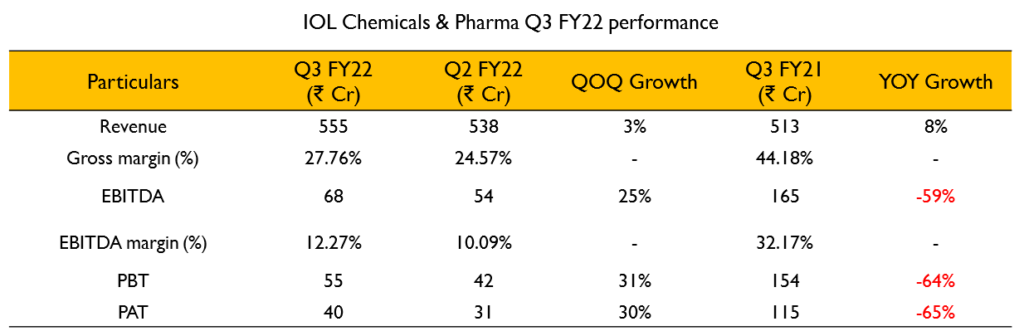

- Total revenues for the quarter were at ₹555 Cr (3% growth QoQ). EBITDA from the quarter stood at ₹68 Cr (25% growth QoQ). EBITDA margins for the quarter were at 12.1%. PAT for the quarter was at ₹40 Cr (29% growth QoQ).

- Non-Ibuprofen pharma business has performed better than Q2 and contributed 17% to the revenues. Overall, 37% of revenues from the Pharma segment comes from non-Ibuprofen.

- They filed 4 DMFs during the quarter, and they got GMP certification from MoH Russia for 6 products. They also got approval from the Korean FDA for 2 products during the quarter.

- Margins have been under stress due to continuous volatility in chemical prices and lower volumes in the Ibuprofen business.

- In the current year, they have spent ₹116 Cr in capex and they expect to spend about ₹150 Cr annually for the next couple of years.

- What matters in the API business is the cumulative capex rather than QoQ capex. They have spent over ₹400 Cr in capex over the last several years and many of those assets are still waiting to be fully utilized.

- Capacity utilization is currently at 65-75% depending on the asset, block and product.

- Ibuprofen volumes were 10% above Q2 level. Pricing is still negative. They believe the Ibuprofen business has bottomed out both in terms of volume and pricing.

- Most of their Ibuprofen business is in India and semi-regulated markets. In these markets there are no contracts. For the regulated markets they are expecting annual contracts in the range of $11/kilo.

- IBB prices are stable however they are facing pressures related to manufacturing rather than RM costs. The increase is more due to increase in energy prices.

- They have some dependency on China for Metformin and no dependency on China for Ibuprofen.

- Metformin contributes to about 16-17% of revenues. After Ibuprofen, Metformin is the largest revenue generator for IOLCP.

- All the facilities that they are building currently are multi product API plants. They are doing this to mainly de-risk the business in case any of the APIs go out of business.

- They expect Q4 to be similar to Q3 in terms of demand and profitability for Ibuprofen. They expect a 10% demand increase in the next financial year.

- BASF is back in Ibuprofen and it is putting pressure on players that are not sufficiently backward integrated. BASF’s plant is fully automated so the capex they have incurred on that is probably very high. IOLCP believes they can beat them on price.

- Over the past 2 years, most of the growth in the business has come from the non-Ibuprofen pharma portfolio. The management is trying to constantly de-risk the business from the cyclicality of Ibuprofen. They expect about 40% of next year’s pharma revenues to come from the non-Ibuprofen portfolio.

- The strategy is that 5 years from now, Ibuprofen will be a minority part of the overall pharma business

Your article helped me a lot, is there any more related content? Thanks!

The Real Person!

The Real Person!

kamagra en ligne: kamagra en ligne – Kamagra pharmacie en ligne

The Real Person!

The Real Person!

Acheter Kamagra site fiable: Kamagra Commander maintenant – Achetez vos kamagra medicaments

Kamagra pharmacie en ligne: kamagra livraison 24h – kamagra pas cher

acheter kamagra site fiable: Achetez vos kamagra medicaments – kamagra en ligne

The Real Person!

The Real Person!

Kamagra Oral Jelly pas cher: Achetez vos kamagra medicaments – Achetez vos kamagra medicaments

The Real Person!

The Real Person!

pharmacie en ligne livraison europe: Pharmacie en ligne livraison Europe – Achat mГ©dicament en ligne fiable pharmafst.com

The Real Person!

The Real Person!

Kamagra pharmacie en ligne: kamagra 100mg prix – kamagra 100mg prix

The Real Person!

The Real Person!

reliable canadian online pharmacy: canadian pharmacy prices – canada discount pharmacy

The Real Person!

The Real Person!

reputable canadian pharmacy: Express Rx Canada – cheapest pharmacy canada

The Real Person!

The Real Person!

mexican online pharmacy: mexican online pharmacy – Rx Express Mexico

canadian pharmacies online: 77 canadian pharmacy – canadian pharmacy drugs online

Medicine From India buy prescription drugs from india indian pharmacy online shopping

The Real Person!

The Real Person!

mexico drug stores pharmacies: Rx Express Mexico – mexico pharmacy order online

canadian pharmacy no scripts: Express Rx Canada – canadian pharmacy com

mexico pharmacy order online mexico pharmacies prescription drugs Rx Express Mexico

The Real Person!

The Real Person!

indian pharmacy online shopping: Medicine From India – indian pharmacy online

indian pharmacy: indian pharmacy – Medicine From India

canadian pharmacy mall Canadian pharmacy shipping to USA canadian pharmacies that deliver to the us

The Real Person!

