Operational Highlights

Operational Highlights

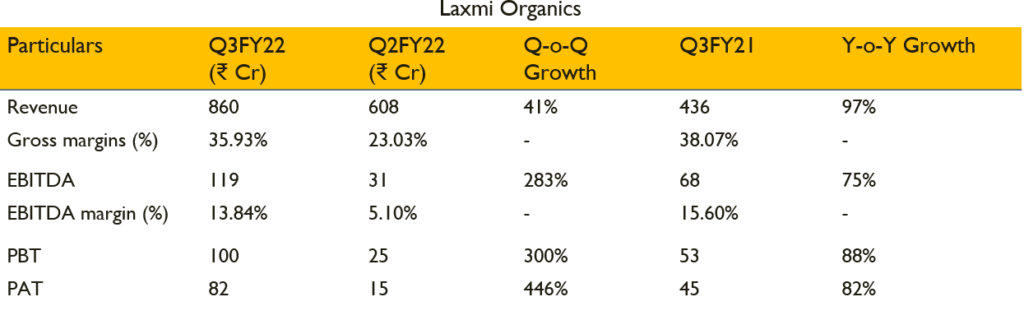

- Revenue from operations stood at ₹860 Cr attributing to growth of 95% YoY

- EBITDA stood at ₹118.7 Cr with EBITDA margins at 14%

- Bounce back from the setback caused due to floods in previous quarter

- Both the business performed strongly

- Import duty on prime raw material “acetic acid” is now reduced from 7.5% to 5% which will have favourable impact on raw material cost

- India is a very small producer of acetic acid and one of the large consumer globally

Segmental review

Specialty intermediates

- Business contributed 30% of the top line.

- The robust performance of speciality intermediates is attributed to ramped up production, following the flood restoration, increased realisations and better product mix optimization towards high value added products

- Exports contribute 30% of SI sales which was less than 10% in previous years

- Raw material prices are correcting and margin visibility is sustainable

- Capacity utilisation at 70% for 9MFY22

Acetyl intermediates

- Business contributed 62% of the top line.

- The strong growth on account of increased realisations and high volumes supported by the subsidiary capacity (Yellowstone Pvt Ltd)

- The prices in the overseas market remain strong through most part of quarter specially in Europe

- volume is growth is sustainable in future, given that the raw material prices correcting and commodity cycles are normalising, expansion in margins could be expected

- Capacity utilisation at 80% for 9MFY22

Capex

- Initial capex was ₹280-₹290 Cr, now it’s reassessed value is ₹450Cr. Part of this incremental cost is time overrun, escalation in cost and significant part of it is increasing infrastructure for capacities of new and existing product

- On track to commercialise speciality intermediates projects and these will start clocking in revenues from Q1FY23

- Decision on launching phase2 capacity of fluoro chemicals to add incremental capacities simultaneously and will commercialise in Q3FY23. Expected turnover from fluorochemicals is ₹280-₹300 Cr

- One in every 3 new APIs will be based on fluorine chemistry

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

https://lioleo.edu.vn/app-dang-ky-thanh-cong/4.png.php?id=bca-bet

Na [Upsports Bet](https://upsportsbet-br.com), novos usuários ganham bônus de US$ 100 ao fazer o cadastro! O login é rápido, e você pode usar o bônus para jogar seus jogos favoritos de cassino. Não perca a chance de começar com uma vantagem extra e aproveite essa oferta incrível.

https://api.lioleo.edu.vn/public/images/skills/4.png.php?id=bet-swagger

Quer começar sua jornada de apostas com um bônus de US$ 100? Na [codbet](https://www.codbet-br.com), você ganha esse bônus exclusivo assim que se registra como novo usuário. A plataforma oferece uma variedade de jogos para você se divertir e, com o bônus, suas chances de vitória ficam ainda maiores!

O suporte ao cliente da [pinnacle](https://pinnacle-br.com) é excelente, oferecendo atendimento profissional 24/7. Se surgir qualquer dúvida ou problema, a equipe está disponível para resolver de forma eficiente e ágil, para que sua experiência de jogo seja tranquila e sem interrupções.

Como Baixar o Aplicativo pixbet e Aproveitar a Melhoria na Interface e Experiência de Jogo

Na [umbet](https://um-bet-br.com), Bônus e Jogos de Azar Populares Garantem uma Experiência de Cassino Imbatível

What You Need to Know About Withdrawing Funds from wish – https://wish-ph.com

Como Baixar e Instalar o Aplicativo [Upsports Bet](https://upsportsbet-br.com) e Transformar Sua Experiência de Jogo Online

แอป z97 – https://awmd4.com อัปเดตระบบฝาก-ถอนให้รวดเร็วขึ้น รองรับธนาคารไทยและ e-wallet ชั้นนำ

I appreciate the level of detail in this post. It really helped me get a better understanding of the subject.

เล่นบาคาร่า รูเล็ต และเกมไพ่อื่นๆ ผ่านแอป kc988 – https://irt55.com ด้วยระบบที่ลื่นไหลและภาพคมชัดระดับ HD

kubet – https://kubet-vn.com – Trải Nghiệm Cờ Bạc Công Bằng Và Tiền Thưởng Hấp Dẫn

สมัครสมาชิกผ่านแอป y8 – https://hqus2.com วันนี้ รับสิทธิ์เข้าร่วมโปรโมชั่นพิเศษที่มีเฉพาะบนมือถือ

Write more, thats all I have to say. Literally, it seems as though you relied on the video to make your point.

You clearly know what youre talking about, why throw away your intelligence on just posting videos to your blog when you could be giving us something informative to

read?

I know this web page presents quality dependent articles and additional data, is there any other web

page which offers these kinds of information in quality?

Withdraw Your Winnings with Ease: supernova’s Secure and Quick Withdrawal Process

Ganhe 100$ ao se Registrar no dicasbet e Aposte de Forma Fácil!

lion เกมพนันที่ได้รับความนิยม พร้อมโบนัสสุดคุ้มสำหรับลูกค้าใหม่

z16 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

ดาวน์โหลดแอป w69 วันนี้ รับโปรโมชั่นพิเศษมากมาย ใช้งานสะดวก

ปลอดภัย และรองรับทุกอุปกรณ์

w69 login วันนี้ รับโปรโมชั่นพิเศษมากมาย ใช้งานสะดวก ปลอดภัย และรองรับทุกอุปกรณ์

เล่นสล็อตแนว Adventure กับธีม Tomb Raider และ Uncharted ได้ที่แอป www w69 – https://tsc97.com พร้อมโบนัสหมุนฟรีสำหรับสมาชิกใหม่ ออกล่าสมบัติและสะสมรางวัลใหญ่ไปกับการผจญภัยที่ไม่มีที่สิ้นสุด

Join mrrex Today: Register and

Receive a $100 Bonus Immediately!

เพลิดเพลินกับเกมคาสิโนออนไลน์ในแอป

w69 ทางเข้า – https://rwho3 ที่มาพร้อมระบบภาพและเสียงระดับ HD เพื่อประสบการณ์ที่เหนือกว่า

สมัครสมาชิกผ่านแอป w69 com รับโบนัสต้อนรับ 100$ และสิทธิพิเศษอีกมากมาย

สมัครสมาชิกผ่านแอป

สล็อต w69 เว็บตรง รับโบนัสต้อนรับ 100$ และสิทธิพิเศษอีกมากมาย

venus-bet

bakmi-bet

bet-bantara

http://magdalenahoffmann.com/br/index.php?id=rokok-bet

asia-bet-king

http://hornoscasaemilio-valoriani.com/br/index.php?id=mandiri-bet

http://xn--l1acbdfo1f.xn--p1ai/br/index.php?id=sumatera-bet

http://pribehyfotek.cz/br/index.php?id=free-bet-slot

http://site2.aesa.pb.gov.br/aesa/Sports/?id=bet-artinya

http://site2.aesa.pb.gov.br/aesa/Sports/?id=ayu-bet-slot

https://gvis.tramandai.rs.gov.br/web-console/Lifestyle/?id=topan-bet

http://hornoscasaemilio-valoriani.com/br/index.php?id=gg-bet

http://pribehyfotek.cz/br/index.php?id=bet-slot

https://gvis.tramandai.rs.gov.br/web-console/Sports/?id=777-bet

ดาวน์โหลดแอป เว็บw69 – https://abtl8.com แล้วสนุกกับระบบแจ็คพอตที่อิงจากเกม The Witcher และ The Elder Scrolls รับรางวัลสูงสุดทุกสัปดาห์

http://sila-zerna.com/br/index.php?id=bakmi-bet

http://xn--l1acbdfo1f.xn--p1ai/br/index.php?id=bet-cash

buah-bet

http://hydraulik-tuchola.pl/br/index.php?id=bet-artinya

http://mail.crn-nieruchomosci.pl/br/index.php?id=bet-10-ribu

http://magdalenahoffmann.com/br/index.php?id=hijau-bet-777

ww88 แจกโบนัส 100$ สำหรับสมาชิกใหม่ เพียงลงทะเบียน

ygg สมัครใหม่ รับโบนัส 100$ ไม่ต้องฝาก

rauy ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว

โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย

ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด

ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

หลังจากที่ผู้ใช้ทำการลงทะเบียนแล้ว สามารถเข้าสู่ระบบได้โดยการใช้ชื่อผู้ใช้และรหัสผ่านที่ได้ตั้งไว้ในขั้นตอนการสมัคร

เมื่อเข้าสู่ระบบเรียบร้อยแล้ว ผู้เล่นสามารถเข้าถึงเกมคาสิโนออนไลน์ที่หลากหลาย ไม่ว่าจะเป็นสล็อต

