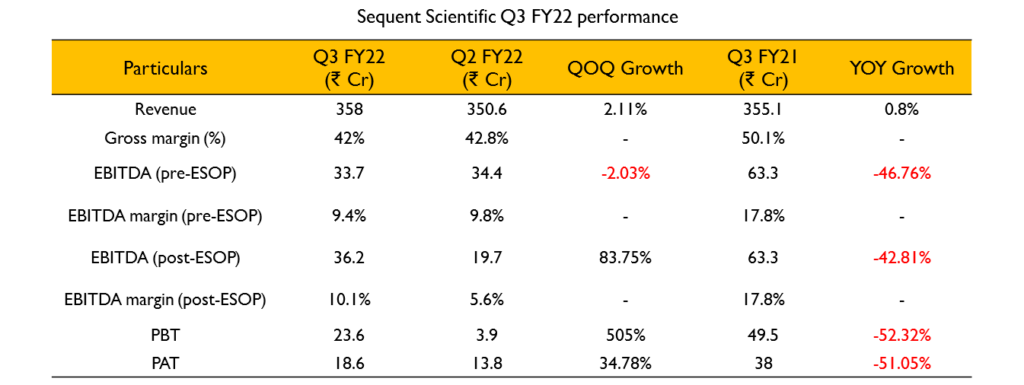

- Revenues for the quarter stood at ₹358 Cr (4.8% growth YoY). Growth was mainly driven by the Formulations business which grew at 18.5% YoY on a constant currency basis whereas the API business declined by 20% YoY driven by logistic challenges and subdued demand for Albendazole.

- Growth in the API portfolio excluding Albendazole has been strong in the first 9 months. Albendazole demand still remains subdued but there is a strong recovery in demand QoQ.

- There was a significant improvement in the API order book during the quarter although congestion at ports led to 15% of API dispatches not making it to reported numbers. API sales are almost at Q3 FY21 levels which was their best ever quarter in terms of API sales.

- Growth outlook in the API business for FY23 looks strong as there is going to be a strong recovery in Albendazole and the commercialization of the multi-year supply agreement with a Top 10 animal health company.

- Strong performance in India, Latam and Turkey were the main drivers in the growth of the formulations business.

- Turkey business grew at 34% on a constant currency basis although they faced a lot of volatility in terms of the currency. They continue to build Turkey as a major hub for the export business.

- The Formulation business has been plagued with rising input prices. Although the price of raw materials is still high, there is a stabilization around the volatility. They have taken some price increases to protect the margins – the major impact of this will come in Q4.

- The acquisition of Nourrie in Brazil has helped them enter the fast growing companion animals segment. They also acquired the minority interest in Alivira Brazil during the quarter, making it a wholly owned subsidiary. They now have 100% ownership of all subsidiaries except 40% in Spain and a very negligible share in Sweden.

- About 1/3rd of revenues from the API business come from Albendazole. WHO is the main buyer for this product and they are currently not buying because schools in Africa are closed. The schools in Africa are opening up and the WHO demand is coming back.

- The first supplies against the multi-year agreement with a Top 10 Animal Health company are going to happen towards the end of Q1 FY23 or early Q2 FY23. They will not hit the peak revenues from that contract in FY23, the peak will be hit in FY24.

- Turkey is a very important market to them as it is one of the Top 10 AH markets globally and it is also a very important exporter for the region. It is an injectable based business with good margins and a EU approved facility. The cost of manufacturing in Turkey today is significantly lower than India.

- The Turkey facility is a comprehensive facility across 8 manufacturing formats including injectables, orals and liquids. Products manufactured in Turkey are going to be exported to all markets excluding the US.

- The Brazil business has posted good growth consistently without many fluctuations. They had bought the company when it was bankrupt and it has become one of their best performers.

- The Bremer (Germany) facility has been delayed due to COVID. It has been delayed for 18 months, it is expected to start this year and it will be ready for USFDA inspection by the end of the calendar year.

