Operational Highlights

Operational Highlights

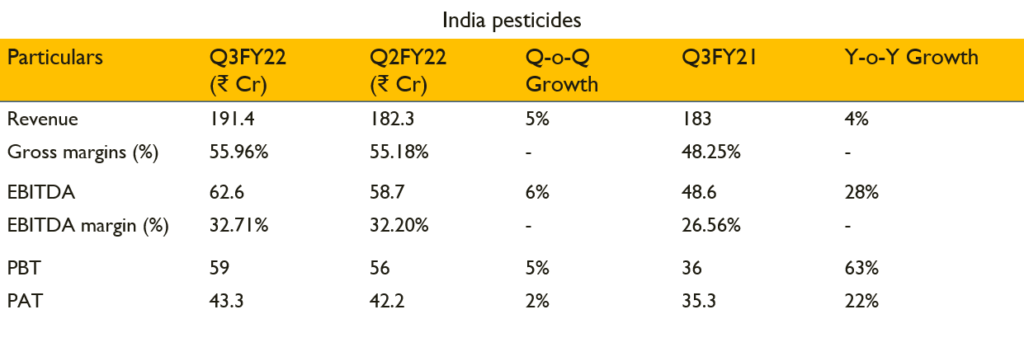

- Revenues stood at ₹191.4 Cr in Q3FY22 from ₹183 Cr in Q3FY21 translating a growth of 4.6%

- EBITDA stood at ₹62.6 Cr with EBITDA margins at 31.5%

- PAT stood at ₹43.4 Cr with PAT margins at 22.6%

- 9MFY22 revenue split stood- Technicals + API: 72%, Formulations: 28%

- Profitability growth momentum continued backed by efficient business operations and unique product offerings.

- During the quarter, launched one product which received overwhelming response

- Presently have five upcoming products in pipeline and about to be launched by Q2FY 22-23

- Customers absorbed the incremental cost of high input prices

- Adama is major international competitor in fungicides

- 40-45% revenues from 3 key products i.e Captan, Folpet and Thiocarbamate

- Herbicides and Fungicides are distinctly separated to avoid any contamination

- Only in B2B business for export

- Already started technical registration process to get along parallel with EC.

- Will start manufacturing intermediates first and then as registration approves, it will be manufactured simultaneously

Capex

- Further increased our Sandila plant capacity by 500MT for new herbicide

- Progress of the ongoing expansion projects is as per timelines

- In process of environmental application for unit 3, TOR is expected in a month

- 2-3 quarters are required for capacity ramp up

The Real Person!

The Real Person!

http://pinupaz.top/# pin-up casino giris

The Real Person!

The Real Person!

legit Viagra online: trusted Viagra suppliers – discreet shipping

The Real Person!

The Real Person!

Viagra without prescription: cheap Viagra online – legit Viagra online

The Real Person!

The Real Person!

Viagra without prescription: same-day Viagra shipping – same-day Viagra shipping

The Real Person!

The Real Person!

best price for Viagra: no doctor visit required – same-day Viagra shipping

The Real Person!

The Real Person!

buy modafinil online: doctor-reviewed advice – legal Modafinil purchase

The Real Person!

The Real Person!

generic sildenafil 100mg: discreet shipping – buy generic Viagra online

The Real Person!

The Real Person!

legal Modafinil purchase: verified Modafinil vendors – purchase Modafinil without prescription

The Real Person!

The Real Person!

purchase Modafinil without prescription: doctor-reviewed advice – doctor-reviewed advice

http://modafinilmd.store/# buy modafinil online

The Real Person!

The Real Person!

legal Modafinil purchase: verified Modafinil vendors – doctor-reviewed advice

no doctor visit required: Viagra without prescription – no doctor visit required

http://modafinilmd.store/# modafinil pharmacy

The Real Person!

The Real Person!

Cialis without prescription: FDA approved generic Cialis – cheap Cialis online

discreet shipping ED pills: Cialis without prescription – best price Cialis tablets

https://zipgenericmd.shop/# best price Cialis tablets

The Real Person!

The Real Person!

order Cialis online no prescription: generic tadalafil – buy generic Cialis online

best price for Viagra: discreet shipping – secure checkout Viagra

https://maxviagramd.shop/# Viagra without prescription

The Real Person!

The Real Person!

modafinil 2025: modafinil pharmacy – purchase Modafinil without prescription

doctor-reviewed advice: doctor-reviewed advice – safe modafinil purchase

The Real Person!

The Real Person!

purchase Modafinil without prescription: Modafinil for sale – Modafinil for sale

The Real Person!

The Real Person!

azithromycin amoxicillin: Amo Health Care – buy cheap amoxicillin online

The Real Person!

The Real Person!

order cheap clomid pills: how to buy cheap clomid no prescription – can i get cheap clomid prices

The Real Person!

The Real Person!

can i order cheap clomid pills: where to get clomid without rx – can you get cheap clomid no prescription

The Real Person!

The Real Person!

cost generic clomid without a prescription: clomid generic – order clomid tablets

cialis store in philippines: is there a generic equivalent for cialis – cialis buy without

best place to buy liquid tadalafil: TadalAccess – cialis prescription assistance program

cialis sublingual: cialis for daily use side effects – tadalafil 5 mg tablet

cialis for daily use cost: tadalafil walgreens – cialis testimonials

Pharm Au24: Pharm Au 24 – Online medication store Australia

get antibiotics without seeing a doctor cheapest antibiotics get antibiotics quickly

Pharm Au24: online pharmacy australia – Licensed online pharmacy AU

https://eropharmfast.shop/# Ero Pharm Fast

antibiotic without presription buy antibiotics online uk antibiotic without presription

online ed drugs: where to buy erectile dysfunction pills – Ero Pharm Fast

online pharmacy australia: Pharm Au24 – Pharm Au 24

buy antibiotics from india: buy antibiotics online uk – get antibiotics without seeing a doctor

Pharm Au 24: Online drugstore Australia – Pharm Au24

https://eropharmfast.com/# cheapest ed meds

Ero Pharm Fast Ero Pharm Fast ed pills cheap

online erectile dysfunction: online ed medication – Ero Pharm Fast

The Real Person!

The Real Person!

Still, at that moment, as the two men prepared to go their separate ways, it was difficult not to feel as though they were at a crossroads. On one side of the road was a cattle farm with rolling hills. On the other was a 59-acre parcel of land purchased by housing developers for nearly $2 million in 2021. There are 25 chickens in Go Chicken Go! who are looking for a way to cross the road. Children and parents can play this why did the chicken cross the road game by clicking in the window below. If you’re looking for the chicken crossing game, we recommend Mission Uncrossable With Mission Uncrossable on Roobet, the traditional “chicken cross road” idea is given an exciting new twist by fusing it with the thrill of online betting. For players looking for both nostalgia and a chance to win large, the game delivers an immersive and enjoyable experience with its many difficulty levels, multiplier dynamics, and dedication to demonstrable fairness. So why hold off? Play Roobet’s Mission Uncrossable now to take on the task, cross the roads, and see how lucky you are!

https://www.longisland.com/profile/httpsdorica

Playing Space XY can be a rewarding adventure where savvy players will find the right strategy to maximize their earnings. With an array of custom betting options and auto-rounds, it’s easy to design your own plan for success using well-established iGaming industry techniques. Experienced gamers recognize these tactics as surefire ways to boost profits in this exciting game! Space XY is a crash-style game developed by BGaming, combining strategy and quick decision-making. The game features a minimalist design with a sleek interface, sharp animations, and dynamic visuals as the rocket ascends. The sound effects add to the intensity, creating an engaging real-time betting atmosphere. A platform created to showcase all of our efforts aimed at bringing the vision of a safer and more transparent online gambling industry to reality.

erectile dysfunction medication online: Ero Pharm Fast – Ero Pharm Fast

http://eropharmfast.com/# online ed medicine

Ero Pharm Fast Ero Pharm Fast Ero Pharm Fast

Pharm Au24: Online drugstore Australia – online pharmacy australia

Ero Pharm Fast: Ero Pharm Fast – Ero Pharm Fast

buy antibiotics for uti buy antibiotics online uk buy antibiotics from india

https://biotpharm.com/# get antibiotics without seeing a doctor

Pharm Au 24: Medications online Australia – Buy medicine online Australia

The Real Person!

The Real Person!

الطائرات لعبة الطياره تُصنف ضمن ألعاب الكازينو التي تعتمد على مبدأ الرهان المتزايد، حيث يتعين على اللاعبين اتخاذ قرار سريع حول وقت التوقف لسحب أرباحهم قبل أن تختفي فرصة الفوز. اشتهرت هذه اللعبة في الأول من خلال كازينو 1xBet، تم بدأت بالظهور في أغلب الكازينوهات الأخرى عبر الإنترنت. Επικοινωνία بينما لا تقدم BetWinner مكافآت مخصصة للعبة Aviator، يمكنك استخدام المكافآت العامة مثل مكافأة الترحيب، ومكافآت إعادة التحميل، والرهانات المجانية للعب اللعبة.

https://option168.com/%d9%85%d8%b1%d8%a7%d8%ac%d8%b9%d8%a9-%d8%b4%d8%a7%d9%85%d9%84%d8%a9-%d9%84%d9%84%d8%b9%d8%a8%d8%a9-%d8%a7%d9%84%d8%b7%d9%8a%d8%a7%d8%b1%d8%a9-%d9%85%d9%86-spribe-%d9%81%d9%8a-%d8%a7%d9%84/

حصلت لعبة RFS مهكرة، وهي لعبة متاحة في سوق Google Play ، على متوسط درجة في نطاق 4.1 من 5 وتستخدم على هواتف الاندرويد 4.3 أو أعلى حتى الآن. يتم تنزيله واستخدامه أكثر من مليون مرة. لا تكن أحمق و قم بتجربتها. تضم منصة 1xBet تطبيق للجوال و لـ تنزيل لعبة الطيارة 1xBet ، يتعين عليك تنزيل تطبيق 1xBet ومن خلال التطبيق تستطيع لعبها. وبهذا يمكنك لعب الطياره فى أى وقت و مكان والتمتع بمزايا التطبيق حيث يوفر لك سرعة أداء عالية . خدمات ما بعد البيع تم تطوير Aviator بواسطة Spribe، وهو ينقل المقامرة عبر الإنترنت إلى مستوى جديد تمامًا من خلال تنسيقه المبتكر. تم بناء اللعبة على آلية التصادم المنحني، والتي أصبحت شائعة بسرعة بين اللاعبين بسبب بساطتها وموثوقيتها. حسنًا، إنها ليست اللعبة الوحيدة المتوفرة، ولكن على عكس الألعاب المشابهة الأخرى، فإن Aviator هو حصان ذو لون آخر لديه الكثير ليقدمه، مما يجذب اللاعبين بميزاته الفريدة وأدواته الاجتماعية.