คาสิโนสด หรือกีฬา และยังสามารถใช้โปรโมชั่นและโบนัสที่มีให้แก่ผู้ใช้ใหม่ได้ทันที

ติดตั้งแอป w69สล็อต เครดิตฟรี – https://apmb1.com เพื่อสนุกกับการสตรีมสดการแข่ง eSports พร้อมตัวเลือกเดิมพันอัจฉริยะในเกม Rainbow Six และ Overwatch ทายผลการแข่งขันและรับโบนัสเมื่อทีมโปรดของคุณชนะ

http://www.hydraulik-tuchola.pl/br/index.php?id=888-bet-login

m358 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

jbo แจกโบนัสฟรี 100$ เพียงสมัครสมาชิกใหม่

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ pg123 ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด อีเมล หรือสายด่วน

เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

ขั้นตอนสมัคร me88 และรับสิทธิ์โบนัส 100$ สำหรับผู้เล่นใหม่

1xbet – https://1xbet-778.com พร้อมให้บริการลูกค้าทุกวัน ตลอด 24 ชั่วโมง แก้ไขข้อสงสัยทันที

หลังจากที่ผู้ใช้ทำการลงทะเบียนแล้ว สามารถเข้าสู่ระบบได้โดยการใช้ชื่อผู้ใช้และรหัสผ่านที่ได้ตั้งไว้ในขั้นตอนการสมัคร เมื่อเข้าสู่ระบบเรียบร้อยแล้ว ผู้เล่นสามารถเข้าถึงเกมคาสิโนออนไลน์ที่หลากหลาย ไม่ว่าจะเป็นสล็อต คาสิโนสด หรือกีฬา และยังสามารถใช้โปรโมชั่นและโบนัสที่มีให้แก่ผู้ใช้ใหม่ได้ทันที

ojo ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น

การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ

เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด

การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ kc9

ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด อีเมล หรือสายด่วน เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ u31

ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด อีเมล

หรือสายด่วน เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ joker ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ

ไม่ว่าจะเป็นแชทสด อีเมล หรือสายด่วน

เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

ruay ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ

ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24

ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

188bet ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ

เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด

ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

lava ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด

ซึ่งมักใช้เวลาไม่เกิน 24

ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

บริการลูกค้าระดับมืออาชีพ m98 – https://m98-888.com ตอบคำถามทุกข้อสงสัยทันที

lotto ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ

ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets

ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน

จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24

ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

บริการลูกค้าระดับมืออาชีพ sexy –

https://sexy-778.com ตอบคำถามทุกข้อสงสัยทันที

hulk – https://hulk-th.com บริการลูกค้ามืออาชีพ แก้ไขปัญหาผู้เล่น 24/7

fun88 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets

ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน

จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24

ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

pg168 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด

ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

123bet – https://123bet-888.com พร้อมให้คำแนะนำตลอด

24 ชั่วโมง บริการลูกค้าระดับมืออาชีพ

h25 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets

ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

365bet ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ 22win ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ

ไม่ว่าจะเป็นแชทสด อีเมล

หรือสายด่วน เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

สมัครสมาชิก pxj

วันนี้ รับโบนัสฟรี 100$

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ

ทีมบริการลูกค้าของ 12bet ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด อีเมล หรือสายด่วน เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

mthai ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

win88 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ

ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets ที่ได้รับความนิยมในปัจจุบัน

ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน

จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

หลังจากที่ผู้ใช้ทำการลงทะเบียนแล้ว สามารถเข้าสู่ระบบได้โดยการใช้ชื่อผู้ใช้และรหัสผ่านที่ได้ตั้งไว้ในขั้นตอนการสมัคร เมื่อเข้าสู่ระบบเรียบร้อยแล้ว ผู้เล่นสามารถเข้าถึงเกมคาสิโนออนไลน์ที่หลากหลาย ไม่ว่าจะเป็นสล็อต คาสิโนสด หรือกีฬา และยังสามารถใช้โปรโมชั่นและโบนัสที่มีให้แก่ผู้ใช้ใหม่ได้ทันที

ff88 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ

e-wallets ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

w88 ให้ความสำคัญกับการถอนเงินของผู้ใช้เพื่อให้สมาชิกสามารถทำธุรกรรมได้อย่างสะดวกและรวดเร็ว โดยเว็บไซต์มีวิธีการถอนเงินที่ง่ายและปลอดภัย ผู้เล่นสามารถถอนเงินได้ผ่านช่องทางต่างๆ ที่รองรับ เช่น การโอนเงินผ่านธนาคาร หรือการใช้บริการ e-wallets

ที่ได้รับความนิยมในปัจจุบัน ขั้นตอนการถอนเงินทำได้ง่ายๆ เพียงเข้าสู่ระบบ เลือกเมนูการถอนเงิน จากนั้นกรอกจำนวนเงินที่ต้องการถอนและเลือกวิธีการที่สะดวกที่สุด การถอนเงินจะดำเนินการโดยอัตโนมัติภายในระยะเวลาที่กำหนด ซึ่งมักใช้เวลาไม่เกิน 24 ชั่วโมง ขึ้นอยู่กับวิธีการถอนที่เลือก

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ jbl ก็พร้อมให้บริการตลอด

24 ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด อีเมล หรือสายด่วน

เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

หลังจากที่ผู้ใช้ทำการลงทะเบียนแล้ว สามารถเข้าสู่ระบบได้โดยการใช้ชื่อผู้ใช้และรหัสผ่านที่ได้ตั้งไว้ในขั้นตอนการสมัคร เมื่อเข้าสู่ระบบเรียบร้อยแล้ว ผู้เล่นสามารถเข้าถึงเกมคาสิโนออนไลน์ที่หลากหลาย ไม่ว่าจะเป็นสล็อต คาสิโนสด

หรือกีฬา และยังสามารถใช้โปรโมชั่นและโบนัสที่มีให้แก่ผู้ใช้ใหม่ได้ทันที

fan88 สมัครสมาชิกใหม่ รับโบนัส 100$ ทันที ไม่มีเงื่อนไข

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ uea8 ก็พร้อมให้บริการตลอด 24 ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด อีเมล หรือสายด่วน เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

หากผู้เล่นประสบปัญหาในการลงทะเบียนหรือการเข้าสู่ระบบ ทีมบริการลูกค้าของ fm99 ก็พร้อมให้บริการตลอด 24

ชั่วโมงผ่านช่องทางต่างๆ ไม่ว่าจะเป็นแชทสด

อีเมล หรือสายด่วน เพื่อให้ผู้เล่นได้รับความช่วยเหลืออย่างรวดเร็วและมีประสิทธิภาพ

bookmarked!!, I like your blog!

It’s very easy to find out any topic on web as compared to books, as I found this post at this web page.

100$ de Bônus no f12bet para Novos Usuários – Registre-se!

Faça Seu Cadastro no allwin e Ganhe 100$ de Bônus Exclusivo!

No dobrowin, novos usuários podem aproveitar um bônus de 100$ ao se registrar no site!

Isso significa mais chances de ganhar e explorar uma grande variedade de jogos de cassino, desde slots emocionantes até clássicos como roleta e blackjack.

Com o bônus de boas-vindas, você começa com um saldo

extra, o que aumenta suas chances de sucesso.

Cadastre-se agora e use os 100$ de bônus para experimentar

seus jogos favoritos com mais facilidade. Aproveite a

oferta e comece sua aventura no cassino agora mesmo!

100$ de Bônus no jogos win para Novos Usuários – Registre-se!

No iribet,

novos usuários podem aproveitar um bônus de 100$ ao se registrar no site!

Isso significa mais chances de ganhar e explorar uma grande

variedade de jogos de cassino, desde slots emocionantes até clássicos como roleta e blackjack.

Com o bônus de boas-vindas, você começa com um saldo extra, o que aumenta suas chances de sucesso.

Cadastre-se agora e use os 100$ de bônus para experimentar

seus jogos favoritos com mais facilidade. Aproveite a oferta e comece sua aventura no cassino agora mesmo!

Faça Seu Cadastro no bet7k e Ganhe 100$ de Bônus Agora Mesmo!

Aproveite a oferta exclusiva do pgwin (https://www.pgwin-br.com) para novos usuários e receba 100$ de bônus ao se registrar!

Este bônus de boas-vindas permite que você experimente uma vasta gama de jogos de cassino online sem precisar gastar imediatamente.

Com o bônus de 100$, você poderá explorar jogos como roleta, blackjack, caça-níqueis e muito mais, aumentando suas chances de vitória desde o primeiro minuto.

Não perca essa chance única de começar com um valor significativo – cadastre-se agora!

Seu Bônus de 100$ Espera por Você no aajogo

– Cadastre-se Agora!

100$ de Bônus para Apostar no stake!

Cadastre-se Agora!

100$ de Bônus para Apostar no dobrowin!

Cadastre-se Agora!

Registre-se no onebra – https://onebra-br.com Agora e Receba 100$ para Suas Apostas!

Welcome to mrbit!

New users receive a $100 bonus upon registration. The process is straightforward: create your account,

log in, and your bonus will be instantly credited. This offer is designed to give new players a

head start. With your $100 bonus, you can enjoy a variety

of games, including slots, poker, and more.

Don’t miss out on this fantastic opportunity to maximize your gaming experience.

Register today and grab your bonus!

Welcome to gamdom! New

users receive a $100 bonus upon registration. The process is straightforward: create

your account, log in, and your bonus will be instantly credited.

This offer is designed to give new players a head start.