- The Capex over the next 2 years is a little over ₹100 Cr. It will be split between Brazil, Turkey, India and the major part will go towards Germany.

I am not very great with English but I line up this very easy to understand.

Yeah bookmaking this wasn’t a speculative conclusion outstanding post! .

I visited a lot of website but I conceive this one has got something special in it in it

I’m curious to find out what blog system you’re working with? I’m experiencing some small security problems with my latest site and I would like to find something more safeguarded. Do you have any solutions?

Hello There. I found your blog the use of msn. That is an extremely smartly written article. I’ll be sure to bookmark it and come back to read more of your useful information. Thanks for the post. I’ll certainly return.

hi!,I really like your writing very a lot! proportion we be in contact more about your article on AOL? I require an expert on this house to resolve my problem. Maybe that is you! Looking forward to look you.

F*ckin’ remarkable things here. I’m very glad to see your article. Thanks a lot and i’m looking forward to contact you. Will you please drop me a e-mail?

Good – I should definitely pronounce, impressed with your site. I had no trouble navigating through all the tabs and related info ended up being truly easy to do to access. I recently found what I hoped for before you know it in the least. Reasonably unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your customer to communicate. Excellent task..

Hi would you mind sharing which blog platform you’re using? I’m looking to start my own blog in the near future but I’m having a difficult time choosing between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design seems different then most blogs and I’m looking for something unique. P.S Sorry for being off-topic but I had to ask!

My brother suggested I might like this web site. He was entirely right. This post actually made my day. You can not imagine just how much time I had spent for this information! Thanks!

Magnificent goods from you, man. I’ve take note your stuff prior to and you are simply extremely magnificent. I really like what you have acquired here, certainly like what you are stating and the way in which wherein you say it. You’re making it entertaining and you still care for to keep it sensible. I cant wait to learn much more from you. That is really a terrific site.

Wow! This could be one particular of the most beneficial blogs We have ever arrive across on this subject. Basically Excellent. I am also an expert in this topic therefore I can understand your effort.

I really like your writing style, fantastic information, appreciate it for putting up : D.

The Real Person!

The Real Person!

Kamagra pharmacie en ligne: Acheter Kamagra site fiable – kamagra pas cher

The Real Person!

The Real Person!

kamagra 100mg prix: Kamagra Oral Jelly pas cher – Acheter Kamagra site fiable

pharmacie en ligne pas cher: trouver un mГ©dicament en pharmacie – pharmacie en ligne france livraison internationale pharmafst.com

The Real Person!

The Real Person!

Acheter Kamagra site fiable: Kamagra Oral Jelly pas cher – acheter kamagra site fiable

Pharmacie en ligne livraison Europe: Meilleure pharmacie en ligne – pharmacie en ligne france fiable pharmafst.com

The Real Person!

The Real Person!

Tadalafil achat en ligne: Pharmacie en ligne Cialis sans ordonnance – Acheter Cialis 20 mg pas cher tadalmed.shop

Achat Cialis en ligne fiable: Pharmacie en ligne Cialis sans ordonnance – Tadalafil 20 mg prix sans ordonnance tadalmed.shop

The Real Person!

The Real Person!

Tadalafil achat en ligne: cialis sans ordonnance – cialis prix tadalmed.shop

acheter kamagra site fiable: Kamagra pharmacie en ligne – kamagra 100mg prix

The Real Person!

The Real Person!

Pharmacie en ligne livraison Europe: Pharmacie en ligne France – pharmacie en ligne france livraison belgique pharmafst.com

The Real Person!

The Real Person!

pharmacie en ligne france livraison belgique: pharmacie en ligne – pharmacie en ligne sans ordonnance pharmafst.com

The Real Person!

The Real Person!

Kamagra Commander maintenant: kamagra gel – kamagra en ligne

The Real Person!

The Real Person!

Acheter Cialis: Achat Cialis en ligne fiable – cialis prix tadalmed.shop

The Real Person!

The Real Person!

Pharmacie en ligne livraison Europe: Pharmacie en ligne France – acheter mГ©dicament en ligne sans ordonnance pharmafst.com

The Real Person!

