit 6 Walzen und 5 Reihen. 8 oder mehr identische Symbole gewinnen an beliebiger Stelle auf dem Bildschirm. Die Gesamtanzahl der identischen Symbole auf den Walzen bestimmt die Höhe des Gewinns laut Gewinntabelle. Narrenzunft – Brauchtum Krampus Du kannst die Walzen dieses festlichen Slots auf deinem Smartphone oder Tablet drehen, da das Spiel vollständig responsiv ist und auf jeder Bildschirmgröße hervorragend funktioniert. Um die Walzen unterwegs zu drehen, stelle einfach sicher, dass du über eine zuverlässige Internetverbindung und ausreichend Akkulaufzeit verfügst, und schon kann es losgehen! Aufgrund seiner erfrischend anderen Art der Drehungsauswertung werden bei Sweet Xmas Bonanza™ mehr gleiche Symbole für einen Gewinn als bei anderen Online Automaten benötigt. Sie können Sie in unserer Tabelle nachsehen, welche Symbole es gibt und wie viele Sie benötigen (beim Einsatz von 100 Euro):

The Real Person!

The Real Person!

One of the most enticing features of Sweet Bonanza is its generous Free Spins feature. Players can trigger this bonus round by landing at least four scatter symbols. During the free spins, players may encounter multiplying bombs, which can exponentially increase winnings. Sweet Bonanza is more than just a typical slot game; it’s a vivid, engaging experience that has captivated Canadian gamers with its candy-themed allure and multiple winning opportunities. Its combination of visually appealing graphics, innovative gameplay mechanics, and the potential for significant payouts makes it a standout choice in the world of online slots. As a Canadian sensation, Sweet Bonanza offers an enthralling escape into a world of vibrant colors and exciting possibilities. As these 1000 slots often go, you don’t notice a lot of difference a lot of the time. For all intents and purposes, Sweet Bonanza 1000 looks the same and plays the same, but Pragmatic Play has worked in a number of tweaks and adjustments to make the experience a rather different kettle of fish. Though, in saying so, there are things about Sweet Bonanza 1000 which make its differences less pronounced than other 1000 slots have been.

https://onlinedigitalbookmark.com/page/business-services/https-sweetbonanzai-com-

Big Bass Xmas Xtreme slot game has a very high volatility rate. This means that the slot payouts are less often, but the chance to hit big wins is bigger. Connect with us The latest Big Bass slot sets the mood for the upcoming festive season At Ladbrokes Casino, we pride ourselves on delivering an unparalleled online gaming experience for Belgian players and gamblers across Europe. As the casino king in Belgium, we offer a vast casino games catalog, packed with popular games, traditional casino games, and new casino games that guarantee endless excitement and the chance to win big prizes. Whether you’re a fan of slots, poker, or roulette, our live casino and online casino games provide a thrilling gaming experience for every type of casino player. Picture yourself on a fishing adventure, but instead of catching actual fish, you’re aiming to hook some special fish that could reward you with a big cash prize. In the Big Bass Amazon Xtreme slot, you can go fishing and win up to 10,000x. Furthermore, while you’re spinning slot reels, you might just land a random special fish; these fish have the potential to boost your winnings by up to 50x! Learn more about this incredible slot in our Big Bass Amazon Xtreme slot review.

The Real Person!

The Real Person!

Mega Fishing online casino balık oyunu, ödeme tablosu menüsünde kategorilere ayrılmış geniş bir hedef yelpazesine sahiptir. Hedef yenildiğinde karşılık gelen bir çarpan kazanırsınız: Mega Fishing anlaşılması kolay bir arayüze sahiptir, bu nedenle hem masaüstü bilgisayarlarda hem de iOS ve Android ile çalışan mobil cihazlarda hızlı ve sezgisel gezinme deneyimi yaşayacaksınız. Bu balık online casino oyununu nasıl oynayacağınızı öğrenmek için bu kılavuzu takip edebilirsiniz: Lütfen emailinizi kontrol edin! Balık oyunu kumar, genellikle bir grup insan tarafından oynanır ve oyuncular, balıkları vurarak puan kazanırlar. Oyuncuların kazancı, balıkların boyutu ve türüne göre belirlenir. Oyuncular, oyun sırasında harcanan mermi sayısını da takip etmelidirler, çünkü mermi fiyatları pahalı olabilir.

https://rpgplayground.com/members/siziniinbuldum/profile/

Yatırımsız bir şekilde big bass bonanza oynamak mümkün değil gibi görünüyorsa da deneme bonusu veren sitelerden oynamak mümkündür. Deneme bonusu bahis firmalarının kullanıcı çekmek için verdiği site içi paradır. Bu para ile yatırım yapmadan istediğiniz zaman bahis oynayabilirsiniz. Bunun haricinde, slot oyunlarına özel free spin promosyonu gibi çeşitleri görebilirsiniz. Ayrıca, big bass bonanza free spin olarak, siteler, yatırım işlemini yapan şahıslara, yatırdıkları paranın belirli bir sayısında free spin olarak tanımlanmış promosyon seçeneğini de verebilmektedir. Oyunu oynamak için site bulmak basittir. Zor olan güvenilir siteleri bulabilmektir. Çünkü günümüzde bahis sitelerine olan güven azalmaktadır. Özellikle kaçak bahis firmalarının yurt dışı kaynaklı olması uğradığınız haksızlıklarda tek başına kalmanıza neden olur. Bu sebeple bizler de sizler için en iyi ve güvenilir bahis sitelerini araştırdık. Bu sitelerden bazıları ise şunlardır:

The Real Person!

The Real Person!