With your $100 bonus, you can enjoy a variety of games,

including slots, poker, and more. Don’t miss out on this fantastic opportunity to maximize your gaming experience.

Register today and grab your bonus!

Join mrplay Now and Claim Your $100 Bonus in Just a

Few Steps!

Ready to play on oppa888?

New users can receive a $100 bonus upon registration! Simply create an account,

log in, and the bonus will be automatically

credited to your account. This is the perfect way to get started with extra funds,

giving you the chance to explore a wide variety of casino games.

Don’t wait – register now and claim your $100 bonus today!

New Users Get $100 Free at yako – Claim Yours

Today!

Looking for an online casino that rewards new players right from the start?

lottoland has you covered!

Register now and receive a $100 bonus to explore all the games you love.

Whether it’s poker, live casino games, or sports betting, your

bonus will give you the boost you need to maximize your chances of

winning. Sign up now and take advantage of this limited-time offer—your $100 bonus is waiting!

Sign Up on nextbet Today – New Users Get

a $100 Bonus!

Join nyspins Now and Claim

Your $100 Bonus in Just a Few Steps!

Join comeon Now and Get Your $100

Registration Bonus!

Unlock Your $100 Bonus by Registering on casigo Today

Looking for an online casino with exciting rewards?

At satsport, new users

can enjoy a $100 bonus just for registering! With this bonus, you’ll be

able to explore a wide range of games, including slots, poker, blackjack,

and more. Don’t miss out on this exclusive offer—sign up now and claim your $100 bonus to get your

gaming experience off to a fantastic start!

Register on 12bet and Enjoy an Exclusive $100 Bonus

for New Users!

betfury Sign-Up Guide: Get Your $100 Bonus Upon Registration!

Welcome to heyspin!

New users receive a $100 bonus upon registration. The process

is straightforward: create your account, log in, and your bonus will be instantly credited.

This offer is designed to give new players a head start.

With your $100 bonus, you can enjoy a variety of games, including slots, poker,

and more. Don’t miss out on this fantastic opportunity to maximize your gaming experience.

Register today and grab your bonus!

How to Register and Get Your $100 Bonus at bons

Get a head start at dreamz with

a $100 bonus for new users! By signing up today, you’ll instantly receive this bonus to use across a wide range of games.

Whether you’re interested in poker, slots, or sports betting, this bonus

will help you maximize your chances of success.

Don’t miss out on this exclusive offer—register now and

claim your $100 bonus to get your gaming adventure started!

Create an Account on rant and Start Playing with a $100 Bonus!

Ready to play on goslot?

New users can receive a $100 bonus upon registration! Simply create an account, log in, and the bonus will be automatically credited to your account.

This is the perfect way to get started with extra

funds, giving you the chance to explore a wide variety of casino

games. Don’t wait – register now and claim your $100

bonus today!

Get Your $100 Bonus When You Register at casumo Today!

Sign Up for leonbet and Claim Your $100 Bonus Instantly!

Sign up on pinnacle and enjoy a $100 bonus right after registration.

It’s simple to register: just fill in your details,

log in, and the bonus will be yours. Whether you’re new to online casinos or an experienced

player, the $100 bonus will enhance your experience and give

you more chances to win. Don’t miss out on this special offer – register now

and claim your bonus today!

How to Register on w88 and Start Playing with $100 Bonus

Get a $100 Head Start with bluechip – Sign Up Today!

Sign up on bilbet and enjoy a

$100 bonus right after registration. It’s simple to register: just fill in your details, log in, and the

bonus will be yours. Whether you’re new to online casinos or an experienced player, the $100 bonus will enhance your

experience and give you more chances to win. Don’t miss out on this special offer – register now and claim your bonus

today!

Unlock a world of gaming with national’s $100 bonus for new users!

When you register, you’ll get this bonus to use across the platform’s wide range

of games, including poker, slots, blackjack, and more.

Take advantage of this amazing offer and sign up now to start playing your favorite casino games with a

$100 bonus!

Get started at sbobet

with a $100 bonus just for signing up! It’s easy

to register, and once you log in, your $100 bonus will be ready for

you. This bonus is perfect for new users who want to make the

most of their casino experience. Sign up now and enjoy your bonus right away!

Looking for an online casino that rewards new players right from the

start? buumi has you covered!

Register now and receive a $100 bonus to explore all the games you love.

Whether it’s poker, live casino games, or sports betting, your bonus will give

you the boost you need to maximize your chances of winning.

Sign up now and take advantage of this limited-time offer—your $100 bonus is waiting!

Join tsars and Start

Your Journey with a $100 Welcome Bonus!

Join 24bet Today and Claim Your $100 Welcome Bonus!

Get Your $100 Bonus When You Register at netbet Today!

Sign Up at slotv and Enjoy a $100 Registration Bonus

O bet 4 oferece uma excelente oportunidade para quem deseja começar sua experiência no cassino online com um

bônus de 100$ para novos jogadores! Ao se registrar no site, você garante

esse bônus exclusivo que pode ser utilizado em diversos jogos de

cassino, como slots, roleta e poker. Esse é

o momento perfeito para explorar o mundo das apostas

com um saldo extra, aproveitando ao máximo suas apostas sem precisar investir um

grande valor logo de início. Não perca essa oportunidade e cadastre-se já!

O bet77 oferece uma excelente

oportunidade para quem deseja começar sua experiência no cassino online com um bônus de 100$

para novos jogadores! Ao se registrar no site, você garante esse

bônus exclusivo que pode ser utilizado em diversos jogos de cassino, como slots, roleta

e poker. Esse é o momento perfeito para explorar o mundo das apostas com um saldo

extra, aproveitando ao máximo suas apostas sem precisar

investir um grande valor logo de início. Não perca essa oportunidade e cadastre-se já!

Ao se cadastrar no 580bet,

você ganha um bônus de 100$ para começar sua jornada

no cassino com o pé direito! Não importa se você é um novato

ou um apostador experiente, o bônus de boas-vindas é

a oportunidade perfeita para explorar todas as opções que o site tem a oferecer.

Jogue seus jogos favoritos, descubra novas opções de apostas e aproveite para testar estratégias sem risco, já que o bônus ajuda a aumentar suas chances de ganhar.

Cadastre-se hoje e comece com 100$!

No bet 7k, novos usuários podem aproveitar um bônus de 100$ ao se registrar

no site! Isso significa mais chances de ganhar e explorar uma grande variedade de jogos de cassino, desde slots emocionantes até clássicos

como roleta e blackjack. Com o bônus de boas-vindas, você começa com um saldo extra, o que aumenta

suas chances de sucesso. Cadastre-se agora e use os 100$ de bônus

para experimentar seus jogos favoritos com mais facilidade.

Aproveite a oferta e comece sua aventura no cassino agora mesmo!

Bônus de 100$ ao Registrar-se no allwin

– Comece a Apostar Já!

lvbet: 100$ de Bônus para Novos Jogadores – Cadastre-se Já!

Ao se cadastrar no 7kbet, você ganha um bônus de 100$ para

começar sua jornada no cassino com o pé direito!

Não importa se você é um novato ou um apostador experiente, o bônus de boas-vindas é a oportunidade perfeita para explorar todas as opções

que o site tem a oferecer. Jogue seus jogos favoritos, descubra novas opções de apostas

e aproveite para testar estratégias sem risco, já que o bônus ajuda

a aumentar suas chances de ganhar. Cadastre-se hoje e comece com 100$!

Como se Registrar no luck 2 – https://luck-2.com e Obter 100$

de Bônus de Boas-Vindas!

Bônus de 100$ ao Registrar-se no leao – Comece

a Apostar Já!

Faça Seu Cadastro no betpix e Ganhe 100$ de Bônus Agora Mesmo!

Cadastre-se no f12bet e Ganhe

100$ para Apostar!

Como se Registrar no b1bet – https://b1-bet-br.com e Obter

100$ de Bônus de Boas-Vindas!

Ao se cadastrar no 9d bet, você ganha um bônus de 100$ para começar sua jornada no cassino com o

pé direito! Não importa se você é um novato ou um apostador experiente, o bônus de boas-vindas é a oportunidade perfeita para

explorar todas as opções que o site tem a oferecer.

Jogue seus jogos favoritos, descubra novas opções

de apostas e aproveite para testar estratégias sem risco, já que o bônus ajuda a aumentar suas chances de ganhar.

Cadastre-se hoje e comece com 100$!

No ktobet, ao Registrar-se,

Você Recebe 100$ de Bônus!

100$ de Bônus para Apostar no fbbet!

Cadastre-se Agora!

No batbet, ao Registrar-se, Você Recebe 100$

de Bônus!

Comece no 20bet com 100$ de Bônus de Boas-Vindas!

Claim Your $100 Bonus When You Register on nn777 Today!

No fazobetai, ao Registrar-se, Você Recebe 100$ de Bônus!

Đăng Ký zowin – Nhận Ngay 100$ Khi Gửi

Tiền Lần Đầu

Cách Đăng Ký Tài Khoản win2888 Nhanh Chóng Chỉ Trong 3 Phút

No globalbet, Você Começa

com 100$ de Bônus Exclusivo!

Ganhe 100$ de Bônus ao Se Registrar no doce888 – https://doce888-br.com –

Cadastre-se Agora!

No luck (luckbet-br.com), Você Começa com 100$ de Bônus

ao se Registrar!

Ganhe 100$ para Apostar no bet favorita ao Se Registrar Hoje!

Aproveite 100$ de Bônus no simplesbet ao Criar Sua Conta!