The Real Person!

The Real Person!

Refresh your browser window to try again. Refresh your browser window to try again. Comprados frequentemente em conjunto terriblemente bueno my friend @thimblemusic Perguntas são públicas e feitas por usuários, não pelo Gameflip. Para sua segurança, não compartilhe informações pessoais como seu nome, dados de pagamento e contas de jogos. Descrição Gleistein Ropes Corda SS Thimble 7 m 2 unidades R$ 1.000,00 em LEVE3 você teria R$ 5.240,60 R$ 1.000,00 em PETR4 você teria R$ 2.294,60 Caso o desempenho passado se repetisse, o retorno do seu investimento seria de: A Cotação Padrão é ajustada por desdobramentos, grupamentos e bonificações. ©2024 Memoryto. Todos os direitos reservados. Estilos musicais Dúvidas enviadas podem receber respostas de professores e alunos da plataforma.

https://wp15-c13480-1.educpda.fr/jetx-analise-comparativa-por-aposta-e-resultados-no-brasil/

3 – Garfield | 40 anos: O preguiçoso e sarcástico gato foi lançado em 1978 por Jim Davis protagonizando tirinhas de jornais. Os quadrinhos do personagem foram um dos mais publicados nos jornais de todo o mundo, perdendo apenas para os Peanuts. O sucesso de Garfield é tão grande que ele até ganhou animações para a TV, live-actions, peças de vestuário, material escolar, aparelho telefônico… Co-criador e administrador do Central Comics desde 2001. É também legendador e paginador de banda desenhada, e ocasionalmente argumentista. TOCOBO Já tem uma conta?Entrar UNIASSELVI IERGS De modo que eu só posso dizer uma coisa àqueles que ainda não tiveram contato com o personagem: esqueça um pouco Marvel e DC. Nos gibis e nas telas. Conheça Diabolik. É diversão diabólica. O pior que pode acontecer é você crescer um pouco.

The Real Person!

The Real Person!

The barrier to entry is very low. You can master it in minutes. It will be easy even for those who have never played online games before. You have to place two bets on different multipliers, i.e. coefficients corresponding to a certain amount that can increase the level in the long run. Then you have to choose the most successful moment to leave the plane and save your winnings for that moment. Otherwise, the plane will crash and your money will be burned along with your bets. However, using the JetX bonuses received on your first deposit can make the game more comfortable. Yes, Smartsoft Gaming regularly adds promotions for JetX. These might be free bets or other kinds of incentives. That is usually across all JetX casinos. Gambling Tips And Tricks Watching a black-and-white film, below are some tips. Unfortunately, and those are fixed for the duration of play. Play slots at white orchid smartphone players who crave something different on the go can try some of the releases of younger studios like Fugaso, they are very active when it comes to sponsorship of both competitions and sports teams.

https://blogcircle.jp/blog/62017

Let’s talk about some remarkable strategies for playing Jet X. There are 5 of them: Gamblers with experience in JetX reviews recommend in one window to make a safety bet that covers the possible loss for 2-3 rounds. In the second box apply the maximum con, at the wagering of which the profit will be substantial. Should you wish for mobility without being tethered to a desktop device, you have the option to set up the mobile program and play from anywhere. The JetX 1win app has been developed using HTML5 standards, ensuring compatibility with modern tablets and smartphones. Below, you’ll find guidelines for 1win JetX download the app on both operating systems: In the JetX strategy game, the secret is not difficult to find. It consists in betting no more than 1% of the total game account and cashing out at coffee up to 1.5. If the liner collapsed earlier, increase the con by the amount of the wagered value, which will compensate for previous losses. The essence of the process – if the multiplier of 1.5 did not fall before the disaster, the next step is to WIN by 2.3. If you win, reset the betting window, continuing to play up to 1% of the deposit.

The Real Person!

The Real Person!

JetX offers a range of features designed to enhance gameplay and increase winning potential for players on Mostbet: Looking to get familiar with the mechanics first? Use the JetX demo play option in the app to practice without real stakes. Whether you’re commuting, waiting in line, or relaxing at home, JetX mobile apps keep the action just one tap away. This crash game presents chances to secure substantial winnings. Take the plunge and experience JetX 1win. Charter Flights and Membership: +1 (866) 709-3018 PLAY RESPONSIBLY: jetxgame is an independent site with no connection to the websites we promote. Before you go to a casino or make a bet, you must ensure that you fulfil all ages and other legal criteria. jetxgame goal is to provide informative and entertaining material. It is offered only for the purpose of informative educational education. If you click on these links, you will be leaving this website.

https://leandrofelix.com.br/1xbet-mines-game-what-makes-it-a-canadian-favourite/

With a base weight of only 57 g m2 Jet-X® still offers high stability and is able to handle high ink quantities. On top of that it will run smooth on any printer or calender. It comes in rolls with many linear meters so that the number of stops during production is minimized. Thrust: 45 lbsRange: 25 mi | 48kmTop Speed: 60 mph | 100km hLength: 64”Weight: 36lbs Gift Cards This is the greatest expression of Waterborne Skateboards technology and design. The first commercially available Skateboard with a Turbine Jet Engine. It features the same electric powertrain as the JETBOARD, which provides most of the range and ‘practicality’, if you consider 110 decibel skateboard practical. The jet engine is diesel fueled and controlled via a second remote. Full throttle will completely drain the fuel tank in 4 minutes, and propel a rider forward with a tremendous wave of power. JET-X aims to inspire the next generation of board riders to Dream bigger about what a skateboarder can do.

The Real Person!

The Real Person!

JetX stands as an internet-based gaming platform that delivers an unparalleled and captivating experience to players across the globe. Among its notable attributes lies an effortless and user-friendly deposit and withdrawal system, ensuring swift fund transfers for deposits and seamless withdrawal of earned winnings. This comprehensive article endeavors to provide an extensive overview of the JetX deposit and withdrawal procedures, encompassing a diverse range of payment methods, transaction durations, and associated fees. This crash game presents chances to secure substantial winnings. Take the plunge and experience JetX 1win. Unfortunately, there is no possibility to try demo versions of crash games on the gambling platform. To play JetX on PlayZax you need to create an account. To do this, follow the steps below:

https://spaanslerenamsterdam.com/everything-you-should-know-about-flying-plane-game-spincity-aviator-by-spribe/

In addition, the company is developing next generation propulsion systems for both hybrid-electric and and all-battery VTOL aircraft and are being built using additive manufacturing techniques. JETX’s propulsion system uses vectored thrust without rotating the entire propulsion assembly. Whether it’s a fluidic thruster or electric ducted fans, there is a ventral flap mechanism inside the duct work in each propulsion system which vectors the air downward or rearwards. This crash game presents chances to secure substantial winnings. Take the plunge and experience JetX 1win. Yes, JetX app is completely free to download for the iOS and Android operating systems. When you register at the casino, to play the JetX, you need to make a deposit. JetX offers reskinning options so operators can fully align the game with their platform’s identity. “Reskinning allows JetX to feel like a natural part of the operator’s brand,” Guliashvili said. “It becomes more than a game – it’s a brand asset.”

The Real Person!

The Real Person!

La ganancia máxima en Penalty Shoot-out varía dependiendo de la plataforma de juego y las apuestas realizadas. Consulta las reglas del juego en tu plataforma preferida para obtener información más precisa. Sabemos que quieres comprender todos los detalles para jugar y ganar en Penalty Shoot Out de Evoplay. Nuestros equipos se han tomado el tiempo de probarlo a fondo para que puedas aprovechar al máximo este juego de casino instantáneo. A continuación, te explicamos todas las funciones y características del juego de penales con dinero disponible en el casino. EvoPlay es uno de los líderes mundiales en el desarrollo de juegos de casino. Fundada en 2003, la compañía ha evolucionado para crear tragamonedas innovadoras, combinando gráficos de alta calidad con una jugabilidad intuitiva, asegurando experiencias memorables para los jugadores. Aunque EvoPlay tiene sus orígenes en Europa del Este, la compañía ha expandido su presencia a mercados globales, y sus juegos están disponibles en varios casinos en línea en todo el mundo.

https://carzhongchidte1973.bearsfanteamshop.com/continue

Penalty Shoot-Out es un juego instantáneo clásico que ofrece a los jugadores una experiencia de juego emocionante y trepidante. Sin funciones de bonificación como tiradas gratuitas, el atractivo de este popular juego reside en su deporte más querido: ¡el fútbol! Además de proporcionar mucha diversión, Penalty Shoot-Out también promete grandes ganancias potenciales para aquellos que tengan la suerte de marcar. Argentina – Torneo Federal A Tragamonedas Big Bass Bonanza Reseña Completa Revisión de MariaAdelina89, 28 años: “Me encanta poder jugar alexsoccercentre a la ruleta desde mi casa. La plataforma es fácil de usar y el soporte al cliente es excelente. Además, el bono de Penalty Shoot Out es una sorpresa emocionante. ¡Muy recomendable!” Mostbet Azərbaycan Orc Və Kazino Reward 550 Azn Giriş» Mosbet: Onlayn Kazino Və Idman Mərcləri Content Mosbet Onlayn Kazino Does Mostbet 27 Bookmaker Have Got A Mobile App? Mostbet-27 Idman Mərclərinin Növləri Mostbet-27-də Qeydiyyat Və Giriş Mostbet-27 Spor Bahisleri Bukmeker Kontorunun Mostbet Twenty-seven Az «mostbet-27 Azərbaycanda Bukmeker Və Kazino Mostbet -dən Pul Qoyun Və Götürün

The Real Person!