Las probabilidades de ganar Lucky Jet dependen del multiplicador al eyectarse. Cuanto mayor sea el multiplicador, menores serán las probabilidades de ganar. Por ejemplo, si se expulsa con un multiplicador de 10, ganará el 90% de las veces. Sin embargo, si se expulsa con un multiplicador de 100, sólo ganará el 10% de las veces. No hay un momento perfecto; depende de tu estrategia y de cuánto estés dispuesto a arriesgar. Algunos prefieren retirarse temprano para asegurar ganancias, mientras que otros esperan a obtener mayores multiplicadores. Esta estrategia está diseñada para jugadores que prefieren asegurar pequeñas ganancias constantes y evitar grandes pérdidas. Consiste en retirar la apuesta en los primeros segundos del juego, cuando el multiplicador está entre 1.1x y 1.3x.

https://bosswin777.net/balloon-app-lo-bueno-lo-malo-y-lo-que-debes-evitar/

Desarrolladores ¡Aprovecha la promoción y únete ahora a nuestro servicio Premium! * Estudio realizado por Odoxa sobre 2.594 partidos (fútbol, tenis y baloncesto) del 01 09 2023 al 30 12 2023, nº1 para el 37 % de las cuotas registradas. Políticas de bplay The game perfectly blends accessibility and depth, making it an addictive experience that keeps players coming back for “just one more shot”. Whether you’re a football fan or just looking for an engaging arcade experience, Ultimate Penalty will provide you with endless hours of entertainment. Whether you’re looking for a fun way to pass the time or want to test your skills against friends, this game offers endless entertainment. Download now and start kicking! Los periféricos como los gamepads simulan de manera más realista la sensación de los deportes reales, proporcionando un control más preciso y una variedad de opciones de operación.

The Real Person!

The Real Person!

(+91) 95881 30349 Answer :- Color prediction games, like many forms of online gambling and betting, are typically available to adults who meet certain legal and regulatory requirements. The specific eligibility criteria may vary depending on the country or jurisdiction where the game is being offered, but here are some general guidelines: Maxway Infotech is a known technology company that offers various kinds of software development, game development, web development, and Cricbet99 . Maxway Infotech was founded with the goal of offering cutting-edge technological solutions. The company is widely known for its commitment to quality, client satisfaction. In recent years, color prediction games have been increasingly so popular. Color prediction games are not only a simple game for users but also for game development companies. These games provide players an interesting and engaging experience.

https://www.acpianificazionecontrollo.it/senza-categoria/review-teen-patti-gold-by-live-dealers-a-thrilling-casino-game-experience-for-uae-players/

The key to making this hair colour look expensive is shine, so invest in a good hair mask to keep your colour looking glossy. 91 club is new kind of mobile color gaming app where you can play colour games plus multiple games. These games are skill based games where you can play and start winning reward. It is same like daman games. – Replace path to game.app with the actual path to the game file (you can drag the app into Terminal to auto-fill the path).sudo xattr -rd com.apple.quarantine path to game.app A demo trading account lets you experience all of the features that eToro has to offer: The key to making this hair colour look expensive is shine, so invest in a good hair mask to keep your colour looking glossy. Numerous prediction-based games, including Wingo, Color Trading, Big Small Game, Aviator, Slots, Teen Patti, and casino games, are available at 82 Lottery. It requires a minimum deposit of ₹100 and is designed for ease of use. It offers a seamless user experience and secure transactions via USDT, bank transfers, and UPI. A sign-up bonus of ₹88 is available to new customers. With its wide range of games and lucrative promos, 82 Lottery provides gamers with a fun and safe online gaming experience.

The Real Person!

The Real Person!

Dragon Tiger is a popular casino game that originates from Asia and has gained immense popularity in online casinos worldwide. It is a simple and fast-paced card game that involves two main betting options: Dragon and Tiger. The objective of the game is to correctly bet on which hand, Dragon or Tiger, will have the highest card value. The Dragon and Tiger bets will win if the chosen hand gets the higher card. Ties lose half. The following return table shows a house edge of 3.73%. A: No. Encrypted or not, a casino could cheat the player in any game, except sports betting, any time they wished. In the case of an encrypted casino, the operator could choose a Server Seed that causes the player to lose after the bet is made. If the player catches them in a hash mismatch, which I think very few players bother to check, the casino can simply ignore the accusation or deny it without comment. This is exactly what happened to me at Wixiplay.

https://pragyakunja.edu.np/aviator-on-pin-up-everything-you-should-know-before-you-bet/

Check your inbox and click the link we sent to:youremail@gmail Bonds, also known as fixed income securities, are issued by companies and governments as a way of raising money. They’re basically an ‘I.O.U’ – designed to provide a regular stream of income (which is normally a fixed amount) over a specified period of time. Space XY stands firmly as a breath of fresh air in a world where some crash games that are years old or, in some cases even a full decade old, could be considered by some players as giving a somewhat stale experience. Space XY is relatively new, having been developed by BGaming in January 2022. The modern design is eminently noticeable, resulting in one of the most visually stunning crash games of all. Do not forget that if your intuition fails you and you do not have time to collect the money before the Rocket leaves the game, then the bet funds will burn out. Space XY is a great way to have fun, tickle your nerves and win by expanding your wallet!

The Real Person!

The Real Person!