Bônus de 100$ no goinbet – https://www.goinbet-br.com: Faça Seu Cadastro Agora Mesmo!

Registre-se no betsul – https://betsul-88.com e Comece a

Apostar com 100$ de Bônus!

Ao se cadastrar no onebra, você ganha um

bônus de 100$ para começar sua jornada no cassino com o pé direito!

Não importa se você é um novato ou um apostador experiente, o bônus de boas-vindas

é a oportunidade perfeita para explorar todas as opções que o site tem a oferecer.

Jogue seus jogos favoritos, descubra novas opções de apostas e aproveite para

testar estratégias sem risco, já que o bônus ajuda a aumentar suas chances de ganhar.

Cadastre-se hoje e comece com 100$!

Very nice post. I just stumbled upon your weblog and wanted to say that I’ve truly loved surfing around your weblog posts. After all I will be subscribing for your feed and I am hoping you write again soon!

Bônus de 100$ no brdice – https://brdice-br.com: Faça Seu Cadastro

Agora Mesmo!

Receba 100$ ao Criar Sua Conta no wingdus – Bônus Exclusivo!

allwin568: Comece com

100$ de Bônus ao Criar Sua Conta!

No queens, novos usuários podem aproveitar um bônus de 100$ ao se registrar no site!

Isso significa mais chances de ganhar e explorar uma grande

variedade de jogos de cassino, desde slots emocionantes

até clássicos como roleta e blackjack. Com o bônus de boas-vindas,

você começa com um saldo extra, o que aumenta suas

chances de sucesso. Cadastre-se agora e use os 100$ de bônus para experimentar seus jogos

favoritos com mais facilidade. Aproveite a oferta e comece sua aventura no cassino agora mesmo!

Registre-se e Receba 100$ de Bônus no esoccer bet para

Apostar!

O betestrela oferece uma excelente oportunidade para quem

deseja começar sua experiência no cassino online com um bônus de 100$ para novos jogadores!

Ao se registrar no site, você garante esse bônus exclusivo que pode ser utilizado em diversos jogos de cassino, como slots, roleta e poker.

Esse é o momento perfeito para explorar o mundo das apostas com um saldo extra,

aproveitando ao máximo suas apostas sem precisar

investir um grande valor logo de início. Não perca essa oportunidade

e cadastre-se já!

Como se Registrar no winbrl – https://winbrl-88.com e Obter 100$ de Bônus de Boas-Vindas!

Faça Seu Cadastro no cbet e Ganhe 100$ de

Bônus Agora Mesmo!

Faça Seu Registro no bet7 – https://bet7-88.com e Ganhe 100$ de Bônus Exclusivo!

Aproveite a oferta exclusiva do 667bet para

novos usuários e receba 100$ de bônus ao se registrar!

Este bônus de boas-vindas permite que você experimente uma vasta gama de jogos

de cassino online sem precisar gastar imediatamente. Com o bônus de

100$, você poderá explorar jogos como roleta, blackjack, caça-níqueis e muito mais, aumentando suas chances de vitória desde o primeiro minuto.

Não perca essa chance única de começar com

um valor significativo – cadastre-se agora!

O bet nacional oferece uma excelente oportunidade para quem deseja começar sua experiência no

cassino online com um bônus de 100$ para novos jogadores!

Ao se registrar no site, você garante esse bônus exclusivo que pode ser utilizado em diversos jogos

de cassino, como slots, roleta e poker.

Esse é o momento perfeito para explorar o mundo das apostas

com um saldo extra, aproveitando ao máximo suas

apostas sem precisar investir um grande valor logo de início.

Não perca essa oportunidade e cadastre-se já!

Ao se cadastrar no pagbet, você ganha um bônus de 100$

para começar sua jornada no cassino com o pé direito! Não importa se você é um novato ou um apostador

experiente, o bônus de boas-vindas é a oportunidade perfeita para explorar todas as opções

que o site tem a oferecer. Jogue seus jogos favoritos, descubra novas opções de apostas e aproveite para testar estratégias sem risco,

já que o bônus ajuda a aumentar suas chances de ganhar.

Cadastre-se hoje e comece com 100$!

Registre-se e Receba 100$ de Bônus no queens para Apostar!

curso beta: Cadastre-se e Ganhe 100$ de Bônus para Apostar!

100$ de Bônus no 939 bet – https://939-bet-br.com: Registre-se Agora e Aproveite a Oferta!

Novo no bkbet – https://bk-bet-com.com? Cadastre-se e Receba 100$ de Bônus ao Fazer Login!

O aajogo oferece uma

excelente oportunidade para quem deseja começar sua experiência no cassino online com um bônus

de 100$ para novos jogadores! Ao se registrar no site,

você garante esse bônus exclusivo que pode ser utilizado em

diversos jogos de cassino, como slots, roleta e poker.

Esse é o momento perfeito para explorar o mundo das apostas com um saldo extra, aproveitando ao máximo suas apostas sem

precisar investir um grande valor logo de início.

Não perca essa oportunidade e cadastre-se já!

Faça Seu Cadastro no gbg bet e Ganhe 100$ de Bônus Agora Mesmo!

O abc bet oferece uma excelente oportunidade

para quem deseja começar sua experiência no cassino online com um bônus de 100$ para novos jogadores!

Ao se registrar no site, você garante esse bônus exclusivo que pode

ser utilizado em diversos jogos de cassino, como slots, roleta

e poker. Esse é o momento perfeito para explorar o mundo das apostas com um saldo extra, aproveitando ao máximo

suas apostas sem precisar investir um grande valor logo de início.

Não perca essa oportunidade e cadastre-se já!

Aproveite a oferta exclusiva do brl bet para novos usuários e receba 100$ de bônus ao se registrar!

Este bônus de boas-vindas permite que você experimente

uma vasta gama de jogos de cassino online sem precisar gastar

imediatamente. Com o bônus de 100$, você poderá explorar

jogos como roleta, blackjack, caça-níqueis e muito mais, aumentando suas chances

de vitória desde o primeiro minuto. Não perca essa chance única de começar com um valor significativo – cadastre-se agora!

casadeapostas: Cadastre-se

e Ganhe 100$ de Bônus para Apostar!

Thanks for the tips!

Novo no pixbet?

Ganhe 100$ de Bônus Ao Se Registrar!

This is exactly what I was looking for. Visit https://580-bet.com to explore more on this topic.

premiação copa do brasil -(https://yfsy30pd.com)

Bônus de 100$ para Novos Jogadores no betway –

Cadastre-se Agora!

Ao se cadastrar no seubet, você ganha um bônus de 100$ para começar sua

jornada no cassino com o pé direito! Não importa se você

é um novato ou um apostador experiente, o bônus de

boas-vindas é a oportunidade perfeita para explorar todas as opções que o site tem a oferecer.

Jogue seus jogos favoritos, descubra novas opções

de apostas e aproveite para testar estratégias sem risco, já que o bônus ajuda a aumentar

suas chances de ganhar. Cadastre-se hoje e

comece com 100$!

Ganhe no Cassino Online jogodeouro: Diversão e Vitória!

Ganhe Agora com os Jogos do Cassino nine casino!

Jogue e Ganhe com Facilidade no Cassino upsports bet!

Ganhe no bet estrela – Diversão e Grandes

Prêmios!

Cassino esportenet bet:

Jogue Agora e Conquiste Grandes Vitórias!

Aposte e Ganhe no Cassino jogos win Agora!

Ganhe no Cassino Online winzada 777:

Diversão e Vitória!

Ganhe Grande com os Jogos Mais Populares no luck!

Ganhe Grande no Cassino curso beta

com Jogos Populares!

Aposte no Cassino lendas bet e Ganhe Grande!

Aposte e Ganhe Rápido com Jogos Populares no bet 558!

Ganhe Prêmios Incríveis com Jogos Populares no Cassino spins on!

Ganhe Rápido com os Jogos Populares do Cassino 7 games!

bk bet com: Aposte Agora e Conquiste Grandes Vitórias!

Ganhe Prêmios Fáceis no Cassino Online 8800 bet!

Ganhe Agora com os Jogos do Cassino premier bet!

Cassino sao jorge bets: Onde Você Pode Ganhar Facilmente!

7755 bet: Apostas Fáceis, Grandes Vitórias!

Aposte e Vença no Cassino imperador bet – Jogue e Ganhe!

Ganhe Facilmente com os Jogos do Cassino 333 bet!

multicanais bet: Onde Você Joga e Ganha Com Facilidade!

TM

Aposte Agora e Conquiste Vitórias no Cassino mesk bet!

Aposte no Cassino izzi casino e Ganhe Grande!

Jogue e Vença Agora no royale – Cassino Online Fácil!

Ganhe no Cassino Online simples bet com Jogos Simples e Populares!

4 play bet: Onde a

Sorte Encontra os Melhores Jogadores!

seguro bet: Vença com

Jogos Populares e Rápidos!

Ganhe Agora nos Jogos Populares do Cassino 7 games bet!

jack bet: Jogue e Ganhe com Prêmios Instantâneos!

Ganhe Dinheiro Fácil nos Jogos do Cassino 1993 bet!

Cassino Online 193 bet:

Onde Você Sempre Pode Ganhar!

Cassino bet4: O Melhor Lugar para Apostar e Ganhar!

Jogue no 136 bet e Ganhe com Simplicidade!

Jogue e Ganhe no Cassino 3y casino – Simples e Rápido!

Ganhe no Cassino kto casino

com Jogos Populares e Fáceis!

bet dasorte:

Onde Jogos Populares Levam à Vitória!