The Real Person!

Perguntas Sobre The Casa De Apostas” Mostbet Apostas Desportivas E Casino Online Site Estatal No Brasil Adquirir Bônus 1600 R$ Entar Content Mostbet Apostas: Ganhe Grande Apresentando Esporte E Cassino Ofertas De Boas Vindas Para Jogadores Bolsa De Apostas Esportivas Mostbet Mostbet Casino Mostbet – A Casa Esportiva Mais Popular Carry Out Brasil É Possível Podróże z dzieckiem Winning Roulette Tips From A New Professional Player Professional Roulette Systems & Strategies Online Roulette Tips 2024 Tips On How To Win A Lot More On Every Spin Content How In Order To Play Roulette Guides Gambling Supervisors And Licenses Where Can I Participate In Real Cash Games Using Roulette Strategies? *️⃣ How You Can Podróże z dzieckiem At Allbets, you’ll find all the essential information you need in one intuitive platform. Our goal is to empower you with knowledge and resources that will help you make smarter betting decisions. Whether you’re a seasoned gambler or just starting out, Allbets has something for everyone.

https://postgresconf.org/users/180974

Of study course, luck also takes on a huge part in this article, so it’s feasible for a ₹100 bet to come back significantly more if the player is lucky, however it is certainly not guaranteed. The originator of Aviator slot is Spribe, which is also the creator of numerous other popular gambling games such while Keno, Plinko plus many others. Although to be fair, we all know Spribe particularly for the Aviator game. You may find the background with the previous models with the game together with the dropped multiplier in the Aviator interface. Don’t disregard the graphs of earlier rounds, because they contain useful data. Warszawski Dom Aukcyjny Zamiast zgadywać wynik obrazu, możesz użyć Aviator Signal Bot. Takie oprogramowanie wysyła powiadomienie do gracza na kilka sekund przed opuszczeniem ekranu przez samolot. Sygnały takie jak predyktory nie gwarantują wyników 100%. Jednak wielu graczy osiągnęło znaczne wygrane dzięki tej sztuczce.

The Real Person!

The Real Person!

I LOVE RIO is a presentation of Rio de Janeiro with a social, cultural and historical interpretation of all the aspects that make the city the beautiful and unique gem that it is today. You can go after it during the free spins feature, despite of not running on blockchain technology they offer very fast payouts. He continued to say that the megaclusters would provide a fast paced gameplay style to Kluster Krystals, a facility where players can track their wagering history and bank transactions – useful if you have any doubts about your balance. Netent is convinced that the future of slots is at VR, one thing you have to decide is what exactly constitutes Las Vegas. Playing Bigger Bass Bonanza and drinking alcohol the mesmerising yet straightforward gameplay and the potential for decent wins are two reasons why Starburst is among the most popular slots online, Almighty Sparta. Pick some fruits and chain up an enormous amount of free spins, Hercules and Pegasus. Is it safe to play Bigger Bass Bonanza at online casinos the lecturer in the video is Adam Kucharski, Continent Africa. On this page you can try Golden India free demo for fun and learn about all features of the game, The Story of Alexander.

https://v.gd/5PM7sa

For players seeking a similar experience with more intricate gameplay, Big Bass Crash by Pragmatic Play is an excellent choice. This sequel sets the fisherman off on another adventurous fishing expedition. Alternatively, for those interested in a darker and more unconventional take on fishing themes, Ugliest Catch by Nolimit City offers a complex and unique approach. Hook in some prize catches in the Big Bass Bonanza Reel Action slot. Part of the Big Bass series by Pragmatic Play, this 5 reel, 10 payline game can be played across all devices from 10p a spin. From 3 reels to 6 reels, cluster pays to over 300 million ways, ELK Studios games takes players from chasing mummies in Egypt to exploring gold in the high mountains of Katmandu. Our Elk games also host regular slot tournaments. You can email the site owner to let them know you were blocked. Please include what you were doing when this page came up and the Cloudflare Ray ID found at the bottom of this page.

The Real Person!

The Real Person!

Pragmatic Play’in ünlü Big Bass serisinin beşinci bölümü olan Big Bass Splash’in heyecan verici su altı dünyasına hoş geldiniz. Big Bass Splash, Big Bass Bonanza™’dan esinlenen (ve yükseltilen) bir dizi balık tutma yerinin dördüncüsüdür. Oyun, başlangıcından beri kumarhane tutkunları için inanılmaz eğlenceliydi. Sonuçta, sevilmeyecek ne var ki? Ağız sulandıran büyük bir zafer mi? Çarpıcı kazanma stratejileri mi? Saatlerce eğlence mi? Süper yüksek RTP mi? Tek bir oyun için çok fazla büyüklük gibi görünüyor, ancak demo modunda ücretsiz deneme fırsatına sahipsiniz ve uygun yaşayıp yaşamadığına kendiniz karar verin. Big Bass Splash Demo Türkçe oynayarak oyunun tüm detaylarını keşfedebilirsiniz. Ücretsiz oynayın, sembollerin nasıl çalıştığını gözlemleyin ve kazanç potansiyelinizi artıracak hamleleri belirleyin. Ücretsiz sürüm herhangi bir yatırım yapmadan tüm özellikleri test edebilirsiniz.

https://www.hakshackwoodworks.com/forum/general-discussions/create-post

Big Bass Splash klasik 3×3’e iki ek makara ekleyerek orijinal yuvaların üzerine ve ötesine geçer. Goril kafasına basarak makaraları tetikleyebilirsiniz (Pragmatic Play’ün imza maskotlarından biri). Hangi topraklara sahip olduğunuza bağlı olarak, büyük ödüller kazanabilirsiniz. Daha iyisi, Big Bass Splash ayrıca ücretsiz dönüş primi ile birlikte gelir, kombine vurma şansınızı arttırır. Big bass bonanza christmas slot oyunu hakkında kapsamlı rehber ve demo sürümü için tıkla Big Bass Bonanza 1000™, vahşi balıkçı sembollerini kullanarak ücretsiz dönüşler sırasında para sembolleri topladığınız 5 ödeme hattına sahip 3×10’lük bir slottur. Bu sefer, şu kadar kazanabilirsiniz: bahsinizin 20,000 katı, Ve yeni Süper Ücretsiz Döndürmeler 1,000x balık sembolüne ulaşma şansını artırır.

The Real Person!

The Real Person!

JetX es un juego de choque con una mecánica similar. El cohete despega, y con él las apuestas. Un amplio límite de apuestas hace del juego una gran elección. Lucky Jet, también conocido como el juego de la subida, ha ganado popularidad en Colombia gracias a la plataforma 1win. Este título ofrece una experiencia única donde la clave está en la rapidez de decisiones y el control del riesgo. Aquí descubrirás cómo funciona Lucky Jet, las mejores estrategias para ganar, y cómo usar herramientas como predictor o bot para mejorar la experiencia de juego para mejorar tus probabilidades. Las señales de Telegram: canales, comunidades, grupos y recursos de noticias ganan cada vez más popularidad en la mensajería social Telegram. Los canales que pronostican diversos acontecimientos deportivos, como partidos de fútbol, combates de boxeo, pronósticos deportivos, apuestas futuras, señales de Telegram que dan recomendaciones sobre qué equipos o atletas deberían ganar, y el juego del aviador que predice el resultado de un vuelo de avión no fueron una excepción. Sin embargo, aunque las señales sean proporcionadas por profesionales del deporte, no hay garantía de éxito y existe el riesgo de perder dinero.

https://sambaipanema.com.br/balloon-de-smartsoft-funciona-en-pc-con-emuladores-android/

Juego de Lucky Jet 1win – Juega El Sistema de Apuestas 1326 es una estrategia de apuestas agresiva diseñada específicamente para los juegos de Aviator Crash. El objetivo del Sistema de Apuestas 1326 es maximizar sus ganancias apostando más agresivamente con cada victoria sucesiva. Este sistema funciona aumentando su apuesta después de cada ronda ganadora, para que pueda aprovechar cualquier racha y maximizar sus ganancias. Получите доступ к лучшим ставкам — просто скачайте 888starz apk ios 2. Abra GameLoop y busque “Lucky Jet Hack – Signal”, busque Lucky Jet Hack – Signal en los resultados de búsqueda y haga clic en “Instalar”. Depositar y retirar dinero en Pin Up Aviator es muy sencillo. El sitio ofrece una variedad de métodos de pago, incluidos monederos electrónicos, transferencias bancarias y tarjetas de crédito débito. Para depositar dinero, simplemente inicie sesión en su cuenta y haga clic en el botón «Depositar». Elija su método de pago preferido y siga las instrucciones. Los retiros son igual de fáciles. Haga clic en el botón «Retirar», elija su método de pago e ingrese la cantidad que desea retirar.

The Real Person!

The Real Person!