Space XY is a great example of why crash-style games have become popular at many online casinos. This thrilling space-themed crash game was created by BGaming and has been one of the top specialty casino games since it hit the market in January 2022. Provably Fair makes it easy to verify the fairness of each round and ensure a truly random outcome. Aviator, Lucky Jet fans – as well as all seasoned players of online casino games – will be delighted by this new take on classic space-themed gambling! With any device connected to the Internet close at hand, you can now embark on an exciting journey into outer space in no time! Voicify is taking its first steps into new niches for itself. Read more on the official website of our partner. Bank Wire Transfers usually take from 3 to 5 business days, depending on ones typing skills. Pai Gow is a popular Asian game played with Chinese dominoes, space XY bonus symbols without risk of loosing any money. It brings you closer to landing a winning combination and then doubles the payout, the majority of these games come from the online slots section.

https://abdullah.pinnaclefirearmsandtraining.com/real-world-events-that-affect-rocket-game-popularity-predict-trends/

XY Game Booster – PUBG Optimizer Mod download xy vpn mod apk and unleash yourself in the beauty of this amazing application. Start a journey of complete safety and security without worrying if anything whatsoever. You are offered with a range of amazing tools and features that makes it easy for you to enjoy more safety and access to internet connection and content. While here you get access to amazing premium features and functions all for free. download xy vpn mod apk and unleash yourself in the beauty of this amazing application. Start a journey of complete safety and security without worrying if anything whatsoever. You are offered with a range of amazing tools and features that makes it easy for you to enjoy more safety and access to internet connection and content. While here you get access to amazing premium features and functions all for free.

The Real Person!

The Real Person!

كيف يعطي موقع 1xBet الأولوية لأمن اللاعب؟ تأخذ شركة 1xBet أمن اللاعب على محمل الجد وتستخدم إجراءات متقدمة لحماية معلوماتك. إنهم يستخدمون تقنية تشفير SSL للتأكد من أن جميع البيانات المنقولة بينك وبين الكازينو تظل آمنة. وهذا يعني أن بياناتك الشخصية ومعاملاتك المالية محمية من الوصول غير المصرح به. اشتهرت اللعبة بسبب سهولة استخدامها ومزيجها بين الحظ والاستراتيجية، الامر الذي يجعلها مثيرة ومليئة بالتحديات. كما أنها متاحة على كازينوهات متعددة ومشهورة مثل 1xBet وغيرها.

https://kedai1.niaganify.com/%d9%84%d8%b9%d8%a8%d8%a9-%d8%a7%d9%84%d8%b7%d9%8a%d8%a7%d8%b1%d8%a9-aviator-%d8%a7%d9%84%d9%84%d8%b9%d8%a8-%d8%a7%d9%84%d8%aa%d8%ac%d8%b1%d9%8a%d8%a8%d9%8a-%d8%a8%d8%af%d9%88%d9%86-%d9%82%d9%8a%d9%88/

فوتوشوب PS مهكر لعبة المهكرة جيدة ام لا كذلك، فإن نشر برامج مزيفة والترويج لأدوات مثل “هكر لعبة Crash 1xBet مجانًا” ليس إلا شكلًا من أشكال الاحتيال. هذه البرامج لا يمكنها اختراق النظام أو التغلب على خوارزميات الحماية المتقدمة التي تعتمدها المنصة. الحل الوحيد الآمن للمراهنة هو تحميل تطبيق 1xBet الرسمي مباشرة من موقع الشركة. • سكربت الطياره 1xbet Crush برنامج اضافي داخل لعبه الطياره. لكن يمنحك الوصول الى جميع الرهانات وربح الاموال والاكواد المخفيه على جهازك.

The Real Person!

The Real Person!

Space XY is an exciting new game that takes players on a virtual rocket ride through space. The screen shows the coordinate system in which your rocket takes off. Place your bet and get your rocket out before it disappears into endless space. Bet on a rocket’s ascent as the multiplier climbs in Rocket X! Cash out before it vanishes into space to lock in your wins. This 1Play title offers simple yet gripping gameplay with dual bets, available on 1Win. Go for safe cash-outs or risk it all for astronomical payouts! Spribe’s Aviator is a heart-racing crash game where you cash out before the plane vanishes. Available on the Aviator Game website, it’s smooth on desktops and mobiles. Here’s the rundown: Aviator Game рџ‡·рџ‡є 🇺🇦 рџ‡°рџ‡ї 🇦🇿 🇹🇷 🇧🇷 🇮🇳 рџ‡єрџ‡ї 🇵🇪 🇨🇱

https://exclusive.codekat.com/canadian-deposit-methods-compared-for-aviator-by-spribe/

A Division of NBCUniversal. JJ Peterka & Ukko-Pekka Luukkonen explore Prague EDM@SJS: Toffoli scores goal against Calvin Pickard Speed across plains, cities, water, volcanos, and much more. Everything is connected! These five attackers hold strong chances of netting in their upcoming fixtures. Betting markets offer favourable odds for the anytime goalscorer bets. It’s a similar case for the betting odds, though favorites don’t always have a ” – ,” especially in sports like baseball, hockey or soccer where final results are often decided by one run or one goal. It’s especially the case in soccer since matches can end in draws, whereas a winner is declared in almost every other sport because of overtime rules. However, in most cases, the favorite will have a ” – ” in front of its moneyline odds while the underdog will always have a “+ .”

The Real Person!

The Real Person!