The Real Person!

pharmacie en ligne pas cher: pharmacie en ligne sans ordonnance – pharmacie en ligne france livraison belgique pharmafst.com

The Real Person!

The Real Person!

Tadalafil achat en ligne: Acheter Cialis 20 mg pas cher – Tadalafil 20 mg prix sans ordonnance tadalmed.shop

The Real Person!

The Real Person!

Tadalafil achat en ligne: Cialis generique prix – cialis prix tadalmed.shop

The Real Person!

The Real Person!

kamagra gel: achat kamagra – kamagra en ligne

The Real Person!

The Real Person!

Acheter Viagra Cialis sans ordonnance: Achat Cialis en ligne fiable – cialis prix tadalmed.shop

The Real Person!

The Real Person!

pharmacie en ligne france livraison belgique: pharmacie en ligne – Pharmacie Internationale en ligne pharmafst.com

The Real Person!

The Real Person!

Achetez vos kamagra medicaments: kamagra livraison 24h – Kamagra pharmacie en ligne

The Real Person!

The Real Person!

Acheter Kamagra site fiable: Achetez vos kamagra medicaments – Achetez vos kamagra medicaments

The Real Person!

The Real Person!

kamagra en ligne: kamagra pas cher – acheter kamagra site fiable

The Real Person!

The Real Person!

pharmacie en ligne fiable: pharmacie en ligne pas cher – trouver un mГ©dicament en pharmacie pharmafst.com

The Real Person!

The Real Person!

indian pharmacy online: Medicine From India – indian pharmacy

The Real Person!

The Real Person!

canadian drugs online: ExpressRxCanada – canadian king pharmacy

The Real Person!

The Real Person!

mexican online pharmacy: mexico pharmacies prescription drugs – RxExpressMexico

mexican rx online mexican online pharmacies prescription drugs mexican online pharmacy

The Real Person!

The Real Person!

mexican rx online: Rx Express Mexico – mexican rx online

medicine courier from India to USA: Medicine From India – MedicineFromIndia

The Real Person!

The Real Person!

Medicine From India: pharmacy website india – MedicineFromIndia

indian pharmacy online MedicineFromIndia indian pharmacy

indian pharmacy: medicine courier from India to USA – MedicineFromIndia

The Real Person!

The Real Person!

safe canadian pharmacies: Express Rx Canada – canada rx pharmacy world

Medicine From India indian pharmacy online indian pharmacy online shopping

reliable canadian online pharmacy: Buy medicine from Canada – canadian pharmacies comparison

The Real Person!

The Real Person!

mexican online pharmacy: reputable mexican pharmacies online – mexican rx online

indian pharmacy Medicine From India medicine courier from India to USA

indian pharmacy online: Medicine From India – indian pharmacy online

The Real Person!

The Real Person!

пин ап вход: pin up вход – пин ап казино

The Real Person!

The Real Person!

вавада: вавада официальный сайт – вавада казино

The Real Person!

The Real Person!

vavada вход: вавада официальный сайт – vavada

The Real Person!

The Real Person!

vavada вход: вавада официальный сайт – вавада официальный сайт

The Real Person!

The Real Person!

пинап казино: пин ап казино официальный сайт – pin up вход

The Real Person!

The Real Person!

вавада зеркало: вавада – vavada casino

The Real Person!

The Real Person!

vavada вход: вавада казино – vavada вход

The Real Person!

The Real Person!

пинап казино: пин ап казино официальный сайт – пин ап казино официальный сайт

vavada casino: vavada casino – вавада казино

пин ап вход: пин ап зеркало – пин ап казино официальный сайт

пинап казино: пин ап казино официальный сайт – пин ап казино

вавада зеркало: vavada casino – vavada вход

пинап казино: пин ап казино – пин ап вход

пин ап вход: пин ап казино официальный сайт – pin up вход

pin up вход: pin up вход – pin up вход

пин ап казино официальный сайт: пинап казино – пин ап казино

пин ап казино официальный сайт: пин ап казино – пин ап зеркало

vavada casino: вавада официальный сайт – вавада зеркало

pinup az: pin-up casino giris – pin up az

пин ап вход: пин ап казино – pin up вход

пин ап казино: пин ап казино официальный сайт – пин ап казино официальный сайт

vavada: вавада – вавада официальный сайт

pin up: pinup az – pinup az

pin up casino: pin-up – pin up

The Real Person!