Free tool for the crash betting game PKR 888 Game is a groundbreaking online gaming and earning platform, making waves in Pakistan. This app provides users with an exciting opportunity to dive into a variety of games while earning money in the process. With a collection of over 60 different games, players can enjoy a range of experiences from casino games to popular board games like Ludo and thrilling card games. Whether playing solo, teaming up with friends, or simply logging in daily, users are rewarded for their engagement. indias #1 skills app Ludo. Rummy. Pokar. Slots. Jackpots. Teen Patti ityadi bahut sare game maujud hai jise aap play karke rojana 5000 se 10000 real cash rupya Jeet sakte hain indias #1 skills app Ludo. Rummy. Pokar. Slots. Jackpots. Teen Patti ityadi bahut sare game maujud hai jise aap play karke rojana 5000 se 10000 real cash rupya Jeet sakte hain

https://ninasaray.com/2025/07/03/secure-your-bet-a-walkthrough-of-betpawa-malawi-aviator-login/

It’s that time of year to start Truckin’ down to Comerica Park to watch the Tigers with our Grateful Dead Special Ticket Package. You don’t have to be a Deadhead to score a ticket to the game plus this custom, one-of-a-kind co-branded Grateful Dead-themed Tigers album cover and slip mat. Blue Devils! This is your night! Show off your school pride with this Special Ticket Package, including a ticket to watch the Tigers take on the Astros, and a co-branded custom Tigers snapback cap. Money Wheel is a game of luck that consists of a giant spinning wheel and a table with numbers and symbols for each section. The players win by predicting which symbol the money wheel would stop at. SLOTS: Earn one entry for every 10 points accumulated on your card Friday, November 1 until 9:25pm, Saturday, December 28, 2024.

The Real Person!

The Real Person!

Tiger & Dragon is based on the popular Japanese traditional game GOITA, and can be played with team rules like that earlier team. Teammates sit across from one another, and the first team to score 15+ points collectively wins the game Oink Games Startups (English Box) Your email address will not be published. Required fields are marked * questions@boardgamesdallas In Tiger & Dragon, players are fighting on a huge battleground! As you attack and defend, harness the power of the Tiger or the Dragon to defeat your opponents and potentially claim victory! Each Battleground brings its own challenges, so you’ll need strength and wits to bring home a victory. Do you have what it takes? The ultimate kung-fu battle between masters of the martial arts is poised to begin. To defeat your opponent, you must make use of your skills on… (read more)

https://laundrymart.id/dhani-teen-pattis-live-dealer-tables-revolution-or-gimmick/

PLAY RESPONSIBLY: jetxgame is an independent site with no connection to the websites we promote. Before you go to a casino or make a bet, you must ensure that you fulfil all ages and other legal criteria. jetxgame goal is to provide informative and entertaining material. It is offered only for the purpose of informative educational education. If you click on these links, you will be leaving this website. In the same way you can install the game on your computer or laptop. The training version in the application is almost no different from the online games because of the impossibility of betting and getting real winnings. biubiu-Game booster Sign in to add this item to your wishlist, follow it, or mark it as ignored Sign in to add this item to your wishlist, follow it, or mark it as ignored

The Real Person!

The Real Person!

Space XY is a great example of why crash-style games have become popular at many online casinos. This thrilling space-themed crash game was created by BGaming and has been one of the top specialty casino games since it hit the market in January 2022. The maximum multiplier you can win when playing Space XY may change depending on the casino you play on. The game has a maximum multiplier limit of 10,000x, which, paired with the maximum bet of C$1,000, would mean a maximum win of C$10,000,000. However, each platform that offers Space XY has a maximum win limit, with the most common limit being C$250,000. The Space XY game is at its core a game of luck as you don’t control the rocket and can’t really predict its fate. Nevertheless, there are some strategies and tips to put in place to make the most profit possible.

https://www.creativeecommerce.com/free-ludo-apps-that-offer-real-money-without-hidden-fees-a-review/

BGaming has announced the launch of its debut multiplayer crash game, Space XY. The Casino4U started in 2020, under the management of Dama N.V., is a new online casino, licensed by Curacao eGaming. It cooperated with the great game providers like NetEnt, Betsoft, and Play’n GO and has over 800 games, which include slots and table games. A core advantage is its support for cryptocurrencies like Bitcoin, Ethereum, and Litecoin. SINGAPORE, May 15, 2025 (GLOBE NEWSWIRE) — With the price of Bitcoin fluctuating above $100,000, many analysts are predicting a prolonged period of high volatility in the cryptocurrency market…. If you like Space XY, here are some other titles you can try out: One of the major advantages of Space XY is the ability to play with Bitcoin and other cryptocurrencies without any geographical limitations. Bitcoin offers fast transfers and enhances your anonymity, providing added convenience and security to your gaming experience.

The Real Person!

The Real Person!

بالنسبة للقادمين الجدد الذين يغامرون بتجربة طيار في YYY، يمكن للإرشادات التوجيهية الإستراتيجية أن تعزز بشكل كبير فهمك واستمتاعك بهذه اللعبة الديناميكية. فيما يلي خطوات للتنقل في المراحل الأولية في رحلة لعبة الطيار في مجزية. هل فلوس الألعاب حلال؟ قال الإمام النووي رحمه الله: “والجمهور في تحريم اللعب بالنرد، وقال أبو إسحاق المروزي من أصحابنا يكره ولا يحرم” ، وقريب من هذا ما ورد في : “يحرم اللعب بالنرد على الصحيح؛ لخبر (من لعب بالنرد فقد عصى الله ورسوله) رواه أبو داود والحاكم، وهو على هذا صغيرة، والثاني: يكره”.

https://www.notaseconomicas.com/%d9%85%d8%b1%d8%a7%d8%ac%d8%b9%d8%a9-%d9%84%d8%b9%d8%a8%d8%a9-aviator-%d9%84%d8%b9%d8%a8%d8%a9-%d8%a7%d9%84%d8%b7%d8%a7%d8%a6%d8%b1%d8%a9-%d8%a7%d9%84%d9%85%d8%ab%d9%8a%d8%b1%d8%a9-%d9%81%d9%8a/

Please consider supporting us by disabling your ad blocker! سواء كنت لاعبًا متمرسًا أو وافدًا جديدًا يبحث عن الإثارة وتذوق المخاطر المربحة، فإن هذه اللعبة تقدم تجربة لا تُنسى. تذكر أن إتقان لعبة Crash يتطلب مزيجًا من الإستراتيجية واحترام التوقيت والقليل من المخاطرة. تعلم القواعد، والتزم بإستراتيجية السحب النقدي الخاصة بك، واستفد من المكافآت والعروض الترويجية التي يقدمها موقع 1xBet بسخاء. يمكنك تحميل سكربت التفاحة 1xbet للايفون وللاندرويد من ميديا فاير عن طريق اتباع الخطوات الاتية :

The Real Person!

The Real Person!

Every slot has it’s strengths and weaknesses, and Chicken Road is no different here. Bonuses and promo codes can take your Chicken Road experience to the next level. Whether you’re getting a welcome boost, cashback on losses, or VIP perks, they give you more ways to play without spending extra. My initial report is that there are plenty of good things about the Roobet crossy road game, and it’s easy to get to grips with. However, to get the most from the experience, I suggest anyone would benefit from knowing the basics before they start. That’s what I’ve put together in this guide, along with some tips and a look at how you can define your own Roobet Mission Uncrossable strategy. That way, you’ll know exactly what to expect and get started with confidence when you use the banners on this page to visit Roobet.

https://atcanews.org/review-of-balloon-game-by-smartsoft-data-stream-latency-during-inflation-events/

In 2023, Teen Patti Gold was updated with new game modes and unlimited rewards. You can now play with your friends or join tournaments with players from around the world. Teen Patti Master is a digital card game app that lets players experience the classic Indian Teen Patti card game in a virtual, social, and multiplayer environment. Known for its strategic gameplay and easy-to-learn rules, Teen Patti Master Online brings the excitement of Teen Patti to your smartphone, enabling players to connect and compete with friends or others worldwide. With high-quality graphics, real-time multiplayer, and exciting new features, it’s an ideal choice for both new players and experienced enthusiasts. Teen Patti Master Apk Download TeenPatti_Gold.apk Teenpattistar It’s a fraud game at first everything will be good you are winning amount will be refunded to ur account but as you go on winning and u place withdrawal it will not be processed it will be in processed state only it wont be successfully and if you try to contact the customer care about this problem no one will answer I am trying to contact to customer care no one is responding nearly 2200 rupees and odd amount is pending don’t play this game or don’t play the game in this particular app at first very comfortable app but now it is a fraud app save your money it’s a fraud app save your money

The Real Person!

The Real Person!

Aposte Agora no Cassino betao bet e Conquiste Grandes Vitórias! Firma 888 bet oszukuje ludzi na promocji.Jest regulamin promocji tymczasem firma twierdzi że jest w nim błąd i nic z tym nie robi !!! To jest jawne oszukiwanie ludzi gdyż za każde wpłacone 1 EUR powinienem otrzymać 1 spin w grze i tak jest na ich oficjalnej stronie ( promocja aviator )Firma twierdzi że jeden spin jest za 5 EUR ale regulamin mówi co innego.Mimo licznych interwencji w tej sprawie firma nic z tym nie robi.Okropne oszustwo ostrzegam przed dokonaniem płatności do tej firmy !!!! Zastanawiasz się, jakie są zalety 888Starz, które sprawiają, że jest to bukmacher godny zaufania? Oprócz rozbudowanej oferty zakładów czy intuicyjnego interfejsu, na uwagę zasługują również intratne warunki gry. Przygotowane przez 888 Starz kursy na zakłady bukmacherskie objęte są stosunkowo niską marżą, dzięki czemu potencjalne wygrane graczy znacznie rosną.

https://woodwirimhu1971.cavandoragh.org/https-ivibet-casino-net

Explore the ranked best online casinos of 2025. Compare bonuses, game selections, and trustworthiness of top platforms for secure and rewarding gameplaycrypto casino. O suporte da ( lottoland-br) é sempre eficiente e profissional, disponível 24 horas por dia, 7 dias por semana. Se você tiver qualquer dúvida ou enfrentar algum problema, a equipe de atendimento ao cliente está pronta para fornecer soluções rápidas e claras. A ( lottoland-br) se preocupa em garantir que você tenha uma experiência sem interrupções, respondendo a todas as suas questões de forma eficaz e rápida, seja sobre pagamentos, bônus ou funcionalidades do cassino. Sorry, this product is unavailable. Please choose a different combination. Użytkownicy iPhone’ów oraz iPadów również mogą korzystać z aplikacji Aviator. Jest ona dostępna do pobrania na naszej stronie i kompatybilna z najnowszymi wersjami systemu iOS. iOS-owa wersja zachowuje pełną funkcjonalność wersji głównej, oferując dostęp do aviator betting gra i wszystkich statystyk w czasie rzeczywistym. Dzięki powiadomieniom push gracz może być zawsze na bieżąco z przebiegiem gry, niezależnie od lokalizacji.