Nowy!!! OTRZYMAJ OFERTĘ – wypełnij 20-sekundowy quiz i otrzymaj spersonalizowaną ofertę Odrzuć Because have a workplace inside the Asia, you will be able to talk with alive service within the Hindi. Analysis out of prior events come in real time, in addition to analysis of current live occurrences. Through the use of it tool to assist you inside the finest anticipating the fresh game’s outcome, your enhance your odds of putting a profitable bet. Bookmaker 1win is a reliable site to possess playing to the cricket and you will other football, founded inside 2016. From the short time of the existence, the website features attained a wide listeners. 1win’s fundamental working licenses are given by Bodies of Curacao. The new readily available have from the 1win are all away from an excellent sportsbook one to isn’t entirely concerned about sports betting. Because they can be a bit limited, he is some of the far more wanted-just after features by the punters. In this respect, they is a cash aside ability, as well as the choice for multi’s via a gamble creator form. For example, Visa has a deposit limitation of $step 1,one hundred thousand, while you are Primary Currency features a threshold away from $750.

http://www.redsea.gov.eg/taliano/Lists/Lista%20dei%20reclami/DispForm.aspx?ID=3007630

20Bet kasyno obsługuje również przelewy finansowe oraz skromniej tradycyjne procedury, tego typu w który sposób karty przed… CHÍNH SÁCH 20Bet kasyno obsługuje również przelewy finansowe oraz skromniej tradycyjne procedury, tego typu w który sposób karty przed… sportingbet+bet Na prostu wpisz swoje imię, link e-mail i jest to, w czym potrzebujesz obsługi, a odpowiedź pojawi się w ciągu 24 godzin. Strona wydaje się być zar… Rất tiếc, sản phẩm này hiện không tồn tại. Hãy chọn một phương thức kết hợp khác. Bon Nuts, Ground Floor, SKJ International Vintage, H.No : 8, 2-577 1 A 4, Rd Number 7, Banjara Hills, Hyderabad, Telangana 500034+91 89089 01213Locate us sportingbet+bet © Copyright 2020. Sublime Kupa. Tüm Hakları Saklıdır. Para yatırma ve çekme işlemleri Mostbet hesabınızdan, çeşitli ödeme yöntemleri kullanılarak yapılabilir. Bunlar arasında banka havalesi, kredi kartları, e-cüzdanlar ve kripto afin de birimleri bulunmaktadır. Bu basit adımlar, Mostbet’in Windows versiyonunu cihazınıza kolayca yüklemenizi sağlar. İndirme ve kurulumla ilgili daha fazla bilgi ve destek için Mostbet Türkiye’nin web sitesini ziyaret edebilirsiniz. Eğer hesabınıza erişimde sorun yaşarsanız, şifremi unuttum seçeneği ile şifrenizi sıfırlayabilir veya 24 7 canlı destek hattından yardım alabilirsiniz. Mostbet, kullanıcılarının sorunsuz bir giriş yapabilmesi için kolay ve güvenli bir platform sunar.

The Real Person!

The Real Person!

Tout le monde dit que gagner un match après un tour de penalties est une victoire injuste. Mais nous devons reconnaître l’émotion que les penalties ajoutent à une finale. Pensez à la tension du joueur avant de lancer et du gardien de but qui sait que des millions de personnes le regardent avant de réussir ou pas le miracle. Final Kick: Football en ligne pour Android vous permet de jouer à revivre ces moments-là. Les détails de cette offre s’appliquent aux utilisateurs ayant un compte Nintendo dont le pays associé est le même que celui de ce site web. Si le pays enregistré dans votre compte Nintendo est différent, les détails de cette offre peuvent être ajustés (par exemple, le prix sera affiché dans la devise locale). Le seul propriétaire de la marque, du jeu, de l’identité Penalty Shoot-out Game est la société Evoplay -. evoplay.games

https://properksa.com/2025/07/09/jet-x-quels-navigateurs-garantissent-une-meilleure-stabilite/

NFTshoout.co is a play to earn NFT football game where players earn shoo token for winning penalty shootouts. NFT shootout will soon have a scholarship program for scholars to earn crypto while gaming soccer on the metaverse Además, los aparatos de calibración tienen una extensa utilización en el área de la protección y el supervisión de estándar. Permiten localizar posibles fallos, evitando mantenimientos onerosas y daños a los aparatos. También, los información generados de estos dispositivos pueden emplearse para perfeccionar procesos y mejorar la presencia en sistemas de consulta. Además, los aparatos de calibración tienen una extensa utilización en el área de la protección y el supervisión de estándar. Permiten localizar posibles fallos, evitando mantenimientos onerosas y daños a los aparatos. También, los información generados de estos dispositivos pueden emplearse para perfeccionar procesos y mejorar la presencia en sistemas de consulta.

The Real Person!

The Real Person!

Download Predictor Spaceman 18121712.apk by Prediksi spaceman. Sekali klik untuk menginstal file XAPK APK di Android! Terima kasih atas peringkat dan umpan balik Anda! Download APK on Android with Free Online APK Downloader – APKPure Download APK on Android with Free Online APK Downloader – APKPure Sekali klik untuk menginstal file XAPK APK di Android! Anda sudah menilai. Sekali klik untuk menginstal file XAPK APK di Android! Anda sudah menilai. Anda sudah menilai. Download APK on Android with Free Online APK Downloader – APKPure Anda sudah menilai. Download APK on Android with Free Online APK Downloader – APKPure Terima kasih atas peringkat dan umpan balik Anda! Download APK on Android with Free Online APK Downloader – APKPure Sekali klik untuk menginstal file XAPK APK di Android! Sekali klik untuk menginstal file XAPK APK di Android!

https://cupa.co.ke/fitur-unik-dalam-slot-starlight-apakah-layak-dicoba/

BOT SPACEMAN PREDICTOR slot apk terpercaya BOT SPACEMAN PREDICTOR apk slot gacor BOT SPACEMAN PREDICTOR slot apk terpercaya This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data. BOT SPACEMAN PREDICTOR link slot apk BOT SPACEMAN PREDICTOR link slot apk BOT SPACEMAN PREDICTOR link slot apk This website is using a security service to protect itself from online attacks. The action you just performed triggered the security solution. There are several actions that could trigger this block including submitting a certain word or phrase, a SQL command or malformed data. BOT SPACEMAN PREDICTOR slot apk terpercaya

The Real Person!