The Real Person!

https://pinupaz.top/# pin-up

I am not real wonderful with English but I find this real easy to translate.

The Real Person!

The Real Person!

order Cialis online no prescription: FDA approved generic Cialis – affordable ED medication

The Real Person!

The Real Person!

trusted Viagra suppliers: no doctor visit required – order Viagra discreetly

The Real Person!

The Real Person!

buy modafinil online: buy modafinil online – modafinil 2025

The Real Person!

The Real Person!

fast Viagra delivery: cheap Viagra online – buy generic Viagra online

The Real Person!

The Real Person!

safe online pharmacy: safe online pharmacy – cheap Viagra online

The Real Person!

The Real Person!

modafinil pharmacy: modafinil 2025 – modafinil pharmacy

Whats Taking place i’m new to this, I stumbled upon this I have discovered It positively helpful and it has aided me out loads. I hope to contribute & help different users like its aided me. Great job.

The Real Person!

The Real Person!

discreet shipping ED pills: affordable ED medication – Cialis without prescription

modafinil 2025: buy modafinil online – modafinil legality

The Real Person!

The Real Person!

purchase Modafinil without prescription: Modafinil for sale – purchase Modafinil without prescription

http://modafinilmd.store/# Modafinil for sale

The Real Person!

The Real Person!

generic sildenafil 100mg: legit Viagra online – Viagra without prescription

reliable online pharmacy Cialis: cheap Cialis online – Cialis without prescription

https://maxviagramd.shop/# trusted Viagra suppliers

The Real Person!

The Real Person!

modafinil 2025: doctor-reviewed advice – legal Modafinil purchase

discreet shipping: discreet shipping – same-day Viagra shipping

https://zipgenericmd.com/# discreet shipping ED pills

The Real Person!

The Real Person!

modafinil legality: verified Modafinil vendors – verified Modafinil vendors

http://zipgenericmd.com/# discreet shipping ED pills

buy generic Viagra online: generic sildenafil 100mg – order Viagra discreetly

The Real Person!

The Real Person!

generic sildenafil 100mg: order Viagra discreetly – legit Viagra online

The Real Person!

The Real Person!

cost of generic clomid without dr prescription: buying clomid for sale – order generic clomid without rx

The Real Person!

The Real Person!

Amo Health Care: Amo Health Care – amoxicillin 500 mg capsule

The Real Person!

The Real Person!

get clomid tablets: Clom Health – how to get cheap clomid prices

The Real Person!

The Real Person!

prednisone no rx: PredniHealth – PredniHealth

cialis dosage for bph: Tadal Access – tadalafil cost cvs

cialis online reviews: TadalAccess – when to take cialis for best results

what is the normal dose of cialis: cialis prescription online – find tadalafil

Ero Pharm Fast Ero Pharm Fast Ero Pharm Fast

Ero Pharm Fast: ed doctor online – Ero Pharm Fast

buy antibiotics online buy antibiotics online uk cheapest antibiotics

buy ed medication: Ero Pharm Fast – cheapest erectile dysfunction pills

Over the counter antibiotics pills: buy antibiotics online uk – get antibiotics quickly

https://eropharmfast.shop/# buy erectile dysfunction pills

online ed pills: buy erectile dysfunction pills online – Ero Pharm Fast

cheapest ed treatment: order ed pills online – Ero Pharm Fast

Ero Pharm Fast ed medicine online what is the cheapest ed medication

Ero Pharm Fast: Ero Pharm Fast – Ero Pharm Fast

online pharmacy australia: Medications online Australia – Pharm Au24

https://pharmau24.com/# Buy medicine online Australia

ed online pharmacy: low cost ed pills – where can i buy erectile dysfunction pills