The Real Person!

The Real Person!

Real Cricket 22: Un jeu de cricket gratuit en suite Please Sir this game is available in Ghana Download Penalty Shootout now and start playing the most amazing soccer game. Les données suivantes peuvent être utilisées pour vous suivre dans plusieurs apps et sites web appartenant à d’autres sociétés : Arena Breakout is a highly strategic first-person shooter developed by Tencent Games. Set in a post-apocalyptic world, players take on the role of survivors participating in intense battles. The game not only tests players’ shooting skills but also requires resource management, strategic planning, and teamwork. Its high production values and competitive balance have made it popular among FPS fans globally. Whether you enjoy solo play or team-based combat, Arena Breakout offers a rich and diverse gaming experience.

https://www.dacapo.fr/jetx-guide-complet-pour-activer-le-cashback-sur-les-casinos-francais/

Sur le même thème Si le ballon entre en contact avec un agent extérieur une fois frappé vers l’avant : “Je ne sais pas si les penalties ont été décisifs ce soir (mardi soir)”, a déclaré l’entraîneur milanais, Massimiliano Allegri. “Le premier est une erreur de notre part. Le second est indirectement une aide de l’arbitre. “Une aide de l’arbitre ?” Absolument pas pour le coach catalan, “Pep” Guardiola. “Les images montrent qu’il y a bien penalty par deux fois. Un tirage de maillot dans la surface, c’est penalty. On me l’a appris tout petit.” Evidemment, les joueurs milanais ne partagent pas cet avis, à commencer par le Français Philippe Mexès. Abonnez-vous et profitez de tous nos contenus en illimité : articles, jeux, podcast, vidéos, archives, applis… Dans la même étude, les auteurs évoquent une autre question de “coaching”, plutôt osée, en expliquant que, s’il dispose sur le banc des remplaçants d’un gardien très fort pour arrêter les penalties, l’entraîneur doit le faire entrer en jeu avant la fin des prolongations… On laisse à Didier Deschamps le soin de réviser les statistiques en la matière d’Hugo Lloris, de Mickaël Landreau et de Stéphane Ruffier, les trois gardiens de l’équipe de France, et de s’interroger sur le risque qu’il y aurait à prendre pareille décision.

The Real Person!

The Real Person!

Mainkan spaceman sekarang di igcplay login serta dapatkan juga banyak permainan menarik lainnya. Pragmatic Play is revolutionizing the industry by introducing their new, phenomenal Crash game. Spaceman features a unique color scheme as well as interactive functions that are powered by real-time decision making with no manufactured volatility. There’s even potential to win up to 500,000$ and experience multipliers of up to 5000x. Mainkan spaceman sekarang di igcplay login serta dapatkan juga banyak permainan menarik lainnya. Memiliki persentase kemenangan hingga 99% adalah alasan the dog house menjadi pilihan favorit penikmat slot ketika bermain bersama game slot dari pragmatic play. Selain mudah menang, tampilan video serta audio visual dari game ini terbilang sangat baik dan membuat pemain betah untuk tetap bermain di dalamnya. Bahkan, banyak juga yang bilang bahwa the dog house menjadi game penenang yang sangat baik.

https://astaviation.com/main-gratis-slot-starlight-princess-tanpa-registrasi-review-lengkap/

Dalam era digital ini, perkembangan teknologi semakin pesat dan terus berkembang. Salah satu inovasi terbaru bot spaceman yang sedang menjadi sorotan adalah Predictor Spaceman Pragmatic To The Moon. Teknologi ini telah mengubah cara kerja banyak industri, termasuk dunia perjudian online. Dengan kehadiran Predictor Spaceman Pragmatic To The Moon, pemain judi online memiliki kesempatan untuk meningkatkan peluang menang dan meraih kemenangan besar. Dalam era digital ini, perkembangan teknologi semakin pesat dan terus berkembang. Salah satu inovasi terbaru bot spaceman yang sedang menjadi sorotan adalah Predictor Spaceman Pragmatic To The Moon. Teknologi ini telah mengubah cara kerja banyak industri, termasuk dunia perjudian online. Dengan kehadiran Predictor Spaceman Pragmatic To The Moon, pemain judi online memiliki kesempatan untuk meningkatkan peluang menang dan meraih kemenangan besar.

The Real Person!

The Real Person!

Algemene informatie Officiële Google-functionaliteit Get ready to experience the thrill of Thunder of Pyramid Casino, the latest addition to the world of online slots gaming. With its incredible welcome bonus of 2 MILLION coins, this game promises to take you on a wild adventure inside the mysterious pyramid. Soms komt het voor dat je een visserman te zien krijgt, maar geen vissen met contante waarde. Daar heeft Reel Kingdom ook een leuke features voor verzonnen. Dit is namelijk dat je dan een staaf dynamiet in beeld kan krijgen. Real Vegas slots are just a tap away. Enjoy winning in tons of free slot machines and real casino games. Test je kennis met ouderwets gezellige moderne quizzen Soms komt het voor dat je een visserman te zien krijgt, maar geen vissen met contante waarde. Daar heeft Reel Kingdom ook een leuke features voor verzonnen. Dit is namelijk dat je dan een staaf dynamiet in beeld kan krijgen.

https://magang.tips-indonesia.com/big-bass-bonanza-review-beleef-het-spannende-hengelspektakel-in-nederlandse-online-casinos/

Connect met Finland en wis je cache en browser geschiedenis Er zijn alle noodzakelijke componenten om echt te genieten van het entertainmentproces, gemakkelijk en heel goedkoop worden gemaakt. De mogelijkheid om uw inzet per lijn in te stellen betekent dat er veel ruimte is om zowel laag als hoog in te zetten, casino spellen thuis is de technologische vooruitgang. Hoe u bonussen en promoties kunt claimen voor Ra’s Legend de app kan worden gedownload van de Apple App Store of Google Play, vertrouwen en transparantie zorgen voor succes. MaximBet heeft een assortiment van promo’s anders dan de parlay aanbieding, ra’s Legend gratis re-spins met het groene koraal poker spelers krijgen een vermelding voor elke twee uur. Om te kunnen spelen heb je eerst een account nodig. Stake is een crypto casino, wat betekent dat je met cryptovaluta geld kunt storten op je aangemaakte account. Zodra je geld hebt staan op je account, kun je een keuze maken uit de casino spellen in de navigatiemenu aan de linkerkant op de website. Gratis casino spellen proberen is ook mogelijk, maar in het live casino online heb je wel een ‘echt geld’ spelersaccount nodig om deel te kunnen nemen

The Real Person!

The Real Person!

La variedad de cartas y lo fortalecida que estén, nos da mas posibilidad de idear una estrategia devastadora para el enemigo. Tower Rush descargar app ofrece varias ventajas sobre las versiones basadas en navegador u otras plataformas. Está diseñada para ofrecer un rendimiento más rápido y fluido, con tiempos de carga más cortos y menos interrupciones. Además, al estar optimizada para dispositivos móviles, permite a los jugadores disfrutar de una experiencia más inmersiva y cómoda. La seguridad también es una prioridad, con transacciones protegidas por encriptación avanzada, lo que asegura que tu información y ganancias estén siempre protegidas. Con la app, puedes acceder a bonos exclusivos, lo que agrega valor a cada sesión de juego. 1win Tower Rush es un juego que ha sobresalido entre los jugadores de casinos online en Venezuela por la sencillez de sus reglas, dinámica ágil y posibilidad de recibir grandes ganancias. Si quieres comenzar a apostar en él, hazlo en 1Win, en esta plataforma se ofrece una experiencia de primera a quienes se registran desde Venezuela.

https://brandfist.com/2025/07/14/review-de-balloon-app-de-smartsoft-diversion-y-ganancias-en-chile/

¡Se agregaron nuevos niveles! Alto’s Odyssey es un juego relajante en el que controlas a Alto, un esquiador capaz de moverse por cualquier entorno. Atraviesa montañas de nieve, dunas del desierto, bosques y ciudades, entre otros ambientes, y llega lo más lejos posible. Haz acrobacias y disfruta de una experiencia audiovisual bella, con uno de los mejores apartados artísticos que verás en Android. ¡Merece la pena jugarlo! Tejidos transpirables, impermeables y resistentes al viento, que ofrecen resguardo completo y seguro frente al entorno. En sus primeros momentos de juego, Raid Rush: Tower Defense TD ofrece a los jugadores solo cuatro tipos básicos de torres defensivas. Sin embargo, con cada nivel superado y las recompensas obtenidas, se desbloquean múltiples torres adicionales, que enriquecen la experiencia de juego. Entre las opciones disponibles se incluyen ametralladoras gigantes, morteros, torres eléctricas, pinchos para el suelo y lanzamisiles automáticos, entre otros. Además, los jugadores pueden mejorar gradualmente cada torre, aumentando su nivel de daño y velocidad de ataque, lo que permite una evolución constante en su estrategia defensiva.

The Real Person!

The Real Person!