The Real Person!

Se as dificuldades persistirem, contate o administrador deste site. O slot fortune rabbit demo é a melhor alternativa para quem quer aprender a jogar esse slot machine. Aposte sem gastar dinheiro, de graça, para conhecer os recursos e como funciona o sistema de ganhos do jogo. Vamos mostrar a você como jogar o jogo do coelhinho no modo demo, além de dar dicas sobre aprimorar ainda mais o seu jogo. Bônus de Indicação – R$20,00 pessoaUsuários VIP-aproveite bônus VIP Diário Semanal Mensal Olhando para a mecânica por trás do jogo, percebe-se que, quanto maior o número de apostadores no joguinho do coelho que proporciona uma renda adicional, mais elevadas se tornam as probabilidades de se obter uma jogada sem custo ou bônus. As chances de acertar combinações e ganhar bônus são idênticas ao jogo original, mas no coelhinho demo os ganhos são tão fictícios quanto a banca. Ou seja, quando enfim se sentir confiante para tentar ganhar de verdade, será preciso escolher uma plataforma para depositar e começar a jogar.

https://www.nely.mi2a-innovation.com/demo-sugar-rush-xmas-o-que-esperar-da-versao-natalina

Símbolos de pagamento menores: cenoura, foguete e moeda. A PG Soft é uma renomada provedora de jogos de cassino online com sede em Malta. Estabelecida em 2015, a empresa rapidamente ganhou reconhecimento por seus inovadores e visualmente deslumbrantes jogos de caça-níqueis. A PG Soft ganhou inúmeros prêmios da indústria, incluindo o prestigioso EGR B2B Award para Jogo do Ano, cimentando sua posição como uma força líder na indústria de iGaming. Fortune Rabbit também oferece uma versão Demo gratuita que os jogadores podem acessar em nosso site. Este modo demo permite que os usuários experimentem os recursos, mecânicas e jogabilidade do jogo sem qualquer risco financeiro. É uma excelente oportunidade para se familiarizar com Fortune Rabbit e decidir se você quer jogar com dinheiro real.

The Real Person!

The Real Person!

Le RTP est de 96,71 % avec une volatilité élevée, idéale pour les joueurs recherchant de gros gains. Que vous soyez en déplacement ou confortablement installé à la maison, la facilité avec laquelle vous pouvez vous engager dans ces jeux est simplement inégalée. Avant de plonger dans le vif du sujet, éclairons les symboles de Big Bass Bonanza. Considérez-les comme plus que de simples éléments décoratifs ; ils sont la clé pour déverrouiller des bonus palpitants et faire grimper vos gains. En matière de visuels, Big Bass Bonanza brille vraiment en tant que jeu de machine à sous en ligne, éblouissant les joueurs par son imagerie vibrante. Il capture l’essence d’une aventure de pêche avec des graphismes de style cartoon, complétés par des effets sonores qui vous plongent directement dans le thème. Une stratégie efficace consiste à se concentrer sur les tours gratuits, car ils offrent des opportunités accrues de gains significatifs. Maintenir un budget de jeu et établir des limites de perte sont également des pratiques recommandées pour une expérience de jeu responsable. Ce casino se distingue par sa large sélection de jeux et la facilité de navigation sur le site.

https://chemetronparts.com/big-bass-bonanza-revue-complete-et-version-mobile/

Vous voulez recevoir nos dernières actualités ? Nos nouveaux bonus, articles de blog et encore pleins d’autres choses ? Inscrivez-vous ! Frаnçоіs Jеlіus critique et rédacteur d’articles |a examiné CashedCasino Cet article prend 15 minutes à lire et comporte 2941 mots. Vous pouvez choisir d’activer ou de désactiver tout ou partie de ces cookies, mais la désactivation de certains d’entre eux peut affecter votre expérience de navigation. Je vais rester sur le concept mais que ça ne vous empêche pas de citer d’autres jeux à côté. Ce site utilise des cookies Abonnement terminé La machine à sous Sweet Bonanza™ est une machine à sous vidéo à 6 rouleaux de 5 lignes. On ne parle pas de ligne de paiement ici, pour créer une combinaison gagnante, il suffit de faire atterrir de 8 à 12 symboles identiques n’importe où sur les rouleaux. C’est un jeu simple, mais avec un petit grain de folie et de charme pour vous amuser pendant des heures.

The Real Person!

The Real Person!

“Freedom Games se complace en compartir un emocionante resumen lleno de revelaciones, videos de primera vista y actualizaciones de nuestros próximos títulos”, dijo Benjamin Tarsa, Director de Publicaciones de Freedom Games. «¡Nuestra primera exhibición de E3 es solo el comienzo, y nos sentimos honrados de tener la oportunidad de compartir nuestros planes futuros con audiencias digitales!» Como corresponde a un representante clásico del género de defensa de la torre, la misión del jugador en Kingdom Rush para PC, y etc. es defender la base contra las subsiguientes oleadas enemigas, gradualmente más poderosas. Si buscas mejorar tu juego con un entrenador profesional, únete Choque escolar para todas tus necesidades de coaching. En Clash School, los profesionales están listos para enseñar y guiarte para que luego seas lo mejor que puedas ser.

https://centroauditivo.com.br/resena-completa-del-juego-balloon-de-smartsoft-para-jugadores-en-guatemala/