The Real Person!

canadian pharmacy near me: Express Rx Canada – canadian pharmacy world reviews

canada drug pharmacy: Canadian pharmacy shipping to USA – canadian pharmacy reviews

The Real Person!

The Real Person!

pin up azerbaycan: pinup az – pin-up casino giris

The Real Person!

The Real Person!

вавада казино: vavada – вавада зеркало

The Real Person!

The Real Person!

pin up az: pin up – pin up az

The Real Person!

The Real Person!

пин ап казино: pin up вход – пин ап казино официальный сайт

The Real Person!

The Real Person!

пин ап вход: пин ап казино официальный сайт – пин ап казино официальный сайт

The Real Person!

The Real Person!

pin up az: pin up az – pin up

The Real Person!

The Real Person!

пин ап казино: pin up вход – pin up вход

The Real Person!

The Real Person!

вавада официальный сайт: вавада зеркало – vavada casino

pin up az: pin up casino – pin up casino

вавада: vavada вход – вавада

вавада: vavada casino – vavada

pinup az: pin up az – pin-up

pin-up: pin up az – pin-up

вавада зеркало: vavada casino – vavada

vavada casino: vavada casino – вавада

vavada: вавада официальный сайт – вавада казино

pin-up casino giris: pin-up – pin-up

vavada вход: вавада зеркало – вавада зеркало

вавада официальный сайт: vavada casino – вавада зеркало

The Real Person!

The Real Person!

http://pinupaz.top/# pin up

The Real Person!

The Real Person!

FDA approved generic Cialis: Cialis without prescription – Cialis without prescription

The Real Person!

The Real Person!

buy modafinil online: verified Modafinil vendors – Modafinil for sale

The Real Person!

The Real Person!

modafinil pharmacy: purchase Modafinil without prescription – safe modafinil purchase

The Real Person!

The Real Person!

order Cialis online no prescription: discreet shipping ED pills – buy generic Cialis online

The Real Person!

The Real Person!

same-day Viagra shipping: buy generic Viagra online – legit Viagra online

The Real Person!

The Real Person!

Modafinil for sale: purchase Modafinil without prescription – safe modafinil purchase

The Real Person!

The Real Person!

online Cialis pharmacy: cheap Cialis online – best price Cialis tablets

The Real Person!

The Real Person!

discreet shipping ED pills: FDA approved generic Cialis – affordable ED medication

http://modafinilmd.store/# legal Modafinil purchase

secure checkout ED drugs: best price Cialis tablets – reliable online pharmacy Cialis

The Real Person!

The Real Person!

modafinil 2025: modafinil 2025 – modafinil pharmacy

best price for Viagra: order Viagra discreetly – cheap Viagra online

The Real Person!

The Real Person!

order Viagra discreetly: buy generic Viagra online – trusted Viagra suppliers

modafinil pharmacy: safe modafinil purchase – modafinil legality

The Real Person!

The Real Person!

cheap Viagra online: generic sildenafil 100mg – best price for Viagra

online Cialis pharmacy: best price Cialis tablets – reliable online pharmacy Cialis

The Real Person!

The Real Person!

secure checkout Viagra: discreet shipping – discreet shipping

The Real Person!

The Real Person!

Amo Health Care: Amo Health Care – buy amoxicillin canada

The Real Person!

The Real Person!

buy amoxil: amoxicillin generic – amoxicillin canada price

The Real Person!

The Real Person!

where can i buy clomid without rx: where buy generic clomid online – order cheap clomid without prescription

The Real Person!

The Real Person!

PredniHealth: PredniHealth – prednisone over the counter uk

cialis 40 mg reviews: Tadal Access – generic tadalafil tablet or pill photo or shape

cialis back pain: Tadal Access – cialis over the counter in spain

cialis price cvs: TadalAccess – tadalafil tamsulosin combination

Thanks for sharing. I read many of your blog posts, cool, your blog is very good. https://accounts.binance.com/bn/register?ref=UM6SMJM3

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

http://pharmau24.com/# Licensed online pharmacy AU

get antibiotics without seeing a doctor: best online doctor for antibiotics – buy antibiotics for uti

PharmAu24: Medications online Australia – Online drugstore Australia

best online doctor for antibiotics buy antibiotics online uk Over the counter antibiotics pills

top rated ed pills: Ero Pharm Fast – cheap ed treatment

http://biotpharm.com/# buy antibiotics from canada

Buy medicine online Australia: online pharmacy australia – Pharm Au 24

buy ed pills online: Ero Pharm Fast – Ero Pharm Fast

Discount pharmacy Australia Discount pharmacy Australia online pharmacy australia

https://pharmau24.shop/# Licensed online pharmacy AU

where to get ed pills: buying ed pills online – Ero Pharm Fast

Ero Pharm Fast: Ero Pharm Fast – Ero Pharm Fast

Ero Pharm Fast online ed drugs erectile dysfunction medications online

https://biotpharm.shop/# buy antibiotics from canada

Ero Pharm Fast: buy ed pills online – ed med online

ed meds cheap Ero Pharm Fast Ero Pharm Fast

online pharmacy australia: pharmacy online australia – PharmAu24

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Your article helped me a lot, is there any more related content? Thanks!

After exploring a number of the blog articles on your blog, I truly

appreciate your way of writing a blog. I saved as a favprite it to my bookmark site list and will be checking back iin the near future.

Take a look at mmy website as well and tell me how yoou feel. https://Glassi-App.Blogspot.com/2025/08/how-to-download-glassi-casino-app-for.html