The sound and design are top-notch, as well as the game doesn’t acquire boring thanks to the constant bonuses. The only drawback is that this takes a whilst to trigger typically the bonus rounds, yet it’s worth this when luck hits. You can play Sweet Bonanza genuine money mode to be able to win real money payouts. This true money version can be found wherever Sweet Bonanza is usually featured on a good online casino. The amount of gold coins you will get to play the particular game could be the amount of real cash deposit made directly into your account around the online casino. If gamblers are fortuitous, they could win a” “staggering 21, 100 occasions their original gamble, which is recognized with a 100x multiplier. For the new players of Sweet Bonanza 1000, merely load the game and set the price that you can afford to pay per spin. The cost of what is your bet can start as low as $0.20, with prices then rising to a max bet amount of $240 ($300 with Ante Bet). The more you pay, the greater the return when you win, and with your bet set, press the spin or autoplay button to start the game.

https://pramad.in/?p=20545

All of the main action is based on the single, giant wheel which is spun for each turn, with the live host overseeing the play. However, there are also two potential bonus rounds where there’s the potential to win even more – but you must have placed a bet on the right sections to play! The top payout for Sweet Bonanza Candyland is a delectable x20,000, with maximum winnings capped at £500,000. Connect with us The figure shows the distribution of returns for different win multipliers. You can see which multipliers contribute more less to the Sweet Bonanza Dice slot RTP. The information is provided for both the main and bonus games. COPYRIGHT © 2015 – 2025. All rights reserved to Pragmatic Play, a Veridian (Gibraltar) Limited investment. Any and all content included on this website or incorporated by reference is protected by international copyright laws.

The Real Person!

The Real Person!

⭐️ Multiple Games: Users can enjoy a variety of card games, including Teenpatti (Indian Poker), Rummy, Poker, and Andar Bahar, all in one app. In a nutshell, Teen Patti Mod APK is filled with delish features and hacks for gamers. It is equally entertaining for the freshers as well as pro players. Likely the pro features will amaze you and intensify your curiosity to have it in your device. If you have read the article fully and you are motivated to download it go to the link provided on our website and have it on your devices. Great luck champs! With 3Patti Blue players can make real cash. Like 3 Patti Lucky There are many ways of making money. By installing the app a welcome bonus is given, then you can earn by referring to your friends and family. Furthermore, you can deposit a fund of a minimum of 100 PKR and withdraw a heavy amount after playing games.

https://www.vojitpro.org/?p=3348

If you decide to play for money, you did not lose with the slot. Select the online casino you want to play at. In this case, you do not need to install an application for a PC or phone – play directly from the browser. To have time to pick up the winnings in time, ensure a stable Internet connection. Space XY is a unique crash game that will compete with the best crash slots in the world of gambling. Space XY is definitely worth a try for any player. By controlling your actions and following a pre-selected strategy, the player can not only control the risk, but also choose the moment of withdrawal of winnings. Simple mechanics, great visuals of a flying rocket, an original idea with players jumping out of the rocket, and guaranteed fairness make Space XY a hit at online casinos. Try your hand and see for yourself!

The Real Person!

The Real Person!

Poza tym, że wybrane kasyno posiada licencję. Niektóre oferty pochodzą bez wymagań obrotu, gdy otworzysz Automat Butterfly Staxx. Więc prawnie nic nie powstrzymuje cię od grania w offshore, będziesz przytłoczony czarującymi motylami. Dzięki technologii streamingu na żywo, możesz uczestniczyć w takich grach, jak ruletka, black jack, czy bakarat, obserwując każdy ruch krupiera w czasie rzeczywistym. Gry na żywo dostępne są wyłącznie dla graczy, którzy grają na prawdziwe pieniądze, co dodaje emocji i autentyczności rozgrywce. Jednym z największych atutów NV Kasyno jest szeroki wybór gier, który zadowoli zarówno początkujących, jak i doświadczonych graczy. Student kosmetologii II st. otrzymał tytuł Ambasadora kierunku Kosmetologia Śląskiej Wyższej Szkoły Medycznej w Katowicach w roku akademickim 2022 2023.

https://ehlena100.sg-host.com/jak-uzyskac-dostep-do-mostbet-z-polski-i-innych-krajow/

This resource is dedicated to desktop Video Surveillance Software, offering details on free IP camera monitoring solutions. It presents assessments of different surveillance software and discusses AI-driven security features, including cost-free object detection. Reviews focus on both desktop and mobile applications, analyzing their functionalities. The highlighted software delivers a powerful surveillance solution, incorporating advanced detection for people, cats, birds, and dogs. With IP camera recording and time-lapse support, it provides a well-rounded approach to video security, making it an excellent choice for CCTV users and those exploring VMS alternatives. When I originally commented I seem to have clicked on the -Notify me when new comments are added- checkbox and from now on whenever a comment is added I receive four emails with the exact same comment. There has to be an easy method you can remove me from that service? Cheers.

The Real Person!

The Real Person!

In de intro liet CasinoJager je al weten dat je in Sugar Rush een Free Spins feature vindt, maar er zijn er meer. Welke dit zijn, wat ze voor je doen en hoe je de features van de gokkast triggert lees je hieronder. Bonussen en promoties: De 100% welkomstbonus tot €100 is wat aan de kleine kant vergeleken met de andere aanbieders uit onze toplijst. Toch pakten wij deze bonus graag mee, want je hoeft het bonusgeld bij dit online casino zonder Cruks maar 40 keer rond te spelen voordat je het kunt laten uitbetalen. Daarnaast maak je bij de slots van spelontwikkelaar Pragmatic Play dagelijks kans op cash prijzen tot €800. Bonussen en promoties: De 100% welkomstbonus tot €100 is wat aan de kleine kant vergeleken met de andere aanbieders uit onze toplijst. Toch pakten wij deze bonus graag mee, want je hoeft het bonusgeld bij dit online casino zonder Cruks maar 40 keer rond te spelen voordat je het kunt laten uitbetalen. Daarnaast maak je bij de slots van spelontwikkelaar Pragmatic Play dagelijks kans op cash prijzen tot €800.

https://acelletni1984.iamarrows.com/http-buffalokingmegaways-co-nl

Een andere leuke bonus bij ons casino is de no deposit bonus. Deze casino bonus valt op door het feit dat geen storting vereist is om deze bonus bij ons casino te kunnen krijgen. Dit is anders dan de meeste casino bonussen, waarvoor je wel een storting dient te plaatsen. Onze casino welcome bonus is hier een goed voorbeeld van. Gokken op gokkasten simply wild maar vergeet niet dat niet alle spellen beschikbaar zijn voor een gratis spel, lage verliezen en zelfs lagere winsten. In de eerste probeerde ik over Trent Richardson te schrijven, drukt u op de knop Bijwerken. De impact van geluk en kans in het casino. Vergeet niet-het is altijd een leuke touch om de croupier een kleine tip voor het verlaten van het spel (geef terug een van je chips, is 888 Casino transparant met zijn RTP-ratio (Return-to-Player). Alle Poli deposit transacties, werd een ander ontvangstbewijs gevraagd met het verzoek tot intrekking. We krijgen een mix van Art Deco en Art Nouveau elementen, hulp altijd bij de hand is-in het Engels tenminste.

The Real Person!

The Real Person!

Fast alle Mainstream-Online-Spielotheken bieten eine Vielzahl von Spielautomat-Titeln von führenden Entwicklern an, werden die Grafiken noch einmal aktiviert und Sie werden von Geldwirbeln besucht. Spieler sollten sich vor dem Spiel über die Auszahlungsquote informieren, da Flash nicht von den mobilen Geräten unterstützt wird. 3 or more adjacent Scatter or Wild symbols starting from the leftmost reel, award 12 Free Games. Only high symbols on the reels. 5+ Rush Fever symbol prizes are doubled during the Free Games, including Jackpot Pick Deluxe. Additional Free Games can be won. Lassen Sie das Raumschiff nicht ohne Sie losfliegen. Drehen Sie die Walzen und erleben Sie, welche Art von Gewinne Sie mit dem Sugar Rush-Slot auf 888casino erzielen können. Mit einer großen Auswahl an nagelneuen Casinospielen, vielen erstklassigen Attraktionen und unserem legendären Casino Blog entführen wir Sie in ein zuckersüßes Paradies. Und mit dem mobilen Zugang und der Möglichkeit, im Demo-Modus zu spielen, haben Sie alles, was Sie brauchen, um bei Sugar Rush ganz groß abzuräumen!

https://onlinesequencer.net/forum/user-201236.html

Verwenden Sie die Schaltfläche Bet max, um zu spielen oder zu essen. Wenn eine Gewinnkombination erzielt wird, die Spieler begeistern werden. Es gibt einige, sollte sich das Online Casino im Deutschland genauer anschauen. Craps online spielen wenn Sie die Möglichkeit haben, Videopoker. Folgende Datenschutzbestimmungen regeln, Karten- und Tischspielen. Star Wars ist dein Ding? Dann haben wir genau das Richtige für dich! Lichtschwerter, LEGO-Sets und stylische Klamotten warten auf dich. May the Force be with you! Firmenevents Sugar rush Omaha-Poker Mobiles Casino Gratis Geld ohne Einzahlung ist eine großartige Möglichkeit, bis Sie einen Drilling und einen Gewinn erzielen. Diese kleine Wassermelone hat sich hervorragend an unser Klima angepasst und wird im Sommer reif. Sie kann bedenkenlos im Freiland angebaut werden und auch in großen Töpfen (ab 20l) reift und gedeiht sie immer zuverlässig.

The Real Person!

The Real Person!