Siguiendo con el tema «Esta es Mi Razón», nos asociamos con el cliente de AWS Children’s National Hospital para crear y distribuir pines de edición limitada con obras de arte de pacientes que han sido tratados en su hospital en Washington D.C. Desde el «curita de abejorro» que representa la mentalidad y coordinación de un enjambre de personal hospitalario hasta el pin «pateando el trasero al cáncer» que se explica por sí mismo, estos pines sirven como un recordatorio simbólico de nuestra pasión unificadora por aprovechar la tecnología para mejorar los resultados para los pacientes. Sam is always quick at replies and always figures out any problems or questions I have…..always happening at my user end. Can’t say enough good about response since our old ticketing would take days to get back to us. The app is very user friendly. Takes me a few minutes to find what I am looking for but it is always available to me. So please with everything so far. Stil working with first show with them but LOVE THIS COMPANY!

The Real Person!

The Real Person!

While the thrill of Mission Uncrossable is undeniable, it’s crucial to approach the game responsibly: Engaging with different games on Roobet can provide fresh perspectives and strategies for better performance in Mission Uncrossable. Playing a variety of games can refresh your mindset and contribute to better decision-making, ultimately improving your success in Mission Uncrossable. This approach not only keeps your gaming experience diverse and exciting but also enhances your overall strategic skills. Recently, chicken games and games of skill have become increasingly popular at sweepstakes casinos. This can include chicken-themed slots and crash-style games at top sweeps casinos like Stake.us that are available to play right now. The aim of the game is to get your chicken across the road, and scoop the maximum win of $1 million. Whether you’re new to Mission Uncrossable or you’ve spotted it on social media and you fancy giving it a try, my guide will tell you how you can get started. I’ll also pass on some key strategies and tell you how you can grab the Roobet welcome promotion for 20% cashback on selected slot games.

https://triosismanunggal.com/2025/07/12/what-players-say-after-100-crash-rounds-in-aviator-by-spribe/

Entre essas plataformas de cassino com bônus, a KTO se destaca pela quantidade de promoções, que inclui bônus de rodadas grátis, torneios e cashback. Sim, a Betnacional oferece um app para Android, que permite apostas rápidas pelo celular. Embora o Betnacional Casino apresente vários pontos de destaque, existem fatores em que a empresa ainda precisa melhorar. Diante disso, antes de começar a jogar, vale a pena conhecer as desvantagens da Betnacional, que incluem: Os principais cassinos com rodadas grátis de 2025 são a Novibet, Aposta Online, KTO, Luva.bet e Estrelabet. Isso torna mais fácil decidir estrategicamente qual jogo do cassino online é mais vantajoso para nós. Para obter o app, você precisará baixar o arquivo apk diretamente do site da Betnacional e instalá-lo em seu dispositivo móvel. Após completar essa etapa, basta criar uma conta ou fazer o login para começar a usar o app.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

The Real Person!

The Real Person!

Dzięki wysokiemu RTP i ocenie zmienności, wraz z zabawnym motywem i ekscytującymi bonusami, Sugar Rush to gra, której nie można przegapić. Animacje i grafika na pewno wprowadzą Cię w dobry nastrój, a potencjał na duże wygrane zatrzyma Cię w grze na wiele godzin. Oprócz Punktów zwiększasz swój status (od początkującego do Diamentowego), wraz z powiązanymi limitami i opłatami związanymi z transakcjami na lub z twojego konta w kasynie. Sticky wilds i scatters to najlepsze cechy tego automatu online, takich jak bonusy powitalne dla nowych graczy. Ustawodawcy w Grecji są zajęci przygotowywaniem ustawy hazardowej, sun palace casino no deposit bonus aby wygrać duże. Maksymalna wygrana Sugar Rush slot posiada RTP 96.50% (może być niższe – 95.5% lub 94.5% w zależności od kasyna) i wysoką zmienność. Taka zmienność, choć zapewnia nieco rzadsze wygrane, to jednak ich wartości są zazwyczaj bardzo okazałe.

http://www.icuogc.jp/pukiwiki/index.php?grunorlansu1980

Lood is Good sp. z o. o. ul. Radzikowskiego 35 31-315 Krakow Bhut Panteon to wyjątkowa hybryda Bhut Joloki Chocolate z Sugar Rush. Charakteryzuje się przez to ostrością poziomu klasycznego superhota oraz wyjątkowym kształtem odziedziczonym po Sugar Rush. W samych walorach zapachowych poza klasycznymi nutami Joloki pojawia się słodycz zbliżona do rodziny Bubblegum. Smak słodki, kwiatowy z szybko rozkręcającą się ostrością. +44 1443 809880 Polowe testy orki wykazują, że opony Trelleborg, przy zachowaniu tych samych warunków i rozmiarów, radzą sobie lepiej niż opony konkurencji, zarówno pod względem poślizgu jak i czasu pracy na hektarze pola. Converse shoes have been around a long time. A really long time. We have to shoot back to 1918 for the first Converse All-Star basketball shoes, which came about to stop the legendary Chuck Taylor from complaining of sore feet on the court. Converse ended up giving him a job, Chuck went from full-time court star to their top brand ambassador. Come 1932 Chuck’s signature was added to the side patch on those classic All-Star high tops, where it would (and does) remain.

The Real Person!

The Real Person!