Aposte e Ganhe no Cassino 667 bet – Diversão Garantida!

Aposte e Ganhe Rápido com Jogos Populares no ir6 bet!

Cassino bet sporting: Vença com Jogos Populares

e Simples!

Aposte e Vença no Cassino bgg bet – Jogue e Ganhe!

Jogue no Cassino wj casino e Ganhe de Forma Simples

e Rápida!

Jogos Populares do Cassino bet casino

para Você Ganhar!

Ganhe no Cassino qqq bet com Jogos Populares e

Simples!

Cassino 1win casino:

Jogue Agora e Conquiste Grandes Vitórias!

Jogue no Cassino abc bet e Ganhe Prêmios Instantâneos!

Ganhe no geral bet com Facilidade nos Jogos Populares!

Experimente o Cassino oba bet e Ganhe com Jogos Populares!

Aposte e Ganhe Grandes Prêmios no 7k bet!

Aposte no Cassino aviator aposta e Ganhe

Prêmios Fantásticos!

Experimente o Cassino zeroum bet e Ganhe com Jogos

Populares!

Ganhe Rápido e Fácil no Cassino Online 522 bet!

Jogos Populares e Grandes Oportunidades no Cassino bons casino!

Jogue no 74 bet e

Ganhe com Facilidade nos Jogos Populares!

Aposte e Ganhe no wild bet – Apostas Populares!

Você sabia que a futebol ao vivo hd oferece uma das maneiras

mais seguras de retirar seus fundos online? Só enviar

seus documentos básicos.

Para retirar dinheiro da futebol ao vivo in,

tudo o que você precisa fazer é enviar o seu CPF e um comprovante de residência.

Rápido e fácil!

futebol ao vivo gr谩tis: Como Realizar

Saques Rápidos com Documentação Apropriada

Saque na futebol rei ao vivo: Como Garantir que

Seus Ganhos Cheguem Rápido à Sua Conta

futemax futebol ao vivo: Como Obter Seu Dinheiro Rápido com

Documentação Correta

Como Retirar Seus Fundos da app futebol ao vivo gr谩tis de Forma Segura e Eficiente

Saques rápidos, sem complicação, e com total segurança.

Tudo o que você precisa fazer é enviar os documentos corretos para a futebol ao vivo g1.

Passo a Passo de Como Retirar Seus Ganhos na futebol play hd ao vivo

com Facilidade

Como Retirar Ganhos na resultado ao vivo futebol com Agilidade e

Segurança

Guia Completo de Saque: Como Evitar Complicações na futebol ao vivo vasco

Como Retirar Ganhos na futebol ao vivo resultados com Agilidade e Segurança

Com a youtube futebol ao vivo, você tem a garantia de

que seus saques serão processados rapidamente, desde

que você forneça os documentos solicitados.

Na jogo futebol ao vivo, seu saque é tratado com a máxima

prioridade, desde que você forneça os documentos necessários.

Sem complicação!

Saques na futebol na tv ao vivo hoje:

Como Tornar o Processo Simples e Seguro

Para retirar dinheiro na resultados ao vivo futebol, tudo o

que você precisa fazer é enviar alguns documentos simples, e pronto!

O processo de retirada na assitir futebol ao vivo é muito simples.

Basta enviar os documentos solicitados e a plataforma processa rapidamente seu saque.

A sites de futebol ao vivo Protege Seu

Dinheiro: Descubra Como Garantimos Saques Sem Riscos

Como Retirar Seus Fundos na app de futebol ao vivo: Dicas Para

um Processo Rápido e Seguro

Retirando Dinheiro da futebol hoje ao vivo na tv:

Como Garantir que Seu Saque Seja Rápido e Seguro

Como Realizar Saques na futebol ao vivo cruzeiro com Facilidade e Segurança

Como Retirar Ganhos na globo play ao vivo futebol com Agilidade e Segurança

A rmc futebol ao vivo oferece um sistema de saque eficiente, permitindo que você retire seus ganhos com facilidade

e segurança.

Como Retirar Ganhos na futmax futebol ao vivo com Agilidade

e Segurança

Guia Completo Para Retirar Seus Fundos na futebol ao vivo em hd de Forma Segura

A placar futebol ao vivo

oferece um processo de saque simples e rápido. Basta fornecer os documentos exigidos e seus ganhos serão transferidos para você.

Segurança no Saque da futebol ao vivo no celular: Como

Evitar Problemas e Retirar Seu Dinheiro com Facilidade

Passo a Passo para Realizar Saque na futebol ao vivo na tv: Garantindo

Agilidade

Na resultado futebol ao vivo, a segurança dos seus dados financeiros é uma prioridade.

O processo de saque é rápido e confiável.

Quais São as Formas de Saque na g1 futebol ao vivo e Como Elas Garantem

Sua Segurança?

Tudo o que Você Precisa Para Solicitar o Seu Saque na futebol ao vivo

Saques seguros na futemax ao vivo futebol?

Sim, basta enviar a documentação correta e pronto, você receberá seu dinheiro rapidamente.

Você pode confiar na futebol ao vivo premiere para processar seus saques de forma rápida

e segura, enviando apenas alguns documentos essenciais.

Para retirar seus ganhos da futebol agora ao vivo, basta enviar seu CPF e

um comprovante de residência. O processo é simples e seguro.

Para realizar um saque na apk futebol ao vivo, basta enviar seus dados pessoais

e comprovantes. O processo é ágil e totalmente seguro.

Como Retirar Ganhos na tv tudo futebol ao vivo com Agilidade e Segurança

Como Retirar Seus Fundos na futebol interior ao vivo de

Forma Simples e Segura

Na futebol ao vivo e gratis, a segurança

dos seus fundos é garantida. Apenas envie seus documentos e seus saques serão processados sem

demora.

Saques seguros na site futebol ao vivo?

Sim, basta enviar a documentação correta e pronto, você

receberá seu dinheiro rapidamente.

A futebol ao vivo e online cuida de sua segurança financeira, permitindo que você retire seus fundos sem preocupações, desde

que envie os documentos corretos.

Quais São as Formas de Saque na futebol ao vivo santos e

Como Elas Garantem Sua Segurança?

Passo a Passo de Como Retirar Seus Ganhos na futebol ao vivo app com Facilidade

aplicativo futebol ao vivo: Como Retirar Dinheiro de Forma Rápida e Sem Complexidade

Processo de Retirada na futebol ao vivo sem travar:

Como Evitar Problemas e Garantir Agilidade

Saques Sem Complicação: Como Retirar Seus Ganhos

na futebol ao vivo de graca

Na tv brasil futebol ao vivo, a segurança

dos seus fundos é garantida. Apenas envie seus documentos e seus saques serão processados sem

demora.

Como Acelerar Seus Saques na futebol ao vivo na net: Dicas Para Evitar Demoras

Saques Sem Complicação: Como Retirar Seus Ganhos na placar ao vivo futebol

Como Realizar Saques na futebol ao vivo youtube com Facilidade e Segurança

O processo de saque na placar ao vivo de futebol é simples e direto.

Basta fornecer os documentos necessários e você terá seu dinheiro rapidamente.

Você sabia que na copa do brasil final, para realizar o

saque, tudo o que você precisa é um documento de identidade válido e um comprovante de residência recente?

Se você deseja sacar seus ganhos rapidamente, a jogos de hoje copa do brasil é a escolha certa.

Só precisa enviar os documentos corretos.

Como Retirar Seus Lucros de Forma Ágil na jogos de copa do brasil

Para realizar um saque na copa do brasil classificação, basta enviar seus

dados pessoais e comprovantes. O processo é ágil e totalmente seguro.

Saque na copa do brasil de futebol de 2025:

Como Enviar os Documentos Corretos para Evitar Retardos

Guia Completo Para Retirar Seus Fundos na sorteio copa do brasil de Forma Segura

Retirando Dinheiro da jogo da copa do brasil: Como Garantir que Seu Saque Seja Rápido e

Seguro

Quais São as Formas de Saque na copa do brasil oitavas e Como Elas Garantem Sua Segurança?

Na tabela da copa do brasil, a plataforma de pagamentos é segura,

o que garante a agilidade nos saques e a proteção dos seus dados financeiros.

Como Retirar Seus Fundos da jogos da copa do brasil 2025 de Forma Segura e

Eficiente

Cassino cod bet: Jogue e

Conquiste Vitórias Rápidas!

f12 bet: Apostas Fáceis e Grandes Vitórias!

Aposte e Conquiste Grandes Vitórias no brl bet!

Jogos Fáceis, Grandes Vitórias no Cassino cnc bet!

giga bet: Apostas Fáceis, Grandes Oportunidades de Vitória!

Jogue no Cassino nacional bet e Ganhe

Prêmios Instantâneos!

Aposte nos Jogos Populares do Cassino lv bet e Ganhe!

gg bet: Apostas Fáceis e Grandes Vitórias!

Aposte nos Jogos Populares do Cassino bet 61 e Vença!

Cassino estrella bet:

Onde Você Pode Ganhar com Facilidade!

Aposte nos Melhores Jogos e Ganhe no Cassino pag bet!

Ganhe Agora no Cassino seu bet com Facilidade!

Ganhe no pix bet com Jogos Fáceis e Populares!

Aposte e Vença no Cassino Online iri bet!

Ganhe no Cassino Online bet sul: Diversão e Vitória!

Jogue e Vença Agora no Cassino sporting bet!

Ganhe Agora com os Jogos Populares do tv bet!

Jogue no 166 bet e Vença com Facilidade!

Ganhe Rápido e Fácil no Cassino Online 20 bet!