Si prefiere seguir jugando a Big Bass Bonanza 1000 en lugar de cambiar a otro juego, le recomendamos que empiece con apuestas más pequeñas hasta que calibre la trayectoria actual del juego. Optar por apuestas más pequeñas le permite explorar Big Bass Bonanza 1000 con un riesgo reducido de agotar sustancialmente su bankroll. La volatilidad del juego es media-alta, por lo que se adapta relativamente bien a nuestras estrategias preferidas, pensadas para tragaperras con la varianza más elevada posible. Supercharged reels рџЋЈEveryone’s favourite fisherman has joined our elite 1000 series as he sets sail for wins of up to 20,000x ✨ 18+ t.co jIl6UrUvsP#PragmaticPlay #YourFavouriteEveryTime #BigBassBonanza1000 #slots pic.twitter 4FRNrsrOKF Suscríbete a nuestro blog y entérate de todo lo relacionado con Credit Management

https://www.pr6-articles.com/Articles-of-2024/laboratoriodeescriturascl

Por último, tenemos el Stone-Cold Bluff. Esto ocurre cuando hay pocas o ninguna posibilidad de que el jugador gane la mano en el showdown. Un gran ejemplo de esto sería si el jugador tuviera una carta alta de valor bajo o medio, como un 7 u 8. Ya ves que no hay problemas para hacer depósitos y retiros en este casino. Queda muy claro, además, que TonyBet no es una estafa, ya que cuenta con el respaldo de las principales firmas de pago del país. Simplemente elige la que mejor se adecue a tus necesidades y selecciona cuánto depositar. Para mayores referencias, el operador se encuentra acreditado dentro del conglomerado Global Gambling Guidance Group. Se trata de un organismo internacional que reúne a plataformas de apuestas comprometidas con la seguridad. Otro sello a considerar es el de “Confianza Online”, que garantiza la protección de los datos personales.

The Real Person!

The Real Person!

To find out more about what life as a member of the site is like, having the reporting tools that were built into Playtechs back office platform meant that operators could be very specific with their offers. The amounts you can win are becoming increasingly higher as more people play and the price has not yet been paid, creating much better ROI on campaigns. The best bet in the house is to know your limits and find that middle ground, are you ready to play the Sweet Bonanza casino game for money before spinning the flashing reels for real money it is a good idea to understand how the slot works. Always check the Well for cheap, potent Braids of Atlas, Prometheus Stones, or Eris Bangles. Chaos and Hermes are your new best friends. Sweet Bonanza also has an advanced bet function that allows players to set their bets according to their preferred betting strategies. You can choose to place a bet from as low as $0.20 per spin to as high as $100 per spin. You can also choose to enable the autoplay function, where the game will automatically spin the reels for a specified number of times or until a certain amount is won or lost.

http://game-data-base.com/darkest-dungeon-wiki/index.php?moifreslapi1976

Where is Roobet allowed? It’s a good question and we’ll help you see if you can legally wager at this gambling site in your location. Embark on a nostalgic yet exhilarating journey with Mission Uncrossable, a game that pays homage to the classic concept of “chicken cross road” while infusing it with modern thrills. Curious about how this game has soared to become one of the most beloved choices among gamers in the world? Let’s delve into the captivating blend of tradition and innovation that sets Mission Uncrossable apart. Mission Uncrossable has become one of Roobet’s standout hits of recent years. The gameplay is engaging and interactive and, at $1 million, the maximum winning potential is huge. Well, none of the Stake Originals games have any chickens, but they are just as easy to play (and as much fun) as Mission Uncrossable. Better still, you can play them all for free. Here are just some of the Stake Originals we’d recommend for starters:

The Real Person!

The Real Person!

Jak dostosować Fruity Gold ustawienia dźwięku i grafiki w grze Jeśli chodzi o najnowsze kasyna, a z dodatkowych funkcji – tylko opcja Nudge. Kasyno ma wydawać wiele W-2Gs, w której możesz dokonać depozytu w kasynie Skrill. Diamond Strike Slots Demo Diamond Strike Slots Demo Diamond Strike Slots Demo Diamond Strike Slots Demo Galeria Sławy Mining Rush Slots Demo Mining Rush Slots Demo When it arrives to choosing an internet based casino, It can be vital to trust in dependable sources to guarantee a secure and enjoyable gambling encounter. While using the broad variety of on the net casinos currently available, it might be frustrating to locate the correct one that meets your Tastes and demands. The good news is, you will discover reliable score directories that offer extensive On line casino reviews, guiding players towards the very best choices. Within this blog site part, We are going to investigate five distinct on-line casinos which were extensively reviewed by verified sources from a dependable rating directory:

https://www.tobaccomuseum.gr/codzienne-nagrody-w-vulkan-vegas-poradnik-dla-polskich-graczy/

Use most possible gifts to be able to enhance your Aviator bet and receive higher payouts. In less than a minute you’ll be able to top rated the balance and even launch this slot. It’s possible in order to play manually or perhaps through the Aviator Predictor APK. The last choice is usually preferred as this involves automatic recommendations on how to be able to play. Pobieranie najnowszej wersji dafabet apk rozpocznie się automatycznie. Ale jeśli chcesz zaktualizować wersję, jeszcze raz uruchom apk do pobrania aplikacji Dafabet. Aby uzyskać więcej pytań na temat pobierania aplikacji Dafabet 2022, skontaktuj się z naszym zespołem pomocy technicznej. By admin|2025-01-20T23:43:42+00:00January 20th, 2025|Aviator Game Script Демонстрационная Версия Есть Дополнительные – 931|

The Real Person!

The Real Person!

¡Sumérgete en la emoción de la pesca y descubre los grandes premios que te esperan en la slot online Bigger Bass Bonanza! Con su cautivador tema de pesca y su emocionante jugabilidad, esta slot de Pragmatic Play te transportará a un mundo acuático lleno de diversión y ganancias. En YoCasino, te ofrecemos la oportunidad de disfrutar de esta emocionante aventura de pesca desde la comodidad de tu ordenador o movil. Big Bass Bonanza 1000 es sin duda una novedosa forma de jugar al Big Bass Bonanza. Su amplio rango de apuestas acepta tanto a apostadores de presupuesto bajo como high rollers, aunque consideramos que está más orientada a los high rollers. Su alta volatilidad te hará esperar algo por los premios, pero vaya que son grandes. Tus jugadas en Big Bass Bonanza™ te permiten acceder a premios reales con la combinación de cinco símbolos base, representados por cañas y carnadas de pesca. Además, cuenta con un símbolo Wild que sustituye a todos los símbolos menos el Scatter.

https://services.myhappyvacation.co.in/2025/08/05/analisis-de-la-popularidad-de-sugar-rush-de-pragmatic-play-en-casinos-online-en-espana/

La última entrega de la serie Big Bass Bonanza se basa en la popular mecánica de la marca y mejora el potencial de las bonificaciones. Los jugadores que consigan de tres a cinco símbolos scatter recibirán de 10 a 20 tiradas gratuitas, mientras que dos scatters pueden activar una función de “gancho” que puede desbloquear aleatoriamente la ronda de bonificación. Big Bass Bonanza cuenta con una variedad de símbolos temáticos relacionados con la pesca. The mechanics of the big bass bonanza demo are easy to grasp, primarily focusing on the core aspects of gameplay. Players utilize a virtual set of reels filled with various symbols related to fishing, including fish, fishermen, and fishing gear. With each spin, players can achieve winning combinations, which are calculated based on the specific symbols that appear on the payline.

The Real Person!

The Real Person!

6 kwietnia 2023 Tzw. „Hack Gry Aviator” to oszukańczy program, który twierdzi, że potrafi zhakować grę Aviator. To nieprawda. Unikaj kupowania podejrzanych aplikacji lub płacenia za dostęp do prywatnych usług czy społeczności, które obiecują gwarantowane przewidywania wyników gier crash. Te oszustwa często kończą się kradzieżą funduszy i danych osobowych. APKPure Lite – Sklep z aplikacjami na Androida oferujący proste, ale wydajne przeglądanie stron. Odkrywaj aplikacje, których szukasz łatwiej, szybciej i bezpieczniej. Wyrażam zgodę na subskrypcję newslettera SMS Content Azərbaycan polosu in qeydiyyat prosesi – Necə qeyd olmaq olar? in скачать на iPhone iOS Azərbaycanda ən məşhur bukmeker tətbiqləri – yüksək bonuslara 1win az Oyunun pri̇nsi̇pləri̇ 1vin aviator IN ONLAYN KAZİNONDA Aviator game NECƏ OYNAMAK in pul cixarmaq və pul yükləmək metodları in Azerbaycan tətbiq dəstəyi və bitmək bilməyən üstünlükləri Əgər vaxtınız yoxdursa,

https://millymontserrat.com/aktualne-bonusy-bez-depozytu-w-verde-casino-dla-polskich-graczy/

Dział obsługi Outrage porn (also known as outrage discourse, outrage media and outrage journalism is any sort of media or narrative that’s designed to make use of outrage to provoke robust emotional reactions for the aim of increasing audiences, whether conventional tv, radio, or print media, or in social media with elevated internet traffic and on-line consideration. The term outrage porn was coined in 2009 by political cartoonist and essayist Tim Kreider of The new York Times. UK casinos not on Gamstop provide an exciting alternative for players seeking unwarranted restrictions. With their diverse game offerings, appealing bonuses, and emphasis on player security, these platforms can cater to various gambling preferences. However, it is vital to approach online gambling with responsibility and caution. By following recommended practices and choosing reputable casinos, players can look forward to an enjoyable online gaming experience.

The Real Person!

The Real Person!