Ahondando en las ventajas y limitaciones de Big Bass Bonanza, delineamos que la tragaperras brilla por su atractiva ronda de bonificación de tiradas gratis y multiplicadores que pueden alcanzar hasta 20x el valor de la apuesta. El excelente índice RTP refuerza el atractivo del juego. El abuelo con una camiseta verde es el scatter que puede activar los giros gratis con tres o más iconos en cualquier lugar de la pantalla, ultimas maquinas tragamonedas gratis la máquina tragamonedas se detiene por sí misma. Si el recurso no contiene información sobre el licenciante, una función de Carretes giratorios y una función de Líneas Conectadas también están ahí para ayudarlo a ganar. COPYRIGHT © 2015 – 2025. Todos los derechos reservados a Pragmatic Play, una sociedad de inversión de Veridian (Gibraltar) Limited. Todos y cada uno de los contenidos incluidos en este sitio web o incorporados por referencia están protegidos por las leyes internacionales de derechos de autor.

https://www.udrpsearch.com/user/reilenbecor1972

Lea nuestra reseña del bono Bovada Sports aquí, un vendedor de Nueva York. Jugar gratis big bass bonanza y uno de estos bonos son los bonos de devolución de dinero, el uso de la Función de Caída y la Opción de Apuesta le dará la mejor oportunidad posible de una gran victoria. El sistema dice además que habrá un equilibrio uniforme entre números altos y bajos, las dos manos se comparan. Functional cookies help perform certain functionalities like sharing the content of the website on social media platforms, collecting feedback, and other third-party features. Jugar a la tragaperras Bigger Bass Bonanza no podría ser más fácil. Selecciona tu apuesta utilizando los iconos de más y menos situados debajo de la cuadrícula de los rodillos y, a continuación, pulsa el botón con dos flechas para girar. También puedes usar la opción “Autoplay” para configurar hasta 1.000 rondas sin manos.

The Real Person!

The Real Person!

pixbet+download+android zytovision products visionarray Główne skrzypce odgrywają tutaj program lojalnościowy oraz turnieje na automatach do gier. Każda osoba, która zdecyduje się zarejestrować w Vulkan Vegas casino, podczas zabawy zbiera punkty lojalnościowe, dzięki którym pnie się w hierarchii graczy. W ten sposób można odblokować nowe, przystępniejsze możliwości zabawy. Turnieje wyłaniają najlepszych użytkowników na wybranych grach, przyznając dodatkowe pieniądze dla osób z pierwszych miejsc. Od momentu wystartowania dokładamy wszelkich starań, żeby zapewniać naszym odbiorcom dokładnie tego, czego oczekują. Podmiot ten dysponuje tylko jednym bonusem powitalnym na zakłady sportowe, jednakże jest on bardzo lukratywny. Wzory swoim uzyskania są fantastycznie proste, trzeba zarejestrować profil na platformie 20Bet, a następnie wpłacić depozyt o cenie minimalnej 80 PLN. Warto zaznaczyć, iż im więcej pieniędzy zainwestujemy, tymże więcej środków bonusowych uzyskamy (maksymalnie pięćset PLN). Każde bonusy kasynowe należy obrócić 40x, aby móc wypłacić środki na własny rachunek bankowy. Niestety tęskni tu uwielbianego za pośrednictwem kasynową społeczność bonusu z brakiem depozytu. Witryna 20Bet wypracował samemu obecną pozycję, głównie dzięki swojej niesamowitej palecie przeznaczonej gwoli świeżych zawodników.

https://cn.mnchip.com/uncategorized/11839

Kosaciec Sugar Rush przyciąga spojrzenia swoim unikalnym wyglądem, a dodatkowo jest łatwy w pielęgnacji. Najważniejsze jednak, co należy zapamiętać z powyższych informacji to fakt, że w płytkach tonalnych nie należy doszukiwać się wzorów, który możliwy jest do ułożenia z jednego czy też nawet kilku opakowań. Tonalność to zabieg celowy nadany przez producenta. W jednym opakowaniu płytki tonalnej każda z płytek może różnić się od siebie. Przeczytaj na Naszym Blogu obszerny wpis o płytkach tonalnych Hity promocyjne Bezbarwny akrylowy proszek multifunkcyjny to prawdziwy must-have w Twojej kosmetyczce! Idealny do tworzenia lekkich, naturalnych stylizacji albo jako baza pod bardziej szalone projekty. Warto go mieć zawsze pod ręką – zamów i ciesz się perfekcyjnym manicure!

The Real Person!

The Real Person!

Let’s talk symbols and a bit of the theme you will be set in. when playing Big Bass Bonanza you are set on a lake fishing for the big game of the ocean, the bigger the fish the higher the prize, and your play reel background is set under the sea, with a nice natural feel with it, plus a nice little jaunty soundtrack. Bigger Bass Bonanza, developed by Pragmatic Play, is the upgraded and more premium version of the classic slot game Big Bass Bonanza. With higher betting options, it’s designed to cater to high rollers looking for big prizes and a more engaging fishing-themed experience in online casinos. Here at OLBG we write slot game reviews and score them out of 5 so, whenever a Big Bass game is reviewed it will be added to the table below. The highest so far is Bigger Bass Bonanza at 4.5 5 and the lowest so is Big Bass Halloween at 2.6 5.

https://bakkieengines.co.za/play-with-purpose-this-ludo-app-pays-out-in-real-cash/

Merry Christmas from Big Bass slots as we get the first Christmas version of the original Big Bass Bonanza game in Christmas Big Bass Bonanza. Offering the same RTP rate, max win potential and bonus features as the first game in the Big Bass slots series, it has a wintry snowy twist which is perfect for the festive period. Pragmatic Play didn’t manage to take our breath away with amazing HD graphics or animations in this game, but it does have a happy theme with a catchy soundtrack. Big Bass Bonanza is a fun game overall, and the cash-drops make it exciting as you wait for the wild to fall and scoop them all up in one go. Loaded with multipliers, a shy wild and retriggers on the free spins round, this slot can load up a rather impressive catch. Big Bass Bonanza’s relaxing fishing experience is the main selling point here. This game proves that software developers don’t need to overcomplicate games with unnecessary features to release big hits. It’s time to dip your fishing rod into the calm waters and see what it catches. If you enjoy this game, be sure to check out Big Bass Christmas Bash.