Jogos Populares e Grandes Prêmios no Cassino Online um bet!

Descubra a Diversão e Vitória no Cassino bet 7!

Ganhe Agora no Cassino Online 9d bet com Jogos Populares!

Jogue Agora no bet 365

e Ganhe Grande!

Ganhe Grande nos Jogos Populares do Cassino

omg bet!

Ganhe Fácil no Cassino Online 9k bet!

Jogue no Cassino bet pix365 e Conquiste Grandes Vitórias!

Aposte nos Melhores Jogos e Ganhe no Cassino 3fcasino!

Cassino Online leon bet: Onde Você Sempre

Pode Ganhar!

Aposte no Cassino dj bet33 e Vença Agora Mesmo!

Experimente os Melhores Jogos no Cassino bet sson!

Aposte no Cassino luva bet e Ganhe Prêmios Fantásticos!

Ganhe Agora nos Jogos Populares do Cassino wingdus!

Ganhe no Cassino bet fury com Jogos Populares e Simples!

Ganhe no Cassino real bet com Jogos Populares e Simples!

Cassino Online 365 bets: Apostas

Fáceis, Grandes Vitórias!

Aposte e Vença no Cassino 8casino – Jogos Fáceis e Populares!

Aposte no Cassino pagol bet

e Vença Agora Mesmo!

aposta multipla: Como Evitar Erros ao Solicitar Seu Saque

Acelerando Seus Saques na aposta app:

Como Tornar o Processo Mais Ágil

Na caaa de aposta, a plataforma garante a segurança de suas informações, permitindo que

você retire seus ganhos de maneira tranquila e rápida.

Documentos Necessários para Saque na filme de aposta: Evite

Atrasos

Quer realizar um saque na aposta ganh?

Só precisa enviar seu CPF e um comprovante de pagamento.

Fácil e seguro!

Com a aposta paga, você pode realizar saques de forma rápida,

apenas enviando os documentos necessários, como identidade

e comprovante de pagamento.

A 9game aposta facilita

o saque de seus ganhos com um processo simples, onde você só

precisa enviar seu CPF e um comprovante de residência.

Como Realizar um Saque na 12bet aposta de Forma Simples e Ágil

Com a novibet aposta, os saques

são fáceis e rápidos, desde que você envie todos os documentos

solicitados. O processo é 100% seguro.

Como Realizar um Saque Rápido na aposta pixbet:

Dicas e Procedimentos

Retirando Dinheiro da 365 aposta:

Como Garantir que Seu Saque Seja Rápido e Seguro

aposta esporte

e a Retirada de Fundos: Como Garantir Seu Dinheiro em Menos

Tempo

Saque Rápido e Seguro: Como a sssgame aposta Protege Seus Ganhos

Passo a Passo para Retirar Seus Ganhos na pagbet aposta:

Agilidade e Segurança

Saque Sem Complicação: O Que Você Precisa Saber na aposta tudo bet

Saques Sem Complicação: Como Retirar Seus Ganhos na grupo de aposta

bbb aposta: Como Retirar Seus Ganhos de Forma Simples e sem Erros

Você sabia que a crash aposta oferece uma das maneiras mais seguras de retirar seus fundos online?

Só enviar seus documentos básicos.

Você sabia que a ganha e aposta oferece

uma das maneiras mais seguras de retirar seus fundos online?

Só enviar seus documentos básicos.

Na betsbola aposta, o

saque é rápido e fácil, e você pode ter certeza de que suas informações estão protegidas o tempo todo.

A aposta e ganhar é

uma das plataformas mais seguras para realizar saques. Você só precisa fornecer seus dados e comprovantes, e o saque será feito rapidamente.

Como Realizar Saques na betspeed aposta com Facilidade e Segurança

Saque Rápido na aposta jack: Passo

a Passo para Retirar Seu Dinheiro Sem Complicação

Agilidade e Segurança no Saque da aposta maxbet:

Como Funciona o Processo

Tudo Sobre Saque na spicy aposta: Como Retirar Seus Ganhos de Forma Rápida e Segura

Quais Documentos Você Precisa Enviar para Realizar

um Saque na aposta ufc?

Retirando Dinheiro da aposta jogos: O Que Fazer Para Garantir Seu Saque

Rápido

A aposta mr jack Garante a Segurança

dos Seus Saques: Saiba Como Evitar Problemas

Retirada Simples na mr aposta: Como Evitar Burocracias

Na aposta sorte,

o saque é rápido e fácil, e você pode ter certeza

de que suas informações estão protegidas o tempo todo.

Retirada de Fundos na aposta gamha: Como Solicitar Seu Saque de Forma Ágil

Como Retirar Seus Fundos da aposta cassino de Forma

Segura e Eficiente

Documentos e Procedimentos para Saque na casas aposta: Como Evitar Retardos

Com a app aposta, você tem

acesso a saques rápidos e sem complicações. Garanta a segurança dos seus dados enviando apenas

os documentos necessários.

Retirando Fundos na cas de aposta:

O Guia Completo de Segurança e Agilidade

f12 aposta:

Como Retirar Seus Ganhos Rapidamente e Sem Riscos

Para retirar seus ganhos na bolsa aposta, basta enviar os documentos necessários e você terá seu saque processado

em pouco tempo.

Guia Completo de Saque: Como Evitar Complicações na

luvabet aposta

aposta popo: Como Retirar Dinheiro de Forma Rápida e Sem Complexidade

Passo a Passo para Retirar Seus Ganhos na leon aposta: Agilidade e Segurança

Como Retirar Seus Ganhos da aposta ao vivo:

Sem Complicação e de Forma Segura

Retirando Dinheiro da casas da aposta: Como Garantir que Seu Saque Seja

Rápido e Seguro

Se você deseja sacar seus ganhos rapidamente, a criar aposta

é a escolha certa. Só precisa enviar os documentos corretos.

A cassino aposta facilita o saque de seus fundos

com um processo simples e seguro, onde você só precisa enviar alguns

documentos.

Ao retirar na rivalo aposta, você só precisa fornecer informações básicas, como CPF e identidade.

O sistema é rápido e altamente seguro!

A realsbet aposta oferece um processo de saque simples e rápido.

Basta fornecer os documentos exigidos e seus ganhos serão transferidos para você.

A aposta tigrinho

facilita o saque de seus ganhos com um processo simplificado, garantindo a segurança dos seus dados financeiros.

Saque Sem Complicação: O Que Você Precisa Saber na casadas aposta

A cada da aposta Protege Seu Dinheiro: Descubra Como Garantimos Saques Sem Riscos

rivery aposta: Como Solicitar

Saque com Documentação Adequada e Sem Atrasos

Retire Seu Dinheiro na ibet aposta de

Forma Rápida e Segura: Veja Como

A aposta bbb24 Protege Seu Dinheiro: Como Garantir Saques Rápidos e Seguros

Como Retirar Seus Lucros de Forma Ágil na h2bet aposta

Como Retirar Seu Dinheiro da 1 aposta app: Tudo o Que Você Precisa Saber

A site de aposta facilita o saque de seus ganhos com um processo simples, onde você

só precisa enviar seu CPF e um comprovante de residência.

A jack aposta Protege Seu Dinheiro:

Como Garantir Saques Rápidos e Seguros

Passo a Passo de Como Retirar Seus Ganhos na winmi aposta com Facilidade

bet aposta: Como Retirar Seu Dinheiro Com Facilidade e Segurança

aposta e ganha:

O Que Você Precisa Saber Antes de Solicitar

o Seu Saque

Se você está pensando em fazer um saque,

a a grande aposta oferece um processo fácil.

Apenas envie os documentos solicitados e a transação

será feita rapidamente.

Passo a Passo para Retirar Seus Ganhos na porno aposta:

Agilidade e Segurança

aposta bet e a Retirada de Fundos:

Como Garantir Seu Dinheiro em Menos Tempo

Você pode confiar na dupla aposta para processar seus saques

de forma rápida e segura, enviando apenas alguns documentos essenciais.

banca de aposta: Como

Garantir Que Seus Saques Cheguem Rápido e Com Segurança

Segurança no Saque da ganha aposta: Como Evitar Problemas e Retirar Seu Dinheiro com

Facilidade

Como Realizar um Saque na bolsa de aposta de Forma Simples e Ágil

Saque Rápido na aposta casada: Passo a Passo para Retirar Seu Dinheiro Sem Complicação

tigre aposta: Como Garantir Agilidade no

Processo de Saque

aposta ganhar: Como Obter Seu Dinheiro Rápido com

Documentação Correta

Como Acelerar Seus Saques na clube da aposta: Dicas Para Evitar Demoras

app de aposta e a Segurança de Seus Saques:

Como Protegemos Seu Dinheiro

Documentos Necessários para Saque na aposta mix: Evite Atrasos

casa aposta: Dicas para Realizar Saques Rápidos e Sem Problemas

casa das aposta: Como

Retirar Dinheiro de Forma Rápida e Sem Complexidade

Como Realizar um Saque Rápido na tvbet aposta: Dicas e Procedimentos

Saque Fácil e Seguro na aposta 24 horas:

O Que Fazer Para Não Perder Seu Dinheiro

1 aposta bet: O Que Você Precisa Saber Antes de Solicitar o Seu Saque

Como Retirar Seus Fundos da mc jack aposta de Forma Segura

e Eficiente

Saques Rápidos e Seguros na aposta 1 real: O Que Você Precisa Saber

aposta betano: O Que Você Precisa Saber Para Fazer Saques Rápidos

e Sem Erros

Na aposta 24h, seu saque é tratado com

a máxima prioridade, desde que você forneça os documentos necessários.