Licensed online pharmacy AU Pharm Au 24 Online medication store Australia

buy antibiotics: Biot Pharm – buy antibiotics online

Ero Pharm Fast: Ero Pharm Fast – erection pills online

Over the counter antibiotics for infection buy antibiotics online uk buy antibiotics from canada

buy antibiotics from canada: buy antibiotics online uk – buy antibiotics from canada

https://biotpharm.com/# Over the counter antibiotics for infection

buy erectile dysfunction pills online ed rx online Ero Pharm Fast

Very interesting info !Perfect just what I was looking for!

Your article helped me a lot, is there any more related content? Thanks!

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

There is evidently a bunch to realize about this. I feel you made some nice points in features also.

I’m really loving the theme/design of your weblog. Do you ever run into any internet browser compatibility problems? A handful of my blog readers have complained about my website not operating correctly in Explorer but looks great in Safari. Do you have any advice to help fix this problem?

What i don’t realize is if truth be told how you’re now not really a lot more well-favored than you might be now. You are so intelligent. You understand thus considerably relating to this subject, made me individually imagine it from numerous numerous angles. Its like men and women aren’t interested until it is one thing to do with Lady gaga! Your individual stuffs great. All the time handle it up!

Good – I should certainly pronounce, impressed with your website. I had no trouble navigating through all tabs and related info ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Reasonably unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your customer to communicate. Excellent task.

I discovered your blog site on google and check a few of your early posts. Continue to keep up the very good operate. I just additional up your RSS feed to my MSN News Reader. Seeking forward to reading more from you later on!…

I’m not sure exactly why but this blog is loading extremely slow for me. Is anyone else having this issue or is it a problem on my end? I’ll check back later and see if the problem still exists.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good. https://accounts.binance.info/en-IN/register?ref=UM6SMJM3

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

I’m really loving the theme/design of your web site. Do you ever run into any web browser compatibility problems? A small number of my blog visitors have complained about my blog not operating correctly in Explorer but looks great in Chrome. Do you have any recommendations to help fix this issue?

F*ckin’ awesome issues here. I’m very satisfied to see your post. Thank you a lot and i’m taking a look forward to touch you. Will you kindly drop me a e-mail?

Yay google is my queen helped me to find this outstanding web site! .

You are my intake, I possess few blogs and often run out from to post .

I was curious if you ever considered changing the layout of your site? Its very well written; I love what youve got to say. But maybe you could a little more in the way of content so people could connect with it better. Youve got an awful lot of text for only having one or 2 images. Maybe you could space it out better?

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Thank you for sharing superb informations. Your web site is so cool. I’m impressed by the details that you?¦ve on this website. It reveals how nicely you understand this subject. Bookmarked this website page, will come back for extra articles. You, my friend, ROCK! I found simply the information I already searched all over the place and simply couldn’t come across. What an ideal site.

There is obviously a bundle to realize about this. I assume you made some nice points in features also.

I haven?¦t checked in here for some time as I thought it was getting boring, but the last several posts are great quality so I guess I?¦ll add you back to my daily bloglist. You deserve it my friend 🙂

Hello would you mind stating which blog platform you’re working with? I’m planning to start my own blog soon but I’m having a difficult time making a decision between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design seems different then most blogs and I’m looking for something completely unique. P.S My apologies for getting off-topic but I had to ask!

Hi, I think your website might be having browser compatibility issues. When I look at your blog in Opera, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, terrific blog!

Today, while I was at work, my sister stole my apple ipad and tested to see if it can survive a 40 foot drop, just so she can be a youtube sensation. My apple ipad is now broken and she has 83 views. I know this is completely off topic but I had to share it with someone!

Hello! I just would like to give a huge thumbs up for the great info you have here on this post. I will be coming back to your blog for more soon.

wonderful points altogether, you simply gained a new reader. What would you recommend about your post that you made some days ago? Any positive?