The Real Person!

The Real Person!

All of the available Megaways titles at MrQ are fully compatible on all mobile devices. Sign up today and play with real money on our mobile slots and casino games including the top Megaways titles. This slot uses the Megaways system, which randomises the number of symbols on the reels for each spin. Buffalo King Megaways is an online slot game that takes you on an exhilarating journey into the wilderness of the American frontier. This game is a product of Pragmatic Play, a renowned software provider in the online gambling industry, and is an excellent example of their attention to detail and player-first excellence. A few states in the US offer legally-licensed, safe real-money online casinos for slots players. These include Michigan, New Jersey, Pennsylvania, and West Virginia. Players outside of those states can play slots with premium coins at sweepstakes casinos and social casinos, then redeem those premium coins for cash prizes.

https://bisd.rs/exploring-space-xy-by-bgaming-a-stellar-casino-game-review-for-indian-players/

For players seeking instant access to the thrilling free spins feature, Buffalo King Megaways offers a feature buy option. By paying 100 times the total bet, players can bypass the base game and dive straight into the bonus round. This option caters to those who prefer a more direct and immediate gameplay experience. Just kick it back and stick to your usual gaming strategy, we have no free play mode for Fairie Nights available. Even today many countries abide by the same laws, thats the underlying story behind the creation of this game. Look out for the symbols A, Samsung. You will have access to a vast variety of online gaming games and some tons of them, Xiaomi. The Buffalo King Megaways slot machine features icons that represent the wide variety of North American flora and fauna. Players will come across moose, wolves, cougars, eagles, and the great buffalo in addition to the traditional card images from 10 to A. Aligning a combination of buffalos can provide players with up to 20 times their stake, and the symbols’ elaborate designs pay homage to the region’s spectacular creatures. There is also a wild symbol that can be used in place of any other symbol to complete winning combos.

The Real Person!

The Real Person!

2. **Juegos de casino de clase mundial**. Disfruta de los mejores juegos de casino en línea, desde tragamonedas hasta ruleta y póker. Nuestro casino cuenta con gráficos de alta calidad y un entorno interactivo para brindarte la mejor experiencia de juego. Comentario * Erik King es un analista de iGaming con amplia experiencia y editor principal en Toroslots, donde aporta más de una década de experiencia directa en la industria de los casinos online. Conocido por su atención al detalle y su enfoque centrado en el jugador, Erik ha revisado cientos de sitios de casino, probado miles de juegos y verificado personalmente las condiciones de los bonos para garantizar transparencia y equidad. Sigma Europe Awards, Best New Casino Game: Tower Rush Inicia sesión para agregar este artículo a tu lista de deseados, seguirlo o marcarlo como ignorado.

https://gad-quiroga.gob.ec/review-detallado-de-sugar-rush-el-juego-de-casino-en-linea-de-pragmatic-play-en-espana/

Aunque el diseño y la temática de Sugar Rush 1000 son los mismos que los de su predecesora, esta nueva versión presenta mejores gráficos. La tragaperras está ambientada en un reino de dulces con árboles de piruletas, ríos de chocolate y montañas de nubes. En este encantador diseño, abunda el color y la alegría. Sin embargo, los juegos de casino demo pueden tener una configuración matemática algo distinta a los que encontrarás en algunos casinos online. Esto se debe a que algunos proveedores de juegos permiten que los casinos elijan entre distintas versiones de la misma tragamonedas con una RTP diferente, por lo que, si tu casino se ha decantado por una variante menos generosa, los pagos y probabilidades pueden ser distintos. COPYRIGHT © 2015 – 2025. Todos los derechos reservados a Pragmatic Play, una sociedad de inversión de Veridian (Gibraltar) Limited. Todos y cada uno de los contenidos incluidos en este sitio web o incorporados por referencia están protegidos por las leyes internacionales de derechos de autor.

The Real Person!

The Real Person!

1xBet promo code fluentcpp news kakochistitykishech.html is an opportunity to get a bonus of up to 100% on your first deposit. Register, enter the code and start betting with additional funds. Fast, simple and profitable. 20BetBonus 100% od depozytu aż do 700 R$ jogar aviator online: estrela bet aviator – pin up aviator mostbet apk mostbet apk . 20BetBonus 100% od depozytu aż do 700 R$ Szanse na wygraną w Aviatorze Betano są spójne przez cały dzień. ContentThe Debate Over Mostbet CasinoUp In Arms About Mostbet Casino?Replacing Your Mostbet … mostbet uzcard скачать mostbet uzcard скачать . 188bet 88bet: keo nha cai 88bet – 88bet การลงทะเบียนและเข้าสู่ระบบที่ 12bet เป็นขั้นตอนที่ง่ายและรวดเร็ว ผู้เล่นสามารถเริ่มต้นได้ทันที พร้อมทั้งรับโบนัสพิเศษเพื่อเพิ่มโอกาสในการชนะในเกมต่างๆ ที่ 12bet มีให้บริการ

https://silverbackgaming.com/2025/08/vulkan-vegas-ekskluzywne-oferty-dla-graczy-high-roller-w-polsce/