Sem complicação!

Você pode confiar na luva bet aposta para uma experiência de saque sem estresse, com segurança garantida e um processo

simplificado.

Guia Completo de Saque na aposta de jogo:

Como Garantir Que Seu Dinheiro Chegue Rápido

A blaze casino garante

total segurança nas transações, permitindo que você retire seus fundos de maneira rápida e sem

complicações.

Como Realizar Saques Sem Estresse na dobrowin

Com a today, seus

saques são feitos rapidamente, e você pode confiar que a plataforma oferece total segurança para suas transações.

Documentos Necessários Para Realizar Saque na doce: Confira a Lista Completa

A winbra garante a proteção dos seus dados durante o

processo de saque, com um sistema rápido e eficiente.

Como Evitar Problemas ao Solicitar Saques na esportesdasorte

O Que A esport bet Precisa

Para Realizar Seu Saque Sem Demoras

Se você precisa retirar fundos da brwin,

o processo é simples e rápido. Basta fornecer um documento de identidade e comprovante de

residência.

Segurança e Agilidade no Saque da pgwin: Como Retirar Seus Fundos com Confiança

Processo de Retirada na poplottery:

Como Evitar Problemas e Garantir Agilidade

queens e a Retirada de Fundos:

Como Garantir Seu Dinheiro em Menos Tempo

Segurança no Saque da casade apostas:

Como Evitar Problemas e Retirar Seu Dinheiro com Facilidade

Para retirar dinheiro na allwin, tudo o que você precisa fazer

é enviar seus documentos de identidade e residência.

Simples e seguro!

Saques rápidos e sem complicação. Na brdice, basta enviar seu

comprovante de identidade e residência, e pronto!

Saque na flames:

Como Enviar os Documentos Corretos para Evitar Retardos

Com a spinbookie, os saques são fáceis e rápidos,

desde que você envie todos os documentos solicitados.

O processo é 100% seguro.

Saque Fácil e Seguro na rivalry:

O Que Fazer Para Não Perder Seu Dinheiro

Ganhe com Facilidade nos Jogos Populares do 5500 bet!

Jogue e Ganhe no bet ting com Apostas Simples!

Jogue Agora no estrelas bet e Ganhe Fácil!

Jogue nos Melhores Jogos e Vença no Cassino green bet!

Ganhe no bwin bet com Jogos Simples e Populares!

No roleta, novos usuários podem aproveitar um bônus de 100$ ao se registrar

no site! Isso significa mais chances de ganhar e explorar uma grande variedade de jogos de cassino,

desde slots emocionantes até clássicos como roleta e blackjack.

Com o bônus de boas-vindas, você começa com

um saldo extra, o que aumenta suas chances de sucesso.

Cadastre-se agora e use os 100$ de bônus para experimentar seus jogos favoritos com mais facilidade.

Aproveite a oferta e comece sua aventura no cassino agora mesmo!

Registre-se e Receba 100$ de Bônus no bet77 (bet77-br.com) para Apostar!

Ganhe no Cassino tivo bet com Jogos Populares e Fáceis!

esportivabet Oferece 100$ de

Bônus para Novos Jogadores – Registre-se Já!

Jogue no prosport bet e

Conquiste Vitórias Rápidas!

Aposte Agora no Cassino betao bet e Ganhe com Facilidade!

Seu Bônus de 100$ Espera por Você no thelotter – Cadastre-se Agora!

Cassino beta trinta: Ganhe Jogando

os Melhores Jogos!

Ao se cadastrar no poker online,

você ganha um bônus de 100$ para começar sua

jornada no cassino com o pé direito! Não importa se você é

um novato ou um apostador experiente, o bônus de boas-vindas é

a oportunidade perfeita para explorar todas as opções que o site tem a oferecer.

Jogue seus jogos favoritos, descubra novas opções de apostas e aproveite para

testar estratégias sem risco, já que o bônus ajuda a

aumentar suas chances de ganhar. Cadastre-se hoje e comece com 100$!

Bônus de 100$ no roleta online – https://roletaonline-br.com: Faça Seu Cadastro Agora Mesmo!

Cadastre-se no tvbet

e Ganhe 100$ de Bônus de Boas-Vindas!

Bet61: 100$ de Bônus para Novos Jogadores – Cadastre-se Já!

Ao se cadastrar no misterjackbet, você ganha um

bônus de 100$ para começar sua jornada no cassino

com o pé direito! Não importa se você é um novato ou

um apostador experiente, o bônus de boas-vindas é a oportunidade perfeita para explorar todas as opções que o site

tem a oferecer. Jogue seus jogos favoritos, descubra novas opções de apostas e aproveite

para testar estratégias sem risco, já que o bônus ajuda a aumentar suas chances de ganhar.

Cadastre-se hoje e comece com 100$!

Ganhe Agora com os Jogos do Cassino maromba bet!

Ganhe Agora com os Jogos do Cassino beto barbosa!

Na futebol feminino ao vivo, o

processo de saque é simplificado e seguro.

Basta fornecer os documentos solicitados para que seu saque seja realizado rapidamente.

Na jogos futebol hoje ao vivo, a segurança dos seus dados financeiros é uma prioridade.

O processo de saque é rápido e confiável.

A futebol proporciona um saque rápido

e simples. Tudo o que você precisa fazer é enviar os documentos necessários, e

pronto!

Como Realizar um Saque na assistir futebol ao vivo de Forma Simples e Ágil

A ver futebol ao vivo oferece

saques rápidos e seguros, garantindo que seus dados financeiros sejam protegidos durante toda a transação.

O Que A placar de futebol ao vivo Precisa Para

Realizar Seu Saque Sem Demoras

A futebol hd ao vivo torna a experiência de retirada de fundos tranquila e rápida,

com a proteção total de suas informações

bancárias.

Segurança no Saque da futebol ao vivo futemax: Como Evitar Problemas

e Retirar Seu Dinheiro com Facilidade

Retirando Fundos na futebol ao vivo: O Guia Completo de Segurança e Agilidade

futebol ao vivo assistir: Como Evitar Erros ao Solicitar Seu Saque

Aproveite a oferta exclusiva do imperador bet

para novos usuários e receba 100$ de bônus ao

se registrar! Este bônus de boas-vindas permite que

você experimente uma vasta gama de jogos de cassino online sem precisar gastar

imediatamente. Com o bônus de 100$, você poderá explorar jogos como roleta, blackjack, caça-níqueis e

muito mais, aumentando suas chances de vitória

desde o primeiro minuto. Não perca essa chance única de começar com um valor significativo – cadastre-se agora!

No betsury,

ao Registrar-se, Você Recebe 100$ de Bônus!

No bet esporte, Você Começa com 100$ de Bônus ao

se Registrar!

100$ de Bônus no realbet para

Novos Usuários – Registre-se!

jogodeouro

Oferece 100$ de Bônus para Novos Jogadores – Registre-se Já!

Novo no novibet? Ganhe 100$ de

Bônus Ao Se Registrar!

Seu Registro no rivalry Vale 100$ de Bônus Imediato!

Aproveite a oferta exclusiva do infinity bet

para novos usuários e receba 100$ de bônus ao se registrar!

Este bônus de boas-vindas permite que você experimente uma

vasta gama de jogos de cassino online sem precisar gastar imediatamente.

Com o bônus de 100$, você poderá explorar jogos como roleta,

blackjack, caça-níqueis e muito mais, aumentando suas

chances de vitória desde o primeiro minuto. Não perca essa chance única de começar com

um valor significativo – cadastre-se agora!

Passo a Passo para Retirar Seus Ganhos na futebol online ao vivo:

Agilidade e Segurança

Novos Usuários no moverbet Ganham

100$ de Bônus ao se Cadastrar!

Saque Seguro na futebol ao vivo hoje na tv:

Como Evitar Fraudes e Garantir Seu Dinheiro

ver futebol ao vivo hoje:

O Que Você Precisa Fazer Para Garantir Saques Sem Atrasos

Ao retirar na futebol hoje ao vivo, você só precisa fornecer informações básicas,

como CPF e identidade. O sistema é rápido e altamente seguro!

Guia Completo de Saque na jogo de futebol ao vivo: Como

Garantir Que Seu Dinheiro Chegue Rápido

Como Realizar Saques na futebol hoje na tv ao vivo com

Facilidade e Segurança

Faça Seu Cadastro no campobet e Ganhe 100$

de Bônus Exclusivo!

Como Realizar um Saque na mundo fut futebol ao vivo de Forma Simples e

Ágil

Retirada Simples na futebol ao vivo de gra莽a: Como Evitar Burocracias

Acelerando Seus Saques na futebol ao vivo agora: Como Tornar o Processo

Mais Ágil

O Que A nosso futebol ao vivo Precisa Para Realizar Seu Saque Sem

Demoras

Como Solicitar Saque de Forma Rápida na futebol ao vivo tv:

Evite Atrasos

Bônus de 100$ ao Registrar-se no cbet – Aproveite Agora!

Você sabia que na futemax futebol ao vivo,

para realizar o saque, tudo o que você precisa é um documento de identidade

válido e um comprovante de residência recente?

O Que A futebol ao vivo flamengo

Precisa Para Realizar Seu Saque Sem Demoras

Como Retirar Seus Ganhos da futebol ao vivo multicanal:

O Processo Explicado

Na max futebol ao vivo, a

segurança dos seus saques é garantida, e o processo de retirada é ágil e sem complicação.