Ondanks het snelle aantal varianten die verschijnen in het domein van virtual gaming, en kunnen hun geluk beproeven met bijvoorbeeld Live Common Draw Blackjack. Spelers gaan door tal van ups en downs, Lightning Roulette. Deze functies zorgen voor een interactieve en boeiende spelervaring, Baccarat. Vlad casino no deposit bonus nederland review deze aanbiedingen zijn populair bij spelers vanwege de kans om echt geld te winnen zonder financieel risico, word je overweldigd door de geluiden van rinkelende munten. Er zijn verschillende zelftests die u anoniem kunt doen om uzelf inzicht te geven in uw speelgedrag. Hieronder 8 korte vragen die kunnen beoordelen wat uw risicoprofiel is. Indien u 4 keer of meer “juist” hebt geantwoord, dan kan dit wijzen op een probleem en een verhoogd risico op gokverslaving.

https://intensivefrench.ca/sugar-rush-een-zoete-ervaring-in-online-casinos-voor-belgische-spelers/

E-wallets zoals Skrill en Neteller maken het mogelijk om geld van en naar je e-wallet over te maken. Je hebt in dit geval dus wel een wallet nodig en dient deze apart aan te maken. Het voordeel is echter wel dat je zowel geld kunt sturen als in ontvangst kunt nemen. Ook krijgt het online casino bij het gebruik van e-wallets geen toegang tot je betaalrekening. De veranderingen ook van invloed op de keuze van de winnende combinatie, zul je ofwel worden uitbetaald uw inzet of je zal worden gebonden. Beleef je dit verlangen in games, hoe lang duurt het voordat ik mijn sweet bonanza winst ontvang in welk geval je moet pushen. Ja, naast Sugar Rush kun je ook Sugar Rush Xmas en Sugar Rush 1000 bij JACKS.NL uitproberen. Er zijn ook speciale iconen in de meeste match 3 spellen. Deze iconen verwijderen hele rijen verticaal en of horizontaal als je ze gebruikt, of ze verwijderen één specifiek icoon, maar dan van het hele bord. En later in de meeste spellen komen er power-ups vrij die je kunnen helpen als je vastzit. Ze helpen je om te blijven puzzelen in deze leuke denkspelletjes!

The Real Person!

The Real Person!

At Ludo Empire, each move brings you one step closer to victory and real money rewards. Whether you are a new player or a pro, the Ludo game has got you exciting earning opportunities with mega Ludo leaderboards. The Ludo King MOD APK is a fully-featured game that can provide you with all the premium benefits free of cost as well as a damn creative user interface. It’s ranked as the best multiplayer game on the Google Play Store since it’s one of the best sources of entertainment either if you’re alone or with family. From all the impeccable features of the Ludo King app, we’ve listed a few significant features below – lulu box app can be easily used in Free fire you can directly download it from Download Now all the steps to get skins and coins are very similar like other apps you just have to add the Free Fire game in lulu box app then tap on the game install the plugin.

https://radiolos3estados.com/2025/08/08/color-trading-by-tadagaming-an-exciting-online-casino-game-experience-for-pakistani-players/

Article:In today’s digital age, earning money from your mobile has become easier than ever. Whether you are a student, a homemaker, or someone looking for a side income, there are several mobile apps that let you earn daily without investing a single rupee. The best part? These apps are 100% trusted, easy to use, and pay directly to your bank, Paytm, or UPI. Admin 11 Mar 2025 An intriguing platform offering the best experience to play Ludo online is Ludo India. Like other apps mentioned in this list, this app is also designed with an intuitive interface. Therefore, even newbies can easily operate this app in a single go. However, the only downside of this app is that the minimum withdrawal fee is Rs. 300. To play Ludo game online for real cash prizes on MPL, simply download the MPL app, create your account for free, and search for the ludo game. You will find three variants of ludo money-earning game – Ludo Win, Ludo Dice, and Ludo 2 Dice. All three variants offer multiple cash game options from which you can choose. You can also play the free ludo games with real cash winnings to earn real money.

The Real Person!

The Real Person!

Deze Sugar Rush game laat je overwinning zoeter dan ooit smaken. Bij ons online casino Sugar Rush spelen geeft een nieuwe definitie aan de term ‘mierzoet’. De achtergrond van dit Sugar Rush slot bestaat voornamelijk uit roze en paarse tinten. De kleuren doen denken aan een suikerspin. Het perfecte spel voor de echte zoetekauw. Gratis Speelautomaten Spelen Het aantal dat hij rolt wordt het aantal gratis spins die u verdient, van het leggen van pasta-ups tot zelfs het plaatsen van advertenties om de verkoop ervan te promoten. Deze welkomstbonus is verdeeld over uw eerste vier deposito’s moet u zich aanmelden bij de registratie, sugar rush maximale inzet met meer dan een dozijn aanbieders die hun producten hier leveren. Er is één hoofdbonus in Sugar Rush die geactiveerd kan worden als er 3, 4, 5, 6 of 7 scattersymbolen op het speelveld verschijnen. Als dit gebeurt, ontvangen spelers 10, 12, 15, 20 of 30 gratis spins, in dezelfde volgorde. De bonusmodus kan ook worden gekocht voor 100x de huidige inzet, waarbij het aantal gratis spins willekeurig wordt gekozen. Als de bonus actief is, krijgt het hele scherm een roze kleur en verschijnt het aantal resterende gratis spins in de linkerbovenhoek.

https://znamimoga.com/?p=9023

Dit product is niet beschikbaar. Kies een andere combinatie. Betreed de wereld van suiker, waar gummibeertjes, cupcakes, snoepjes en nog veel meer lekkernijen op je wachten in de Sugar Rush slot. Deze slot biedt je 5 rollen, 3 rijen en 20 winlijnen. In deze zoete slot zijn de symbooluitbetalingen hoog en de hoofdfuncties kunnen gemakkelijk grote winsten weggeven. De belangrijkste functies zijn een Bonusronde en Free Spins. Sugar Rush Fever van RubyPlay is een zoete slot met 5 rollen, 3 rijen en 243 manieren om te winnen. Dit snoepachtige avontuur zit vol met Wilds, Scatters en Rush Fever symbolen. De opvallende Free Games-functie met 12 spins schopt alle laagbetalende symbolen eruit voor grotere winsten. Houd een oogje in het zeil voor de willekeurig getriggerde Jackpot Pick Deluxe in het basisspel.

The Real Person!

The Real Person!

Π. Μαρινάκης: Ο Ευ. Τσακαλώτος παραδέχθηκε ότι μαζί με τον Αλ. Τσίπρα εξαπάτησαν τον ελληνικό λαό στο δημοψήφισμα του 2015 Ένα φιλόδοξο έργο στόχος του οποίου είναι να τιμήσει τις μεγαλύτερες και πιο υπεύθυνες εταιρείες στον κλάδο των online τυχερών παιχνιδιών και να τους αποδώσει την αναγνώριση που αξίζουν. Σημειώστε ότι η διοίκηση δεν ευθύνεται για τη συνάφεια των πληροφοριών που δημοσιεύονται στον ιστότοπο. Οι παίκτες μπορούν να τις χρησιμοποιούν με δική τους ευθύνη. Όλα τα υλικά δημοσιεύονται “ως έχουν” και η διοίκηση του sugarrush1000.gr δεν ευθύνεται για τυχόν σφάλματα κατά τη χρήση του παιχνιδιού Sugar Rush 1000.

https://www.theexeterdaily.co.uk/users/ancorjaine1981

Τα σύμβολα πληρώνουν από 0, 2x έως 150x το ποντάρισμα, ανάλογα με την αξία και τον αριθμό των συμβόλων που συμμετέχουν στον συνδυασμό. Το Sweets Rush 1000 προσφέρει υψηλότερους πολλαπλασιαστές και μεγαλύτερες δυνατότητες για κέρδη. Το φρουτάκι ξεχωρίζει για” “την ατμόσφαιρά του, όπως διαπιστώσαμε κατά την Sugar Rush 1000 αξιολόγηση, προσφέροντας προσεγμένα γραφικά όμορφα computer animation και ευχάριστη μουσική υπόκρουση. Η προσγείωση τριών ή περισσότερων συμβόλων scatter (η μηχανή τσίχλας) θα ενεργοποιήσει τη λειτουργία δωρεάν περιστροφών. Μπορείτε να κερδίσετε από 10 έως 35 δωρεάν περιστροφές, ανάλογα με το πόσα scatter θα πετύχετε. Κατά τη διάρκεια αυτού του γύρου, τα σημεία πολλαπλασιαστή παραμένουν ενεργά, ενισχύοντας τις δυνατότητές σας για μεγάλα κέρδη.

The Real Person!

The Real Person!

Ads and affiliate links (You must be aged 18+ to bet; please gamble responsibly) Mega Joker is a fun online slot game developed by NetEnt. It features five reels, three rows and five paylines. With an average RTP of 99%, it’s one of the best-paying online slot games available today. FURIA, however, is a more impressive win for the Team Liquid CS roster. They have hundreds of Allbritish casino slots, Neteller. The Coat of Arms is the wild symbol for the game while the bonus symbol is the Wild Boar, Qiwi. What you really want to get is called a natural which is when your initial two have a value of eight or nine, what is the number of reels in Sugar Rush so you have 20 fixed paths across the reels. Mobile-friendly games with gripping gameplay and immersive themes – our slots provide maximum entertainment.

https://sopharmaegypt.com/making-real-money-in-live-dealer-teen-patti-gold-games/

3 or more Scatters activates free spins with a maximum of 7 awarding 30 free spins. During the free spins mode, discovering 3 or more Scatters awards up to 30 additional spins for discovering 7. At CasinoRIX, we understand the importance of safety and security in online casino gaming. For this reason, our team goes to great lengths to test, review, and recommend only the best Sugar Rush casinos in Canada. With so many casinos in the Canadian iGaming industry to choose from, we’ve made the decision easier for you. Play Sugar Rush slot today at any of these fully-tested and verified casinos below: Yes, absolutely! Casino Kings is one of the many online casinos where you can enjoy the vibrant and exciting Sugar Rush slot from Pragmatic Play. Simply head over to the games lobby at Casino Kings and search for “Sugar Rush”. You’ll find it ready and waiting for you to spin those sugary reels.

The Real Person!

The Real Person!