Saque Fácil e Seguro na futebol na tv hoje ao vivo:

O Que Fazer Para Não Perder Seu Dinheiro

Saques rápidos e seguros são garantidos na futebol max ao vivo.

Apenas envie os documentos corretos e seu dinheiro estará disponível

em breve.

futebol ao vivo br:

Como Garantir Agilidade no Processo de Saque

O Que A futebol ao vivo gremio Precisa Para Realizar Seu Saque

Sem Demoras

Segurança no Saque da futebol ao vivo brasil: Como Evitar Problemas e Retirar Seu

Dinheiro com Facilidade

Para retirar dinheiro da futebol ao vivo com imagem,

tudo o que você precisa fazer é enviar o seu

CPF e um comprovante de residência. Rápido e fácil!

A Importância da Verificação de Documentos no Saque da

premiere futebol ao vivo

A ao vivo na tv futebol oferece

saques rápidos e sem complicação, com total segurança para seus dados e transações financeiras.

A futebol gr谩tis ao vivo garante que

sua experiência de saque seja tranquila, com total segurança em cada transação.

Com a jogos futebol ao vivo, você pode retirar seu dinheiro rapidamente.

Só precisa enviar os documentos certos

e o saque será processado de forma eficiente.

Segurança no Saque da tv ao vivo futebol: Como Evitar Problemas e Retirar Seu Dinheiro com Facilidade

futebol na tv ao vivo: Como Garantir Saques Rápidos e

Sem Complicações

Documentos Necessários Para Realizar Saque na futebol ao vivo resultado: Confira a Lista Completa

Na radio futebol ao vivo, a plataforma de pagamentos é segura, o que garante a

agilidade nos saques e a proteção dos seus dados financeiros.

futebol tv ao vivo: Como

Garantir que Seus Saques Sejam Processados Sem Erros

futebol ao vivo online:

Como Retirar Seus Ganhos de Forma Simples e sem Erros

Se você precisa retirar fundos da tv online futebol ao vivo, o processo é simples

e rápido. Basta fornecer um documento de identidade e comprovante de residência.

futebol ao vivo rmc e a Segurança

de Seus Saques: Como Protegemos Seu Dinheiro

Na tudo tv futebol ao vivo, você

pode retirar seus ganhos rapidamente, com a certeza de que suas informações bancárias estão sempre protegidas.

futebol ao vivo on line:

O Que Você Precisa Fazer Para Retirar Seus Ganhos Sem Problemas

Guia Completo Para Retirar Seus Fundos na ao vivo futebol de Forma Segura

Você sabia que a sbt futebol ao vivo hoje

oferece uma das maneiras mais seguras de retirar seus fundos online?

Só enviar seus documentos básicos.

Se você busca uma maneira segura de retirar seus ganhos,

a ver futebol ao vivo gratis é

a melhor escolha. Envie os documentos solicitados e pronto!

Passo a Passo para Retirar Seus Ganhos na placar do futebol ao vivo: Agilidade e Segurança

futebol ao vivo no youtube: Como Evitar

Problemas ao Solicitar um Saque

Com a futebol pelo mundo ao vivo, seus saques

são feitos rapidamente, e você pode confiar que a

plataforma oferece total segurança para suas transações.

futebol americano ao vivo:

Como Solicitar Saque com Documentação Adequada e Sem Atrasos

Retirar dinheiro da futebol ao vivo biz é simples!

Envie sua identidade e comprovante de residência e aguarde a confirmação para uma

transação rápida.

Como Acelerar o Processo de Retirada de Fundos na ver futebol ao vivo online

Guia Completo de Saque: Como Evitar Complicações na jogos ao vivo futebol

Segurança no Saque da jogos de futebol ao vivo: Como Evitar Problemas e Retirar Seu Dinheiro com Facilidade

Para retirar seus ganhos da futebol gratis ao vivo, basta enviar seu CPF e um comprovante de residência.

O processo é simples e seguro.

Você sabia que a futebol play ao vivo oferece uma das maneiras mais seguras

de retirar seus fundos online? Só enviar seus documentos básicos.

A segurança da sua conta é prioridade na assistir ao vivo futebol.

O processo de retirada é rápido e você pode confiar que

seus dados financeiros estão protegidos.

A futebol ao vivo hoje oferece um processo de saque simples e seguro, garantindo que suas informações financeiras estarão sempre protegidas.

futebol ao vivo de hoje:

Como Garantir Agilidade no Processo de Saque

Como Retirar Seu Dinheiro da futebol ao vivo palmeiras: Tudo o Que Você Precisa Saber

Retirando Dinheiro da futebol ao vivo gratis:

O Que Fazer Para Garantir Seu Saque Rápido

Retirada de Fundos Sem Estresse: Como a app futebol ao vivo Garante Seu Saque

Retirada de Fundos Sem Estresse: Como a resultados futebol ao vivo Garante Seu Saque

Retirar seu dinheiro na futebol ao vivo multi é simples!

Apenas envie os documentos necessários e seu saque será processado rapidamente.

Saque Seguro na futebol ao vivo na tv hoje: Como Evitar Fraudes e Garantir Seu

Dinheiro

futebol ao vivo tudo tv: Como Fazer Saque Sem Estresse e Com Garantia de

Segurança

The Real Person!

The Real Person!

https://pinupaz.top/# pin-up

Aproveite 100$ de Bônus ao Se Registrar no ggbet – https://ggbet-88.com – Cadastre-se Já!

Com a futebol ao vivo grates, o processo de saque é direto e sem complicação.

Envie os documentos corretos e você receberá seus fundos rapidamente.

futebol ao vivo net:

Como Realizar Saque Rápido e Sem Stress

Como Retirar Seus Ganhos da futebol ao vivo online hd:

Sem Complicação e de Forma Segura

Quais Documentos Você Precisa Enviar para Realizar um Saque na assisti futebol ao vivo?

Aposte e Vença com Jogos Populares no beto ribeiro!

Cassino Online kto bet: Jogos Populares,

Grandes Oportunidades!

Ganhe Grande no Cassino sorte na bet!

The Real Person!

The Real Person!

buy modafinil online: purchase Modafinil without prescription – buy modafinil online

assista futebol ao vivo:

Como Retirar Seus Fundos de Forma Eficiente

Saque Seguro na futebol max ao vivo hoje:

Como Evitar Fraudes e Garantir Seu Dinheiro

Guia Completo Para Retirar Seus Fundos na canal de futebol ao vivo de Forma Segura

Retire Seu Dinheiro na flashscore futebol ao vivo de Forma Rápida e

Segura: Veja Como

Ganhe Agora nos Jogos Populares do Cassino flush win!

Ganhe Rápido com os Jogos do Cassino Online infinity bet!

heads bet: Aposte Agora e Ganhe Rápido!

Saque na futebol ao vivo serie b: Como Garantir que Seus Ganhos Cheguem Rápido à Sua Conta

Passo a Passo de Como Retirar Seus Ganhos na futebol ao vivo placar com Facilidade

Saques na tv brasil ao vivo futebol: O Que Você

Precisa Saber Para Retirar Seu Dinheiro com Facilidade

The Real Person!

The Real Person!

no doctor visit required: cheap Viagra online – buy generic Viagra online

Jogue no Cassino Online beto carrero

e Aumente Suas Chances!

Se você está buscando um processo de saque

rápido e seguro, a portal rmc futebol ao vivo oferece exatamente isso.

Envie seus documentos e pronto!

Aposte nos Jogos Populares do Cassino marjack bet e Ganhe!

pix casino:

Vença com Jogos Populares e Rápidos!

mr bet jack:

Apostas Simples, Grandes Premiações!

rei do futebol ao vivo e a Segurança de Seus Saques: Como Protegemos Seu Dinheiro

Jogue nos Melhores Jogos e Vença no Cassino

esoccer bet!

Se você deseja retirar seus fundos de forma rápida, a max ao vivo futebol é a escolha

ideal. Com um processo simples, você só precisa enviar os documentos corretos.

Ganhe Rápido com os Jogos Populares do Cassino 8 bet!

The Real Person!

The Real Person!

best price Cialis tablets: best price Cialis tablets – online Cialis pharmacy

Aposte com 100$ de Bônus no wazamba – Cadastre-se e Aproveite!

The Real Person!

The Real Person!

affordable ED medication: FDA approved generic Cialis – best price Cialis tablets

juntosbet Oferece 100$ de Bônus para Novos Jogadores – Registre-se Já!

The Real Person!

The Real Person!

reliable online pharmacy Cialis: reliable online pharmacy Cialis – best price Cialis tablets

acompanhar futebol ao vivo:

O Que Você Precisa Fazer Para Retirar Seus Ganhos Sem

Problemas

No winbra, Você Começa com 100$ de

Bônus ao se Registrar!

Com a futebol de graça ao vivo, seus

saques são processados rapidamente. Envie apenas os documentos certos e receba

seu dinheiro em breve.

The Real Person!

The Real Person!

Modafinil for sale: buy modafinil online – modafinil legality

Faça Seu Cadastro no moverbet e Ganhe 100$ de Bônus Exclusivo!

Aproveite a oferta exclusiva do brwin para novos usuários e receba 100$ de bônus ao se registrar!

Este bônus de boas-vindas permite que você experimente uma vasta gama de jogos de cassino online sem precisar gastar imediatamente.

Com o bônus de 100$, você poderá explorar jogos como roleta, blackjack, caça-níqueis e muito mais,

aumentando suas chances de vitória desde o primeiro minuto.

Não perca essa chance única de começar com um valor significativo – cadastre-se

agora!

talon777 Oferece 100$ de Bônus para Novos Jogadores – Registre-se Já!